Lyft (NASDAQ:LYFT) stock sold off massive after reporting its Q2 2024 results and outlook, pulling back over 17%, in spite of achieving its first-ever quarter of GAAP profitability. I reiterate my buy rating on Lyft, as I think Lyft is now better positioned to outperform in the second half of FY2024, as we’ve gotten the negatives out of the way. The stock sold off after earnings as investors panicked due to 1) a slight miss on gross bookings, coming in at a 17% increase year-over-year to $4.02 billion versus consensus of $4.07 billion and 2) 3Q24 soft guidance of gross bookings in the range of $4 billion- $4.1 billion versus estimates of $4.14 billion and adjusted EBITDA of $90 million – $95 million versus estimates of $104 million. What we learned this quarter was that my positive outlook proposed back in early May played out in terms of boosted rides due to customer obsession-based initiatives and lower net loss due to cost-cutting efforts, but it was not enough to offset the 25% decline in Primetime.

I think Lyft’s soft guide for Q3 is because management is preemptively pricing in headwinds from Primetime that could spill into the next quarter. I expect the new Price Lock initiative to counteract the Primetime headwinds as 3Q coincides with the summer travel season, back to school, and back to work. Additionally, the double-digit decline in Primetime, though not ideal in the short term, should help with rider retention and conversion in the longer term and translate to share gain for Lyft against competitor Uber (UBER).

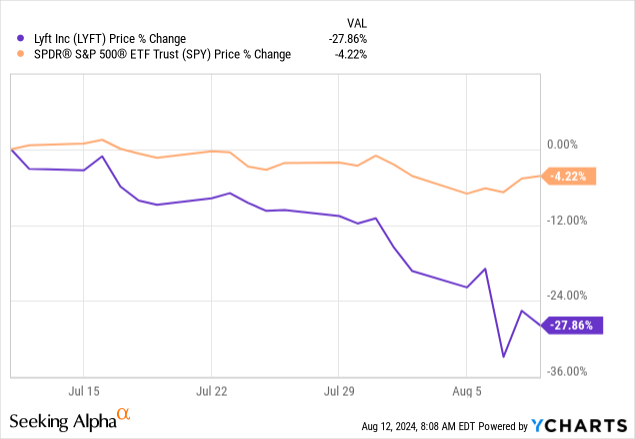

I continue to be optimistic about Lyft’s “go-to-market strategy under Risher will show more upside in 2024,” as per my last investment thesis. Management’s “customer obsession drives profitable growth” motto has been successful, especially through initiatives like Women+ Connect, on-time pickup promises, etc. I think the negatives on the conservative guidance have been priced in. As seen below, Lyft is down ~28% against the S&P500, down ~4% on the one-month chart. I believe the stock offers a small window for investors to jump in after the pullback, as I see limited downside risk from here and expect Lyft to be better positioned after its disappointing Q3 guidance to beat estimates next quarter.

