La-Z-Boy Inc (NYSE:LZB) is a leader in the U.S. furniture business with integrated wholesale manufacturing and more than 175 company-owned stores with an even larger franchise retail network. Despite a tough industry environment over the past year amid inflationary cost pressures and ongoing macro headwinds, the stock has managed to outperform, up more than 30% this year, with a string of better-than-expected results.

The attraction of LZB here starts with its solid fundamentals including a trend of recurring profitability, free cash flow, and a rock-solid balance sheet. We last covered the La-Z-Boy with a bullish note in 2022, highlighting many of these strong points supporting a positive outlook.

Our update today brings some attention to the company’s latest results, which beat consensus, but also featured mixed indicators that deserve some context. In our view, LZB remains well-positioned to climb higher as we see shares as still undervalued by the market.

Seeking Alpha

LZB Financials Recap

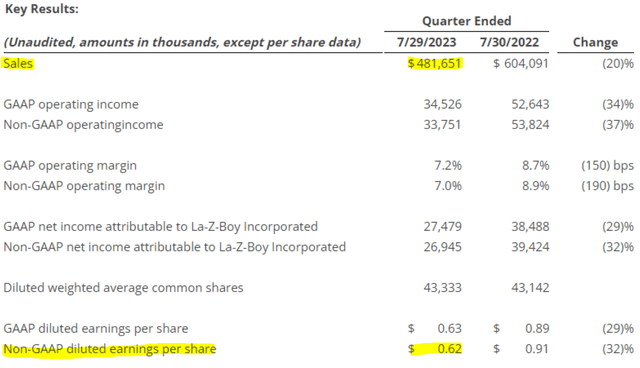

LZB fiscal Q1 non-GAAP EPS of $0.62 came in $0.07 ahead of market estimates while revenue of $482 million also beat expectations. At the same time, the year-over-year change to these headline figures likely raised some eyebrows. Sales fell by -20% from the period last year while EPS was -32% lower.

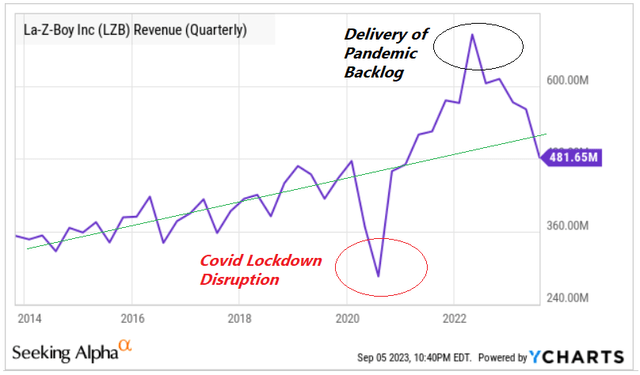

The explanation here is that the company benefited in 2022 from fulfilling a large backlog of orders that had accumulated going back to the early stages of the pandemic. This resulted in some exceptional comps, with this year being more defined by a return to normal in terms of its operations and inventory management.

source: company IR

The more important figure to focus on is the level of company-owned same-store-sales, which are up by 2%. This metric better reflects core trends considering the macro circumstances. Delivered sales are also up 16% compared to pre-pandemic levels.

While the non-GAAP operating margin at 7.0% was down from 8.7% in the period last year, this level included a 70 basis point increase in the operating margin from the wholesale segment, capturing some cost savings efforts. Free cash flow of $12.5 million was even up slightly from $12.1 million in Q1 fiscal 2023.

The takeaway here is that sales and earnings are above pre-pandemic levels and management remains “encouraged” on conditions going forward. While not offering full-year financial targets, La-Z-Boy is guiding a stronger back half of the year with near-term fiscal Q2 sales between $490 and $510 million, representing a 4% sequential increase at the midpoint from Q1.

source: yCharts

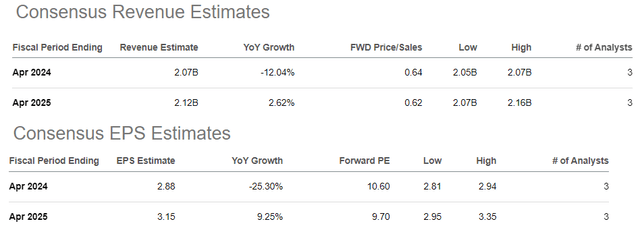

According to market estimates, a full-year fiscal 2024 revenue forecast of $2.1 billion represents a -12% decline from last year, again considering the high benchmark of comps. An EPS estimate of $2.88 this year, if confirmed, would be -25% lower than the $3.86 in fiscal 2023.

