Summary

Madison Square Garden Entertainment (NYSE:MSGE) deserves a buy rating from me, as I view the secular tailwinds ahead very favorably. The growing demand for live events directly benefits MSGE, as it operates popular venues in the United States, and because of its exclusivity in operating them, MSGE has a dominant position in the local regions. Strong demand for venue bookings also provides more sponsorship opportunities, which further supports growth.

Company Overview

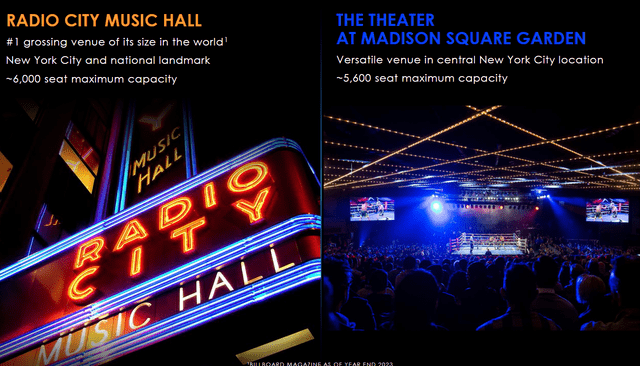

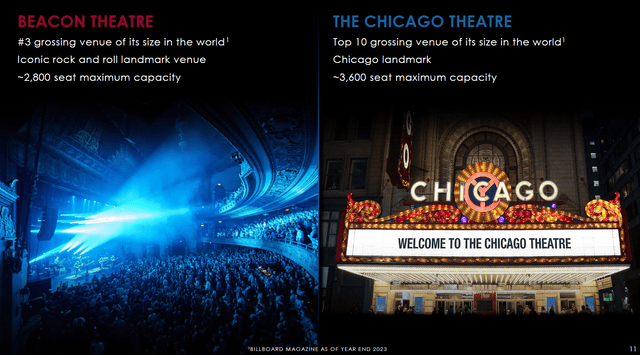

MSGE was a spin-off from Sphere Entertainment, and on a standalone basis today, the business consists of a collection of live entertainment venues and productions. The key venues that MSGE operates include Madison Square Garden, the Hulu Theater, Radio City Music Hall, the Beacon Theater, and the Chicago Theater.

MSGE

Direct Beneficiary of the Growing Demand for Live Events

I see an opportunity for MSGE to continue growing topline for the long term, easily in the high single-digits, given the (1) strong secular growth in the live entertainment industry and (2) sponsorship opportunities.

LYV

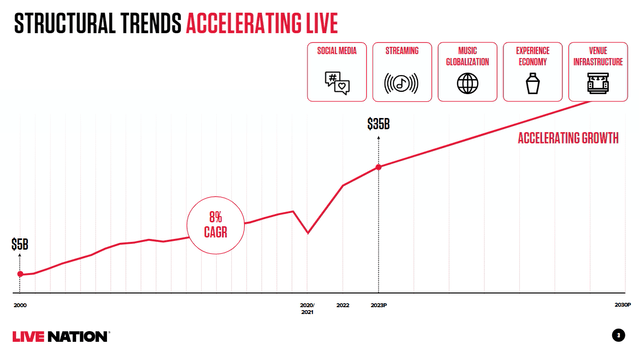

Consumer demand for live events has increased significantly over the last two decades and was not structurally impaired by COVID (as seen from the chart by Live Nation (LYV) above). In contrast, demand rebounded strongly back to the historical trendline, suggesting that underlying demand remains strong. Demand for more live events naturally leads to demand for venues, and the performers prefer to host their events at venues that are popular since it will attract more participants. MSGE fits the bill as it operates many of the most popular venues in the United States, in particular Madison Square Garden.

MSGE MSGE MSGE

This is a huge competitive advantage for MSGE because it either owns the venue (MSGE owns Madison Square Garden) or has very long-term lease agreements that prevent any competitor from competing effectively in the same region. To put it another way, MSGE has a dominant position in the local region where its popular venue operates.

