Introduction

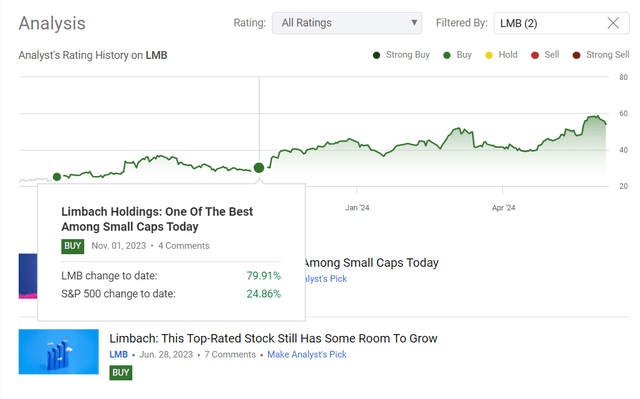

I’ve only written 2 articles on Limbach Holdings, Inc. (NASDAQ:LMB) since June 2023, but this stock has become one of my most successful picks here on Seeking Alpha – since the latest update, LMB is up a whopping 79% versus the S&P 500 (SP500) (SPX) Index of 24.86%:

Seeking Alpha, my coverage of LMB stock

As it has been six months since I last looked at LMB, I’d like to update my coverage today and look again at LMB’s future prospects – is there still potential for further growth in the stock?

Latest Financials And Developments

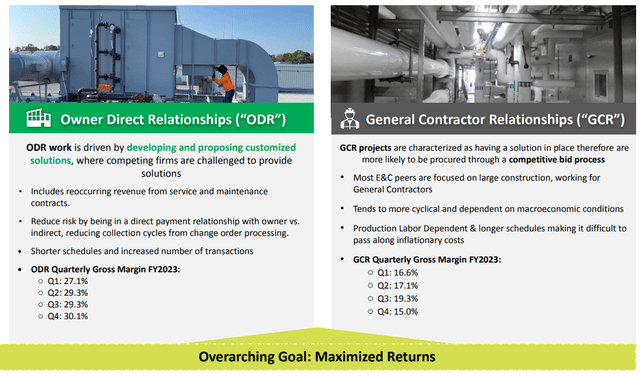

Limbach is a leading building systems solutions company specializing in mission-critical mechanical, electrical, and plumbing services. The company designs, installs, and maintains these systems in large buildings. According to the IR materials, Limbach operates in 2 segments: General Contractor Relationships (GCR) and Owner Direct Relationships (ODR), with GCR (construction and renovation projects that involve MEP services) accounting for 37.6% of total sales in Q1 and ODR providing construction projects directly to building owners or property managers.

LMB’s IR materials

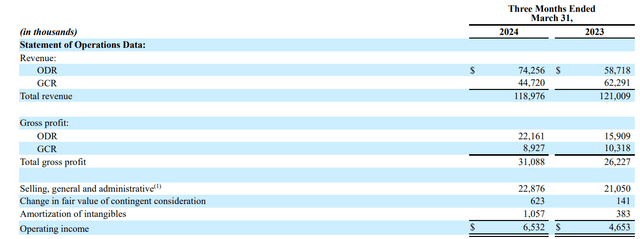

In Q1 FY2024, the company’s ODR segment experienced a significant revenue increase of 26.46% YoY, contributing $74.3 million, which represented 62.4% of the consolidated revenue and 71.3% of the total gross profit. Despite a slight decline in overall revenue to $119.0 million, total gross profit rose by 18.5% to $31.1 million, driven by higher margins in the ODR segment:

LMB’s 10-Q

In general, LMB is in the process of making a strategic shift from GCR to ODR in order to achieve higher margins for the consolidated business in the longer term. This apparently explains the decline in ODR revenues (and total consolidated revenues) in the first quarter – this is how management explained this dynamic during the recent earnings call:

Revenue was down slightly, which is a result of the intentional strategy to scale down the GCR business in favor of ODR and therefore, increase margins.

Despite the decline in sales, we see that this strategic shift is bearing fruit – the consolidated gross margin is growing quite rapidly (from 21.7% last year to 26.1% in Q1 FY2024), and due to the strong operating leverage, we also see EBIT growth of 40.4% year-on-year and an expansion of the corresponding margin from 3.85% last year to around 5.5% in the last reporting quarter.

