Matrix investment thesis

Engineering, construction, and maintenance firm Matrix Service Company (NASDAQ:MTRX) was a victim of the COVID-19 pandemic and its subsequent fallout. Its revenue dropped off, it slipped from profitability into losses, and the share price lost 45% over the past five years.

The company now appears to be headed to higher revenue and profitability. Backing up that opinion are financial improvements in recent quarters, a large backlog of orders, the capture of deferred revenue, and tailwinds.

I have rated Matrix a Buy, and have a one-year price target of $15.30, an increase of more than 50%.

Matrix history and operations

The company was founded in Tulsa, Oklahoma in 1984, and provides engineering, fabrication, construction, and maintenance services. It serves the critical energy and industrial markets in 50 states and four Canadian provinces, according to its 10-K for fiscal 2023.

Business goes through three reportable segments:

- Storage and Terminal Solutions: Engineering, procurement, fabrication, and construction services related to cryogenic and other specialty tanks and terminals. These facilities handle LNG, NGLs, hydrogen, ammonia, propane, butane, liquid nitrogen/liquid oxygen, and liquid petroleum. It also does work involving traditional above ground crude oil and refined product storage tanks.

- Utilities and Power Infrastructure: Main business is services that support LNG utility peak shaving facilities. This segment also works for public and private utilities, taking on projects such as new substations, transmission, and distribution line installations.

- Process and Industrial Facilities: Focused on plant maintenance, repairs, and turnarounds in downstream and midstream facilities. This includes clients that refine and process crude oil, fractionate, and market natural gas and its liquids.

It had about 400 customers in 2023, but only one of them accounted for more than 10.0% of consolidated revenue (10.7%).

Its operating results reflect the seasonality inherent in some of its businesses, and especially the Process and Industrial Facilities segment. Many plant outages and turnarounds are scheduled in spring and fall when there is less energy demand.

Seasonality also involves energy demand levels, as well as extreme weather, including hurricanes, snowstorms, and unusually high or low temperatures.

Matrix’s fiscal years end on June 30, and ‘fiscal year’ refers to the end of the period.

At the close on Tuesday, July 30, it traded at $10.07 and had a market cap of $275.82 million.

Competition

According to the 10-K, it competes with local, regional, and national competitors.

Based on an online search, major EPC (engineering, procurement, and construction) companies include White Construction, Mitsubishi Heavy Industries (OTCPK:MHVYF)(OTCPK:MHVIY), and SOLV Energy.

Matrix reports that it competes for most contracts, but some come out of “preferred provider relationships”, through long-term agreements. Contracts are usually based on price, quality, safety performance, schedule, experience, and customer satisfaction.

Judging by its profitability margins and return on common equity, the company does not have much of a moat (Matrix versus Industrials sector medians):

- Gross margin [TTM]: 5.74% versus 31.21%

- EBITDA margin [TTM]: -2.09% compared to 13.70%

- Net income margin [TTM]: -2.81% versus 6.12%

- Return on common equity [TTM]: -12.11% versus 12.62%.

Note that both the net income margin and return on common equity are negative. These results help explain why the share price has been shrinking.

Third quarter financial results

Matrix reported its third quarter earnings results (that ended on March 31), on May 8:

- Revenue was down 11% year-over-year, at $166.0 million.

- Adjusted EBITDA declined to ($9.8) million from ($7.7) million during the same quarter last year.

- Net loss per share was $0.53 versus a loss of $0.47 last year.

But there were also a couple of pieces of encouraging news:

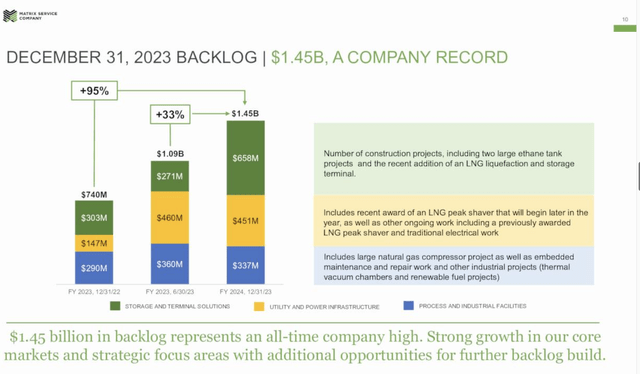

- Total backlog rose 74% over last year, to $1.45 billion, a record for the firm.