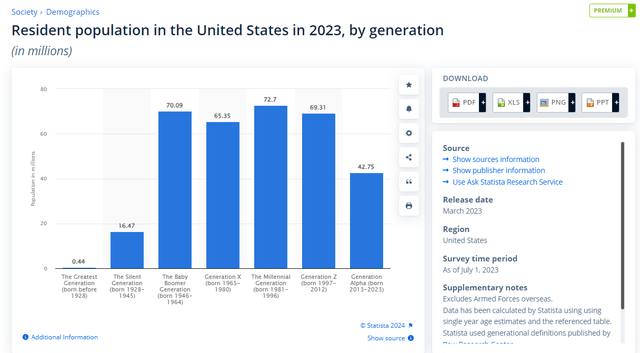

Statista

I hold a very positive view on the demand for live events over the long term due to demographics (the rise of the Millennials) and consumer spending tailwinds. For several reasons, the millennial generation is crucial to the live events sector. First, Millennials are the largest generational cohort in the US, which represents around 22% of the population in 2023 and is the largest generation group. Second, most Millennials have entered the workforce, which means that their wealth, income, and purchasing power will increase significantly in the coming years. Coupled with the fact that Millennials prioritize purchasing experiences, I think the demographic set-up for the live events industry is very bright for the coming years.

Instagram

There is another major growth tailwind that is driving Millennial demand for live events that was not present in previous generations – Social media. These days, live events wouldn’t be complete without including social media into the mix. This is due to multiple factors.

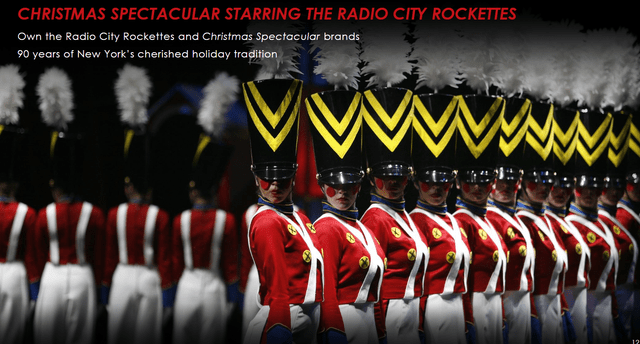

To start, social media allows eventgoers to record and share their presence at one-of-a-kind gatherings with their online friends and followers. Second, event marketers now have a tremendous weapon in social media to reach targeted demos with high-quality ads, and many people rely on it as a main source of information about new or upcoming events. Finally, many cultural icons, sports leagues, and musicians now use social media to connect with their fans on a personal level, which in turn increases attendance at live performances. As an example, MSGE uses its social media influence to promote the Radio City Rockettes, a dance company that has amassed a million Instagram followers and uses them to communicate with fans and find new performers.

LYV

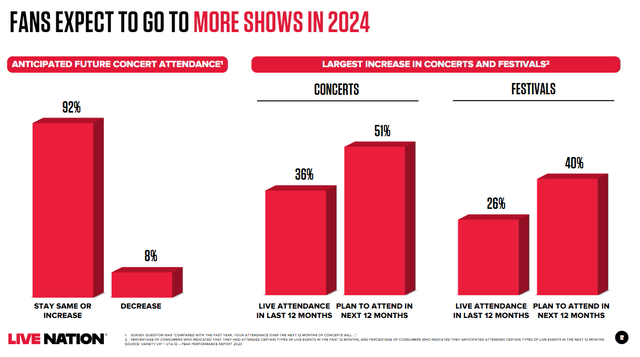

There might be a concern that there will be less demand in CY2024 because of the weak consumer spending environment. I don’t think this is the case. The data from LYV shows that consumer demand has not decreased; in fact, it has increased. The booking data that MSGE is seeing also suggests that demand remains very strong (data source from 3Q24 earnings report and call).

- Event bookings at The Garden are already trending ahead by mid-single-digit percentage for FY25 (vs. FY24), with 1FH25 trending in low-double-digit percentage vs. 1FH24.

- Sales of Christmas spectacular tickets for FY25 are also up 35% vs. FY24 as of 3FQ24, and this is before MSGE began actively promoting the FY25 season. This is a crucial data point because it suggests that organic demand has increased significantly, supporting the chart shown above.