Looking ahead, the expectation is for renewed top-line and earnings growth by next year, with the company benefiting from firming margins and organic growth. On this point, the strategy is to expand and continue opening new “Furniture Galleries” stores while building momentum in the smaller “JoyBird” modern furniture brand seen as a future growth driver.

Seeking Alpha

What’s Next For LZB?

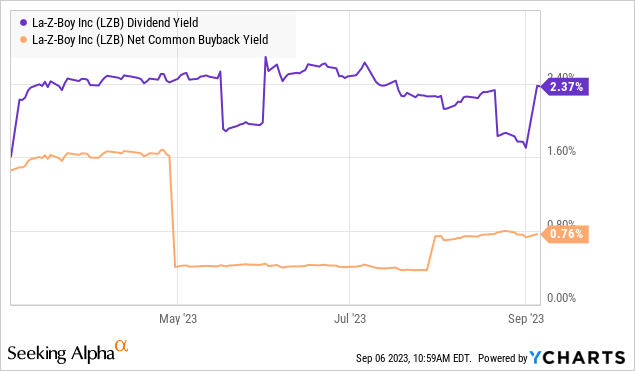

The way we’re looking at LZB is that this is a high-quality business with a record of solid execution and room to consolidate its market position. Investors get a $0.185 per share quarterly dividend that yields 2.4%, well-supported by underlying cash flows, considering a 25% payout ratio on the current year’s earnings, in addition to an ongoing share buyback program.

On the other hand, the concern here for the company relates more to the macro backdrop, with currently high-interest rates weighing on consumers. There is also a connection between the furniture business and the housing market, and that dynamic appears to be a headwind given falling existing home sales. The setup poses a risk to demand and a downside to current estimates that would likely pressure the stock.

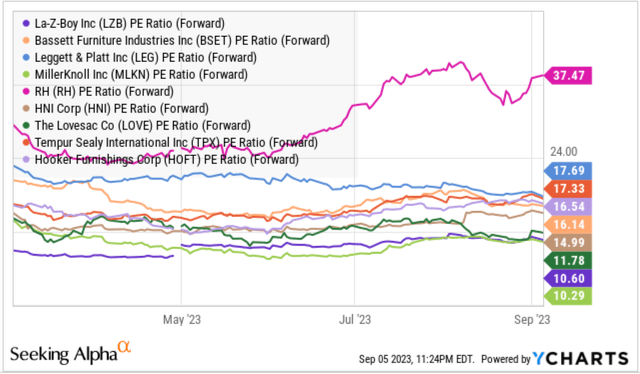

All that being said, LZB still stands out as one of the better-value names in this market segment. Shares trading at a 10.6x forward P/E are a large discount relative to peers like Bassett Furniture Industries Inc (BSET), and Hooker Furnishings Corp (HOFT) trading at multiples above 15x.

By this measure, LZB is undervalued in our opinion, and the recent “messy” results could be one reason if it means the market is overlooking the underlying strength evident by measures like the comp sales gains.

Several other comparables like MillerKnoll Inc (MLKN) or HNI Corp (HNI) have greater exposure to office furniture, which has the added layer of uncertainties related to the corporate real estate market and work-from-home dynamics. There is a case to be made that LZB’s fundamental quality could limit the stock’s downside relative to another player in a broader cyclical slowdown.

We can also take a “glass is the half-full” approach. A scenario where interest rates stabilize or fall and economic conditions remain resilient are part of the bullish case. The idea here is that LZB could capture a growth rebound that re-accelerates demand for furniture, allowing it to exceed consensus estimates.

source: yCharts

Final Thoughts

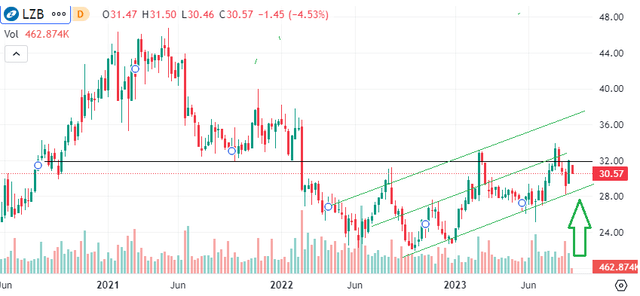

Ultimately, we see LZB trading higher by this time next year and an updated price target of $37.50, representing a forward P/E of 13x on the current year consensus EPS of $2.88. It might not be a straight line higher, but between our bullish outlook on the market and optimism toward the economy, LZB should continue to perform well. Shares are attractive, particularly within the furniture segment.

We mentioned the risks on the macro side. Over the next few quarters, it will be important for LZB to confirm a stabilization of its top line. The trends in the operating margin and same-store sales are key monitoring points.

Seeking Alpha

Read the full article here