- Cash flow from operations grew 25% year-over-year, to $25 million.

- Cash and credit facility available was $135 million.

- It continued to be debt-free.

President and CEO John Hewitt stated, “Bidding activity remained strong across our end-markets during the third quarter, driven by multi-year tailwinds that continue to support backlog growth within our core storage, terminal, utility and power infrastructure markets”.

Comments: Before 2021, Matrix routinely generated billion-dollar plus revenue, and hit a high of $1.416 billion in 2019. Since then, it has produced revenue ranging from $673 million (2021) to $795 million (2023). On a TTM basis, it currently stands at $744.6 million.

It has been improving its basic and diluted EPS. Matrix had its first profitable year in the past decade in 2019 when it posted a positive $1.04. The following year, 2020, pandemic fallout led to a loss of $1.24 and losses continued to grow until they hit $2.39 in 2022. Last year, fiscal 2023 brought an improvement, but continuing loss, of $1.94. On a TTM basis, the loss per share is now down to $0.77.

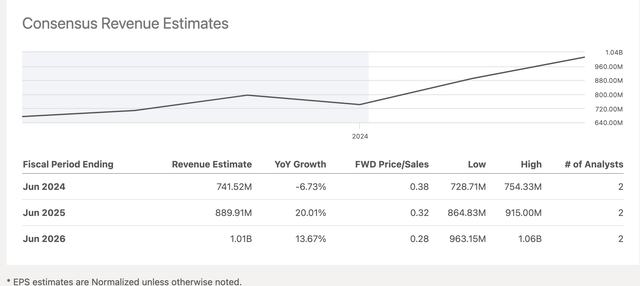

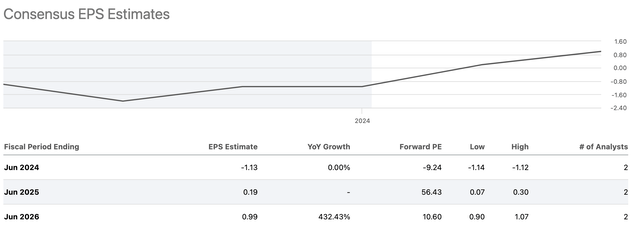

Analysts expect revenue to start growing again in fiscal 2025, and that profitability will return in that year, so this quarter’s earnings improvement is another step on the way to consistent profitability.

One of the firm’s tailwinds is the Infrastructure Investment and Jobs Act, which has provided $1.2 trillion for projects such as electric grid renewal. It has provided cash for new and upgraded facilities that comprise America’s infrastructure.

Growth

CEO Hewitt suggested the revenue and earnings weakness in the third quarter largely reflected one-off issues. Part of it, he argued in the Q3-2024 earnings call, was due to “the complexity of finalizing large capital construction project contracts”. He added those projects should begin providing additional revenue in Q4 and throughout fiscal 2025.

Another reason was that a multi-decade refinery client pulled back its spending for the third quarter and the remainder of its contract. He also reported softness in two core markets, crude tank new builds as well as maintenance and repair, and electrical infrastructure in the Northeast sector.

Hewitt went on to say, “In short, we expect revenue to improve from here and continue to build through fiscal 2025. As this increased volume of projects and backlog and new awards convert to revenue, we expect to drive improved fixed cost absorption and margin expansion toward our historical double-digit levels.”

A second tailwind is the clean energy transition. Hewitt explained that his company is one of “the very few” that has the cryogenic experience required to complete infrastructure for LNG, ammonia, hydrogen, and other renewable fuels.

A third is data center growth, which he says leads to higher electricity consumption. Hewitt argues that the company is well positioned to benefit from incremental data center load growth, which drives demand for new infrastructure investments.