- Importantly, the majority of concerts at its venues were sold out (viewed from another lens, which suggests that growth could have been better).

As such, I think the reality is that consumers are demanding more live events, and this trend should continue for the foreseeable future. I must reiterate again that this is despite rates staying at this high level (which supposedly is hurting discretionary spending). When the situation flips and consumers have more discretionary spending, I believe it could lead to more demand. The constraint would then be supplied, and encouragingly, MSGE is only operating at 70% utilization. Theoretically, MSGE could meet almost twice the current demand level.

Mentioned in the 3Q24 earnings call: We are very well positioned in terms of supply and demand here. On the supply side, we’ll do about 245 total events at the arena in fiscal 24, which as we mentioned previously would be internally a record for us. That does equate to about 70% utilization, relatively flat year over year. We’ve managed to minimize the number of loading days and we’ve had some success in having multi-event days.

Growing Demand Leads to More Sponsorship Opportunities

The indirect positive impact of more live events (which leads to more venue utilization) is that it creates more opportunities for sponsorship. In my opinion, live events and experiential marketing differ greatly from conventional means of advertising like television and the internet because of the personal connection that can be formed with fans through these mediums, which in turn can create cherished memories. As such, I believe that live music events in particular provide an opportunity for advertisers to connect with a more diverse subset of the overall population, including the increasingly important Millennial and Gen Z generations that conventional marketing methods cannot reach effectively.

Hence, I believe brand marketers will pay more attention to this channel, and if my expectations for live event demand come true, this segment of the advertising market should continue to capture advertising dollars from other avenues. MSGE’s recent financials are already showing that this is progressing as I expected. After a relatively stable FY24, management mentioned that the sponsorship segment will see increased renewal activity in FY25 and beyond. They also see opportunities to either increase pricing or expand upon their current deals with sponsors.

Valuation

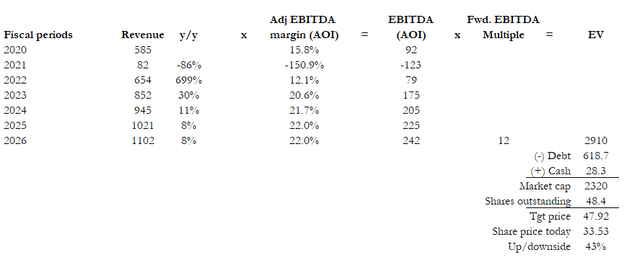

Source: Author’s calculation

The upside is attractive at this share price. Using my model estimates of 11% growth for FY24, 8% growth for FY25/26, and EBITDA margin of 22% in FY26, I believe MSGE could be worth $48 in FY26. Following are the reasons for my assumptions: (1) Since 3 quarters of FY24 financials are already out and MSGE has visibility into near-term demand, FY24 guidance should be reliable; (2) As I noted above, high-single digits top-line growth is possible because of the strong secular tailwinds; (3) I am assuming that utilization rates stay at 70%. However, if demand exceeds my expectations (could be due to rates cut), margins could go higher as incremental utilization carries high margins; (4) Compared to other peers in the entertainment industry like Walt Disney (DIS), Six Flags Entertainment (SIX), Cedar Fair, L.P. (FUN), and IMAX (IMAX), MSGE valuation at 12x forward EBITDA seems reasonable as its growth profile is similar (peers are mid-to-high-single-digits growth and trade at ~10.5x forward EBITDA).

Investment Risk

The biggest risk for MSGE is losing its rights to operate the key venues I listed above. Last year, the NYC Council committee only extended MSGE to operate Madison Square Garden for five more years. The fear is that the rights are not extended. As of the current data available, demand for live events remains strong. However, this is not to say that demand will not plummet in a major recession. Given the high fixed-cost nature of the business, a sharp drop in demand will decimate earnings, as seen in FY21.

Conclusion

I see MSGE as a compelling investment due to the powerful secular tailwinds driving the live entertainment industry. The growing demand for live events directly translates to increased venue bookings and sponsorship opportunities for MSGE. MSGE’s strong competitive advantage, with its popular venues and long-term leases, also effectively gives it a leading position in the local region.

Read the full article here