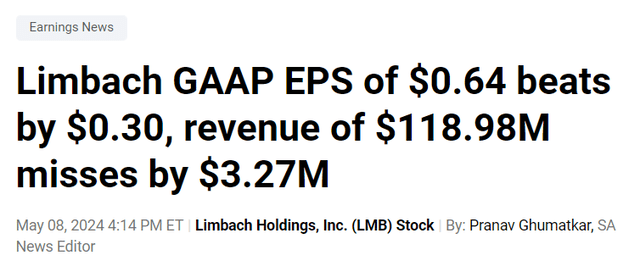

Net income in Q1 surged even more – by 153.5% to $7.6 million, translating to $0.64 per diluted share, which was more than enough to beat the consensus estimate even amid the missing top line:

Seeking Alpha, LMB

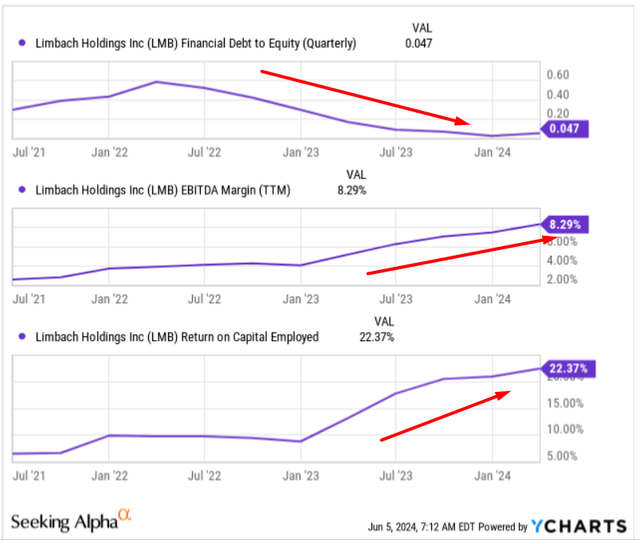

As far as I can see, the ODR focus is working well so far (take a look at the increased margins and profitability in general). Also, Limbach’s balance sheet remains robust, with $48.2 million in cash and cash equivalents and a current ratio of ~1.60 (above the generally accepted ratio of 1). The management plans to continue investing in the ODR segment “to drive further growth and value for shareholders, leveraging its strong financial position and disciplined business engagement” – based on these plans, I assume that we should see a continuation of the existing trends in terms of leverage and profitability shortly:

YCharts, the author’s notes added

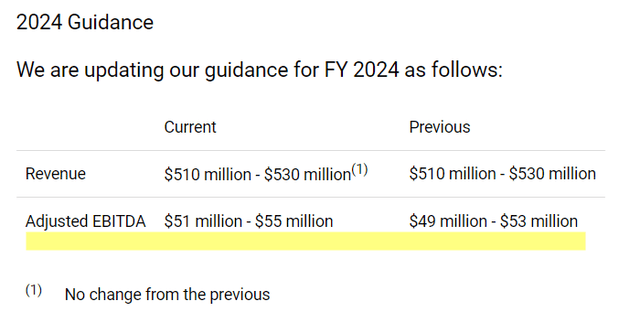

What’s also noteworthy is that Limbach revised its FY2024 adjusted EBITDA guidance upwards to a range of $51-55 million (3.9% higher, comparing the mid-range values), reflecting confidence in its strategic shift towards the higher-margin ODR business:

LMB’s press release, notes added

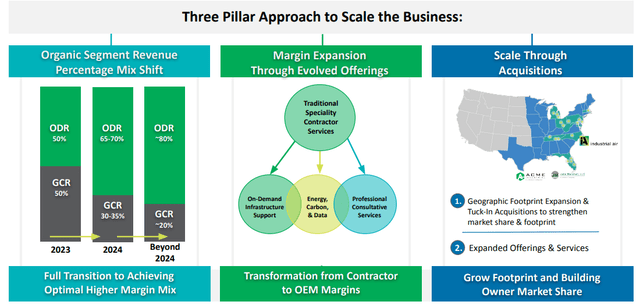

What I like about the LMB approach is the transparency of the business processes: Management sets clear targets for its near future and takes strategic steps that are easy to follow. For example, the latest IR presentation shows that LMB wants to generate 80% of its turnover coming from ODR beyond FY2024. What are they doing to achieve this? In addition to everything I described above, Limbach is actively buying other companies to expand ODR. During FY2023, Limbach acquired two companies for a total of $15.3 million – an industrial company from TN ($5 million) and an engineering company from NC ($13.5 million). Both firms will be managed in the ODR segment, further expanding LMB’s presence in the US.

