Although I have a really solid track record when it comes to investments, not every call that I make turns out to be a winner. And some calls are very ambiguous for an extended period of time because, for a while, they can move in the opposite direction from what you think for a while. Distinguishing between what is ultimately a loser and what ultimately is a firm that just requires additional time to play out is incredibly important. And one company that I could point to that seems to be teetering on the edge between these two categories is Markforged Holding Corporation (NYSE:MKFG), and enterprise that operates as an additive manufacturer that helps clients with their 3D printing needs.

Recently, shares have taken a beating, even as revenue for the company continues to grow. The bottom line for the company has suffered, but cash flow data is showing signs of improvement. Normally, a company that’s still generates significant cash outflows would be one that I am bearish on. But given the massive amount of cash and cash equivalents on its books, I also recognize that the company has plenty of fuel that it can utilize an order to get where it needs to be. At the end of the day, this is a tough investment to call. But because of the tremendous amount of cash that it has, I do believe that near term risk for shareholders is quite limited. So even though the company may not be anything close to a prime prospect, I do think it still warrants a ‘hold’ rating at this time.

Putting recent pain in perspective

The past several months have not been particularly kind to Markforged or its shareholders. Since I last wrote about the company back in January of this year, shares have plunged 19.4%. That is a significant departure from the 12% increase seen by the S&P 500 over the same window of time. Had I rated the company bearishly, you could imagine my elation at this return disparity. But unfortunately, I ended up rating the company a ‘hold’ to reflect my view at the time that the stock should perform along the lines of the market for the foreseeable future. At that time, I recognized that bottom line results for the company were far from great. Yes, revenue had been climbing nicely. But with earnings and cash flows deeply in the red, the picture was not looking great. Having said that, the stock looked incredibly cheap, especially after factoring in the fact that the business had no debt and had cash and cash equivalents of $181.8 million. That brought its enterprise value at that time down to only $91.5 million.

Author – SEC EDGAR Data

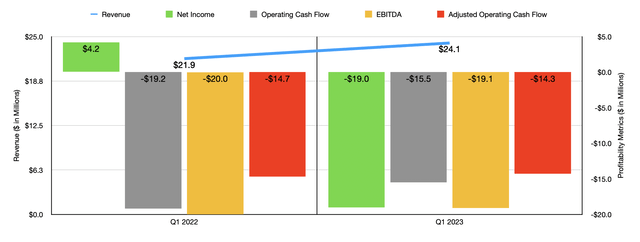

The rationale behind my stance on the company really centered around the idea that it wouldn’t take much in terms of profitability to see the company worth at least enough to keep from falling. Unfortunately, in some respects, the picture has worsened since then. To see what I mean, we need only touch on data covering the first quarter of the company’s 2023 fiscal year. Let’s start with the good news first though. According to management, revenue for the quarter came in at $24.1 million. That was up decently from the $21.9 million generated the same time one year earlier.

In absolute dollar terms, the biggest impact for the company on the sales side involved its consumables. Revenue there spiked about 18%, or roughly $1 million, climbing from $5.5 million to $6.5 million. This increase, according to management, was driven largely by a rise in active printers being utilized in the field because of more units having been sold from one year to the next. Personally, I view consumables revenue as a huge driver for the company in the long run. While the hardware sold by the firm brings in big dollars, it should be considered low margin in nature and it’s a purchase that customers only make once every several years. But consumables are required in order to see that hardware continue to be useful.

Services, meanwhile, are also great to see an increase from because of how high margin those should be. And we did see a 29% spike there. For only 10.1% of overall revenue, they will never be the big money maker for the company. As a sign of long-term growth, investors should also pay attention to hardware revenue. The more hardware that’s sold today, the more services and consumables the company will provide in the future. This growth was a bit on the light side, coming in at only 5% year over year. Management said the overall unit sales decreased. But this was made-up for by the fact that the higher price point next generation printers became popular.

On the bottom line, this is where things get a bit mixed. Net income, for instance, took a real beating. The metric went from $4.2 million to negative $19 million. This was in spite of the fact the operating expenses as a percent of revenue dropped from 150% to 137%. The real pain on the bottom line, then, came from the fact that, in the first quarter of 2022, the company had a $24.9 million benefit associated with a contingent earn out liability. This compared to only $808,000 worth of a benefit seen the same time this year. When you look at other profitability metrics, meanwhile, you start to see some real areas of improvement. Operating cash flow went from negative $19.2 million to negative $15.5 million. On an adjusted basis, it ticked down from negative $14.7 million to negative $14.3 million. Meanwhile, EBITDA went from negative $20 million to negative $19.1 million.

Author – SEC EDGAR Data

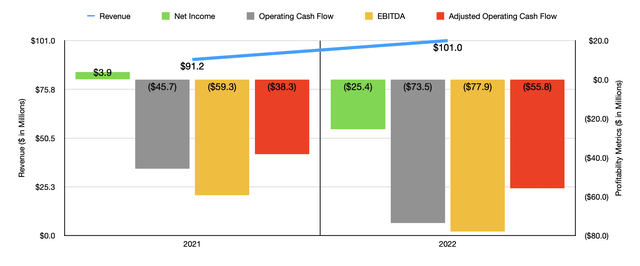

As you can see in the graph above, the results seen in the first quarter of this year do mark something of a turnaround for the most part compared to what the company saw in 2022 relative to 2021. And when it comes to the rest of 2023, management expects this trend to continue. Overall revenue for 2023 should be between $101 million and $110 million. That’s not as strong of growth as I would like. But it’s better than nothing. What really struck me is that management is forecasting an operating loss of between $55 million and $58 million. If that comes to fruition, it would represent a nice improvement over the $87.1 million operating loss the company experienced in 2022. It would even be better than the $61 million loss the company reported for 2021.

This anticipated improvement looks really promising. But that doesn’t change the fact that you can’t really value a company that’s generating negative results like this. The best thing you can do is figure out what kind of profit and cash flow picture would make shares at least fairly valued. In the table below, I did precisely that. I calculated the amount of operating cash flow that the company would need to generate an order to trade at a price to operating cash flow multiple of 10. I did the same thing with EBITDA for the EV to EBITDA multiple. From the air, I repeated the process to see what the picture would need to look like for these multiples to be 20 or 30.

Author – SEC EDGAR Data

When you look at the EV to EBITDA multiple picture in particular, you can understand why I’m not terribly bearish on the company. Profitability in the single digits is all that’s needed in order for the stock to be fairly valued. That’s not all that large a bridge to cross, especially as the company’s revenue continues to grow.

Takeaway

Operationally, things are not the best for Markforged right now. However, the firm is making progress on both its top and bottom lines, as evidenced by its most recent quarterly results. It won’t take much in the way of profits for the enterprise to reach fair value, or perhaps even become undervalued. Add on top of this the $151.4 million in excess cash on the company’s books, and I do believe that a ‘hold’ rating is still appropriate for now. But if the company does see its bottom line results worsen from here, I could definitely understand a downgrade.

Read the full article here