YCharts

Financial Breakdown & Tailwinds Ahead

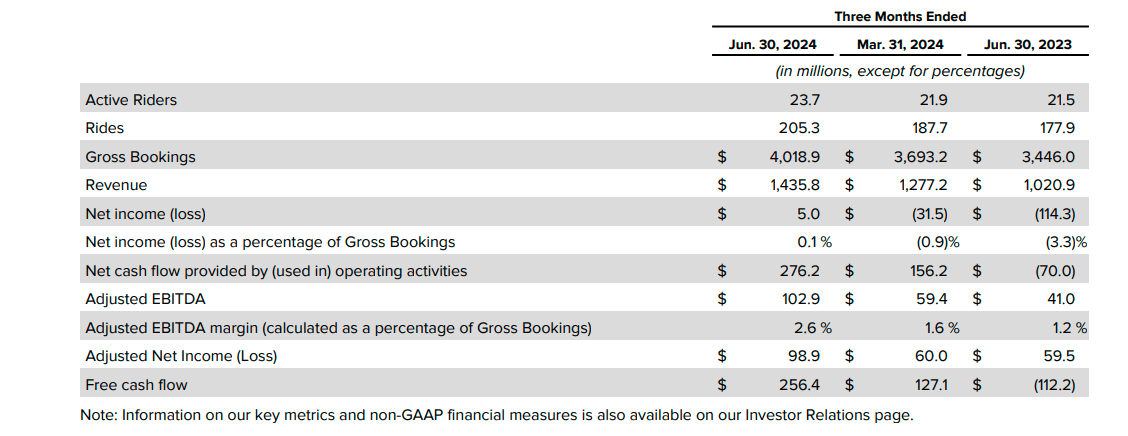

Lyft had a decent quarter across the board, with the exception of the gross booking miss and softer guidance. Revenue came in at $1.4 billion and was up 41% from a year ago quarter at $1.02 billion. I foresaw “management’s discipline with cost-cutting measures will pay off in lower net loss,” and this quarter’s net income came at $5 million and was 0.1% of gross bookings, while the company reported a net loss of $114.3 million and was 3.3% of gross bookings in a year ago quarter. Adjusted EBITDA came in at $102.9 million, significantly higher from a year ago quarter at $41 million. Free cash flow came in at $256.4 million, also higher year over year at a loss of $112.2 million.

Consistent with my expectations, active riders reached an all-time high of 23.7 million this quarter, up 10% year over year from 21.5 million. Rides reached a record of 205 million, 15% up from a year ago quarter’s 177.9 million. This was mainly due to driver hours also hitting an all-time high since 2019; I think this is in part due to the Women+ Connect initiative playing out. New drivers were the highest number the company had in any quarter since 2019, with over 34% more women and nonbinary drivers year over year. I think this is one instance where Lyft is showing commitment to its customer obsession, and I believe the numbers tell us that it’s working, although this is not yet being reflected in the gross bookings guidance.

Lyft 2Q24 earning results

Initiating “Price Lock”: Let the pricing wars continue

Lyft recognizes that “Primetime,” also known as Uber’s “surge pricing,” will always be part of its business. For context, this is an instance where prices become higher due to heightened customer demand or lower driver availability. So, to be more affordable than its biggest competitor, Uber, especially amidst the current economic headwinds, Lyft CEO Risher said the company would “open a can of whoop-ass on Primetime” through its new Price Lock initiative. The latter allows riders, specifically everyday commuters, to sign up for a monthly subscription that locks in a specific price for a fixed time and a route. I believe this is a good way for the company to match supply and demand. This quarter’s average Primetime decreased 25% year-over-year, and management is forecasting for further decline next quarter. I think my previous investment thesis on Lyft fell through because the positives of customer obsession-centered initiatives were not able to offset the lower Primetime. I think there will be limited downside from the Primetime headwind in the second half as management has factored for this headwind in its outlook and investors have factored it into the stock price. I expect that what is now a near-term pain will turn into a flex for Lyft in FY25 and enable the company to achieve better conversion rates. For example, the markets that witnessed the steepest decline in Primetime (Phoenix, Baltimore, Orlando) showed better improvement in conversion rates than in other markets.

As an underdog in the ride-hailing business, I believe Lyft is doing a good job of achieving profitability without taking it out of the customer’s wallet. I believe this puts them in a better position to keep up with Uber, which has also been keen to increase affordability through cheaper offerings and discounts. Management realizes that “reliable pricing is particularly important to them [customers] because they know what their ride should cost and hate it when prices change,” and I believe this customer obsession mindset is what differentiates Lyft from the peer group. Management wants to take one thing customers hate, Primetime, and turn it into a new selling point through Price Lock.

Lyft Media as a New leg for growth

The segment was announced in 2022 and is considered the advertising leg of the business. Lyft is monetizing the ad business through several outlets: Lyft Halo (rooftop screens), Lyft Tablets, Lyft Bikes, Lyft Skins, and the latest addition, Lyft in App, which uses personalized targeting, attention-grabbing formats, and measurable results.