Internally, the firm has a robust and growing backlog, as shown in its Q2 earnings presentation:

MTRX – backlog graphic (Matrix Q2 earnings presentation)

The challenge with the backlog is to turn it into revenue and earnings.

All of that led Hewitt to say on the conference call that Matrix expects to see gains on both the top and bottom line in the fourth quarter in fiscal 2024.

That optimism is shared by the Wall Street analysts, who also expect material improvements:

MTRX revenue estimates table (Seeking Alpha )

Similarly, they see increases in earnings per share, with Matrix becoming profitable in fiscal 2025 and a large EPS jump in fiscal 2026:

MTRX EPS estimates table (Seeking Alpha )

Patient investors should do well if they stick with the company for at least the next few years.

Valuing Matrix shares

If that growth scenario plays out, long-time investors will get some relief from a decade of mostly falling share prices and capital losses:

Matrix has operated at a loss for most of the past five years, and so conventional valuation metrics such as Price/Earnings and the PEG ratio are unavailable. A couple of other metrics can provide some valuation guidance, though:

MTRX Valuation ratios table (Seeking Alpha )

The first column to the right of letter grade is the Matrix ratio, the second lists the sector median, the third shows the percentage differences, the third column shows the firm’s five-year average, the fourth shows the sector’s five-year median, and the fourth shows the difference between the latter two.

Focusing on the letter grades, we see the firm gets A grades for Price/Sales, both TTM and Forward. Price/Book and Price/Cash Flow produce Bs. Those grades suggest the stock is currently undervalued.

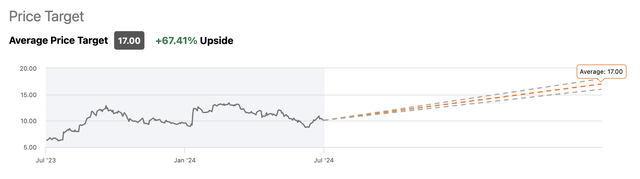

Wall Street analysts, who posted bullish earnings estimates, have a price target of $17.00:

MTRX analysts’ one-year price target (Seeking Alpha )

However, the analysts have a history of overvaluing Matrix:

MTRX Target prices versus actual prices (Seeking Alpha )

So I will trim that target by 10% to compensate. That makes my one-year price target $15.30 ($17.00-1.70).

That’s still an ambitious target, a gain of 51.49%. But, it’s also a reasonable target given the recovery underway in recent quarters, the large backlog of orders, capturing deferred revenue, and tailwinds.

I rate Matrix a Buy (the only current Seeking Alpha rating). The Quant system gives it a Hold, while the Wall Street analysts have one rating, a Strong Buy.

Risks for Matrix shareholders

My Buy rating and the Wall Street Strong Buy rating may overestimate whether or how soon Matrix will reach profitability and start generating sustained positive earnings. While internal factors seem aligned for growth, external factors may cause reversals.

As the company pointed out in the 10-K, its revenue originates from contracts awarded on a project-by-project basis, which leads to uncertainty. In addition, there are always timing uncertainties involved in contract bidding and execution. To some extent, though, these concerns are mitigated by its large backlog.

It operates in a cyclical environment, especially in its dealings with the energy industry. Slowing demand reduces capital spending on LNG, hydrogen, renewable energy, midstream and downstream petroleum projects. Again, having a backlog is a mitigating factor.

The work Matrix performs requires qualified personnel. As it notes in the 10-K, engineers, project managers, skilled craftsmen, and other experienced professionals are critical. Many industries are currently constrained as Baby Boomers retire.

There are relatively few customers in its markets. As noted above, its market comprises about 400 customers, so the loss of one or more of them could have adverse effects on its financial results.

Conclusion

It appears Matrix Service Company is about to see the fruits of its turnaround materialize. In the fourth quarter of 2024, it expects to see further improvements in its net income and earnings per share.

Fiscal 2025, which will end on June 30 of that year, should see revenue start rising again, and the company finally return to profitability. Beyond that, Wall Street analysts see surging profitability.

Given the positive signs and potentially profitable growth, I rate Matrix a Buy.

Read the full article here