Marine Products (NYSE:MPX), the fiberglass powerboat manufacturer selling under brands such as Chaparral, Robalo, and SSX, has faced significant financial turbulence in the two quarters reported after my previous article on the stock.

In the previous article, published on the 16th of December 2023 with the title “Marine Products: Expecting A Storm Ahead”, I initiated Marine Products at hold despite a moderate estimated undervaluation – I noted that further financial turbulence, potentially varying widely from my estimates at the time, would be likely. Industry turbulence has since deepened, also worsening Marine Products’ revenues, but the company continues to post stable earnings. The stock has had a total return of 2% after my previous article, with S&P 500 (SP500) returning a higher 13% now, making the stock a more attractive opportunity.

My Rating History on MPX (Seeking Alpha)

Waiting for an Industry Recovery

After the Covid pandemic peak in demand, the boating industry has been left in crumbles as interest rates have risen. Manufactures have taken an especially large hit as dealerships are churning through excess inventories bought during the pandemic. While significant signs were already seen in December as of my previous article, the struggles have widened into a dramatically wider level than anticipated at the time – in my previous article’s DCF model, I anticipated revenues of $340 million in 2024, but the current outlook seems significantly worse with Wall Street analysts now estimating revenues of $274.2 million for the year.

The company’s Q4 and Q1 results showed significantly declining demand, with Marine Products reporting a revenue decline of -34.7% and -41.7% in the quarters, respectively. The Q4 report shocked analysts as reported revenues were over a third below the anticipated level, also worsening the EPS into a half of the expected figure.

The weakness isn’t related to Marine Products alone, and the company’s revenues have performed in line with publicly traded peers such as Malibu Boats (MBUU) and MasterCraft (MCFT). An industry recovery is likely to eventually raise boat manufacturers’ revenues into a clearly better level, and it seems that interest rates play a key part in an eventual recovery. A good share of customers purchase boats with financing, and higher interest rates have deterred potential customers from purchasing. In addition, dealerships’ floor plan financing has become more expensive, making leaner inventory management favourable. Interest rates in the United States have continued to relatively high, but are still down slightly from the peak. Marine Products continues to expect continued softness in the short-term.

Margins Have Been Incredibly Resilient

Despite revenues figuratively falling off a cliff in recent quarters, Marine Products’ margins have remained impressively high – the company’s history of great operating leverage doesn’t seem to reverse backwards too much with lower revenues. Marine Products’ current operating margin trails at 12.1% after Q1, above the 2019 level of 11.7% despite industry weakness. The margin is only 1.8 percentage points below the 2022 peak of 13.9%.

I anticipate that margins will fall further in the short term, but still only into a continued healthy level. In the two latest reported quarters, the operating margin has fallen by 6.5 and 4.5 percentage points year-over-year respectively, and such a performance should continue in upcoming quarters. Still, the strong overall margin performance in dry demand raises my longer-term margin estimates.

It must be noted that capital expenditures have risen from a previously consistently low level into $10.2 million in 2023 – more expenses have been capitalized as investments in the year. In the Q4 earnings call, Marine Products relates the capex to warehouse investments and new trailers. Investments were mainly high in Q2/2023 with $5.4 million and have fallen into a more historical level in more recent quarters.

Strong Balance Sheet Leaves Marine Products with Options

Marine Products’ balance sheet is incredibly strong, with $81.2 million in cash and no interest-bearing debt. The cash position represents over a fifth of the company’s market cap at the time of writing, leaving the company with options for a potentially large excess dividend, share repurchases, or M&A. The company has hinted at the potential of an acquisition or organic investments in recent quarterly reports as a use to the excess capital. Marine Products doesn’t have a history of M&A or very large share repurchases, though, and I wouldn’t expect strategic use of the capital very soon as a base scenario. For the time being, Marine Products earns interest income on the excess cash, with $3.2 million earned in the past twelve months.

A part of the cash is also likely reserved to navigate the currently stormy waters, and recent working capital decreases could reverse tying up cash.

Valuation Is Now Highly Attractive

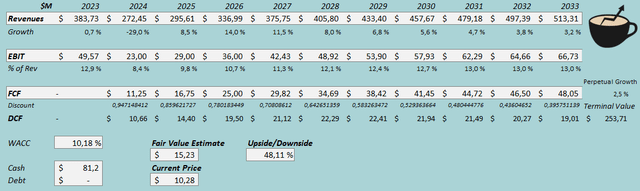

Revenues have performed worse than I previously anticipated, and I updated my discounted cash flow model (DCF model) accordingly – for 2024, I now estimate revenues of $272.5 million compared to $340.0 million previously. In following years, I now estimate a gradual recovery to start in 2025 and continue stronger in 2026 with 14.0% in the year. The revenues in 2024 end up at $337.0 million, representing a CAGR of only 2.1% from 2019 prior to industry turbulence. Afterwards, I estimate good continued growth that slows down gradually into a perpetual growth of 2.5%.

Due to great margin resilience, I estimate better continued operating leverage. Despite a weaker short-term margin outlook at an estimated 8.4% EBIT margin in 2024 due to weak revenues, I now estimate the margin to gradually increase into 13.0% compared to 11.7% previously. Marine Products’ cash flows continue to be stable and very healthy.

DCF Model (Author’s Calculation)

The estimates put Marine Products’ fair value estimate at $15.23, 48% above the stock price at the time of writing. The estimate is up from $13.51 previously, and combined with a slightly lower stock price, the stock now seems highly attractive. The valuation’s attractiveness still relies on an industry recovery in the mid-term, which I do see as very likely. Changes to the recovery thesis could happen, though, as the demand slump has already deepened from my previous estimates.

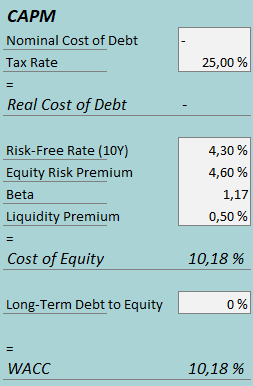

A weighted average cost of capital of 10.18% is used in the DCF model. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

I continue estimating no interest-bearing debt for Marine Products with the strong balance sheet. To estimate the cost of equity, I use the United States’ 10-year bond yield of 4.30% as the risk-free rate. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the United States, updated on the 5th of January. I have kept my beta estimate the same at 1.17. Finally, I add a liquidity premium of 0.5%, creating a cost of equity and WACC of 10.18%, down from 11.32% previously due to a lower equity risk premium.

Takeaway

Boat manufacturers’ headwinds have continued to worsen beyond previous expectations. Marine Products reported Q4 revenues shocking estimates, and Q1 continued with an even more dramatic revenue decline as the industry continues to experience low demand from dealerships due to weak customer demand and more cautious inventory management. Marine Products’ revenue declines are still largely in line with peers in the industry, and the company has demonstrated incredible margin stability despite the revenue weakness. An eventual industry recovery should boost Marine Products’ earnings in the mid-term into a highly attractive level at the current price, largely dependent on interest rates. The stock now seems to be undervalued considering the earnings rebound potential, and as such, I upgrade Marine Products into a Buy rating.

Read the full article here