Lyft Media revenue grew by around 70% year-over-year this quarter. This came as less impressive than last quarter, which had a 250% increase year over year. I believe what we’re seeing is the macro-uncertainty and headwinds with the roaming fear of a recession. Last quarter, Lyft added new customers, such as Zillow and Mastercard, as well as Nielsen and Oracle Advertising, as new partners for targeting purposes. This quarter, the company signed deals with 44 new brands, such as T-Mobile, and resigned with Amazon, Fidelity, and NBCUniversal. Lyft ad videos, a new addition to the media segment, generated over “10 times the ad industry’s typical click-through rate” and campaigns seven times “the impact relative to the norm, on-brand perception and purchase intent” last quarter. The in-app video ads “continue to drive interest from brands to power this growth,” with revenue growing over ten times year over year. This quarter’s new major partners include Google campaign manager, which, I believe, is Lyft’s way of seriously considering the media segment as the new leg of growth. I think the ad business could be more lucrative for Lyft and the broader peer group once macro uncertainty eases in 2025.

What could go wrong?

Macro uncertainty in North America could weigh on consumer discretionary spending and, by extension, active rides, making it more likely for riders to opt out of taking a Lyft or Uber for cheaper forms of transport. Uber’s regional diversification comes in handy to help offset the macro uncertainty facing North America in particular. Lyft doesn’t have that extra leg to stand on.

I think Lyft is focusing on consolidating its market share in the U.S. and Canada more, and I don’t think Lyft will need an international presence to drive near-term outperformance. The company is already making big achievements in the Canadian market, where rider and driver obsession is apparent. Lyft is in five of the largest cities in Canada and around 13 smaller ones. Canada ride came in double what they were in a year ago quarter, making Toronto their 8th largest market. Management believes this opens opportunities for Lyft outside the U.S. Lyft is taking its reach in North America seriously, which, along with all its new initiatives, gives it a near-term edge over Uber.

Valuation

According to data from Refinitiv, Lyft’s price/earnings ratio for C2024 is 13.5, significantly lower than the peer group average of 41.2. The stock’s EV/Sales ratio is also lower than the peer group average and substantially lower than its biggest competitor in the ride-hailing industry, Uber. In my opinion, Lyft is undervalued for what I estimate the stock’s near-to-mid-term value to be, and I think there’s more upside for Lyft than the market is pricing in at current levels.

Market sentiment on Lyft could be more positive. The current median PT is $15, revised down from the median of $18 in May and $19 throughout June and July. The current mean PT is $15.5, again revised down from a mean of $18.4 in May, $19.2 in June, and $18.9 in July. This isn’t a good look. Investors are reflecting a less-than-optimistic sentiment, as only ~7% of Street Analysts give the stock a strong buy, and 20.5% give it a buy. The majority of Street Analysts, making up over 65%, give the stock a hold, and around 2% give it a sell. This tells me that negatives from soft guidance are being priced in, and I expect the stock to rebound before next quarter.

The company held its Investor Day event in June last quarter, confirming my positive outlook on profitability and the customer-obsessed Lyft approach. This earnings call came in to say that Lyft is “well ahead of schedule” and said management is on track to “generate positive free cash flow for the full year, and given our strong progress in the first half of 2024 and our increased visibility, we now expect that more than 90% of adjusted EBITDA will convert to free cash flow for the full year 2024.” In my opinion, Lyft will continue to improve its financials and expand its domestic customer base in the second half of the year.

What’s next?

With the fear of Robotaxis taking over the ride-hailing industry, everyone wants a piece of the cake. Lyft is no different; the company believes that AVs pose a huge opportunity due to its network of over 40 million riders a year in Canada and the US and around 2 million rides a day. The said network is why Lyft succeeded in Las Vegas with its AV penetration and has secured over 130,000 AV rides so far. The company has had a “Flexdrive subsidiary” for years and now has around 15,000 vehicles working online. Honestly, aside from management’s “active conversations” with partners, I don’t expect this to be part of Lyft’s profitable endeavors in the near future. I also don’t think it causes any near-term risk to Lyft’s market share. I think it’ll be years before the world takes automotive means of transportation seriously in the ridesharing industry.

I’m also watching for the trend with Primetime and expecting conversion rates to show up in FY25. I think the second half of the year will help assess how successful the new Price Lock initiative will be.

Read the full article here