LMB’s IR materials

In my view, LMB is growing and developing in the right direction: by tightly controlling liquidity and cash on the balance sheet, the company is moving smoothly into a higher-margin and economically stable segment, which, I believe, should lead to multiple expansion. But where is the fair price for LMB?

Limbach Stock Valuation Update

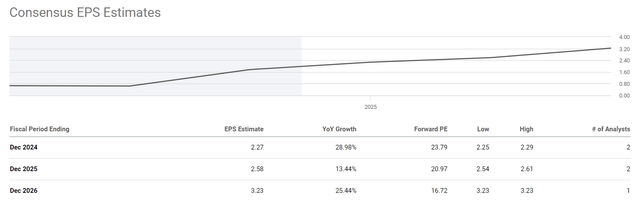

Let’s do the math together. If we assume that Limbach receives 80% of all revenues from ODR in 2024 and beyond and the margin of this segment remains at 28.9% (average of the 4 quarters of 2023), then gross profit for the full FY 2024 should be approximately $149 million (if the revenue consensus of $505 million is close to reality). Assuming that EBITDA/GP remains at the current level of 34.3% this year, we should achieve EBITDA of $51.1 million (+20% YoY) – this is within the management’s guided range but is not an adjusted figure. In other words, adjusted for individual items, adjusted EBITDA should be even higher. More than that, the net profit should be significantly higher, taking into account the existing operating leverage and the reduction in interest expenses. I don’t see analysts forecasting “much higher” EPS growth than what I just calculated with you.

SA, LMB’s EPS forecasts

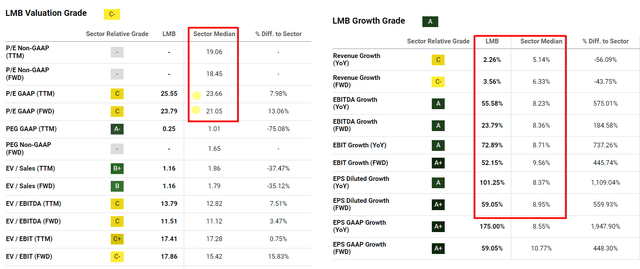

I expect LMB’s FY2024 EPS to be 15% higher as the company continues to beat estimates for the reasons outlined above. With projected EPS of $2.61, this gives an implied P/E of 20.7x – not that much considering that a) margins are rising and will only grow for the foreseeable future and b) the sector median is slightly higher, although LMB’s growth rates are several times higher than average.

Seeking Alpha, the author’s notes added

If we assume that LMB stays at the current P/E ratio of 23.8x until the end of the year, then the stock should trade at ~$62 with my projected EPS of $2.61. The “fair value” I arrive at is 15% above today’s market price – let this be my price target.

Risks To Consider

I am taking risks by reiterating my “Buy” rating on LMB today.

First, I cannot say exactly where the company has a ceiling in terms of gross profit margin. Perhaps we are already approaching it, and then it will be critically difficult for LMB to continue to show margin expansion, which could explain the increase in the valuation premium.

Second, the company’s business is highly dependent on economic cycles, and any downturn in the US economy could have a meaningful impact on Limbach’s business.

Third, the multiples that, I think, are fair – especially the current P/E ratio of 23.8x – seem quite high. The company may even miss its current EPS forecasts, which will most likely lead to a sell-off as the valuation already seems quite rich today.

Fourth, technical analysis shows the risk of a correction after LMB failed to gain a foothold above $59-60/sh recently. If there is a mean reversion to the 200-day moving average (which coincides with the medium-term trend level), we may see a 15% correction from the current levels.

TrendSpider Software, LMB (daily), the author’s notes added

The Bottom Line

Despite the abundance of risks, I try to look at Limbach from the point of view of facts and fundamentals.

- The company continues to grow EBITDA and EPS by focusing on higher-margin businesses;

- Management is raising its forecast for adjusted EBITDA, which could indicate that margins are growing even faster than previously assumed;

- LMB is actively expanding in various regions of the United States and is rapidly approaching its goal of achieving 80% of sales from ODR.

Based on my analysis of future EBITDA and EPS, I think LMB is still an undervalued company. In my opinion, the upside potential is 15%, but it could be even higher if management’s strategic plans are implemented faster than I expect.

So I maintain my “Buy” rating for LMB today.

Thank you for reading!

Read the full article here