In early August I published my 4th article on Medical Properties Trust (NYSE:MPW), in which I urged readers not to buy the heavy 14% dip after the Q2 results announcement. As time has shown, that recommendation has proven correct: MPW is down 43.71% [total return] since that call:

Seeking Alpha, author’s previous article on MPW

And, as is often the case, such a sharp correction led to even more positivity among some analysts and many retail investors, who see a 30% discount to assets and believe that the existing undervaluation should be bought up with both hands.

Today, once again, I urge everyone to be extremely cautious with MPW and avoid this company, because, in my opinion, the worst could be yet to come.

Why Do I Think So?

First off, let’s take a look at Q3 FY2023 numbers and management commentary around them.

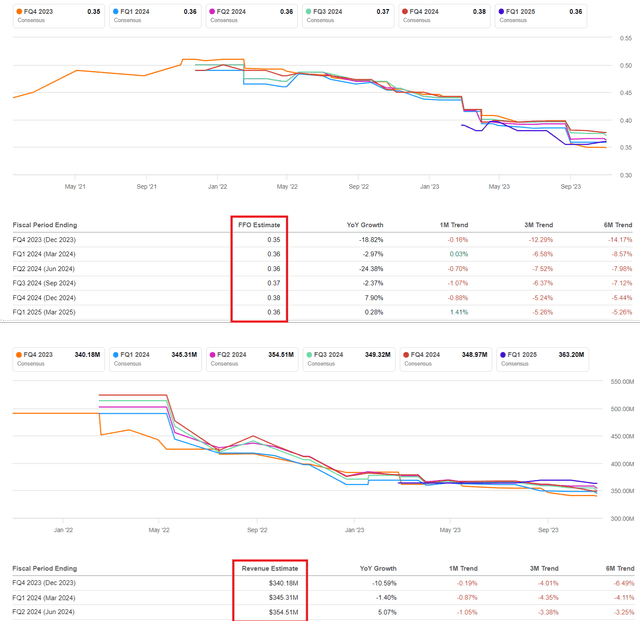

MPW reported a Q3 net income of $0.19 per diluted share (in line with consensus) and Normalized Funds from Operations (NFFO) of $0.38 per diluted share. In terms of revenue, the company missed estimates by a wide margin: actual revenue was 10.3% below initial expectations:

Seeking Alpha, MPW’s Earnings Summary

According to the earnings call commentary, over the past 18 months, MPW executed ~$3 billion worth of asset sales, which had a dilutive effect on AFFO (Adjusted Funds From Operations).

The net cash impact of acquisitions and divestitures since the end of 2021 was approximately a negative $0.21 per share, and there was an additional negative $0.16 per share impact from prospect recapitalization transactions. As a result, the company reduced its dividend level to maintain a near-term AFFO payout ratio below 60%, preserving ~$335 million of cash per year. Notably, MPW had already repurchased notes due in December and closed the sale of its Australian facilities for ~$305 million.

The company announced its strategy to enhance liquidity by targeting ~$2 billion in liquidity transactions over the next 3-4 quarters. These transactions could involve asset sales, joint ventures, secured financing, or amendments to certain bank loans. MPW would use the proceeds to reduce revolver balances and potentially repurchase unsecured notes.

MPW narrowed its FY2023 guidance for per-share net income to $0.36-0.38 and per-share NFFO to $1.56-1.58. These estimates are based on the existing portfolio, and they do not include the effects of unexpected costs, changes in lease terms, market conditions, or other non-recurring/unplanned transactions.

To me, if a company cuts its dividend because it needs to cover its debt, that in itself is not good: that certainly can’t be called “strong” operating activity. Analysts at Hedgeye calculated that management used the word “strong” phrase 13 times in their prepared comments during the earnings call – more than three times the number of times they used it in the last quarter. Just a fun fact for your consideration.

MPW’s executives mentioned during the Q&A session that Steward’s denials have been higher than desired, but they are working on addressing that issue. I can’t imagine how exactly the Steward team is working on this problem, so I don’t see any positive (much less “strong”) progress from their side here.

If you recall, MPW’s stock price got a big boost when the Q3 earnings press release just came out:

But management’s comments could not support this trend and ultimately the market’s distrust seems to be winning again:

The market reaction after the earnings call tells me that the professional market participants do not like what is happening to MPW and how its management elaborates on different aspects of the business decline. And if we look at the number of institutional investors in this REIT’s ownership structure, we find that there are still 1,255 funds holding MPW in their portfolios, according to YCharts data. That’s a lot – many times more than MPW’s peers:

Therefore, I believe that if things continue as they are, we may see a continued mass exodus of institutional investors from their positions and a subsequent rotation of the freed-up assets within the industry (or outside of it). That is, the supply side is still strong, no matter what anyone says.

Then why don’t I give a “Sell” rating?

Because I assume that when we see the funds’ sales, they are most likely to be made on so-called “rips,” when an asset experiences a significant increase in a short period because it is oversold or for other reasons. In the case of MPW, it is strictly speaking oversoldness and a huge percentage of shares already sold short that will have to be covered at some point:

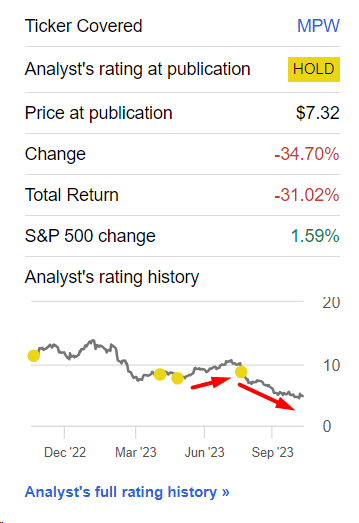

I already wrote in my May article that high short interest in itself should not be a reason to buy MPW. At that time, short interest was 18.65%, but since then the stock has fallen 31% (total return) after its short-lived rally from $7 to $10.

Seeking Alpha, author’s notes

At the same time, we can talk all we want about the discount at which MPW is trading relative to its assets, prospective earnings, etc. But the fact is that MPW will get even cheaper if it suddenly turns out that the company’s earnings prospects are actually more at risk than Wall Street currently believes. That’s happened before, if we use Seeking Alpha’s Quant grades as a benchmark:

Seeking Alpha, author’s notes

The positive move in the Revisions you see above doesn’t really look bullish in case you wonder:

Seeking Alpha, author’s compilation

The Verdict

I honestly don’t understand how one can buy shares in a company whose management raises so many doubts in the market. MPW looks like a completely uninvestable stock that needs to go through a turnaround cycle to get back to growing like it used to. But as is so often the case, a typical turnaround doesn’t bear fruit immediately, and even when this business reversal cycle does develop favorably, the share price usually remains flat or stagnant.

As in previous times, I recommend not catching falling knives in MPW stock, as I expect new lows in the long term. In the short term, of course, we can expect sharp swings today due to the technical characteristics of the stock. But most likely, these possible “rips” will likely be used by institutional investors to exit.

So overall, I’m neutral on MPW, having a gloomy outlook for it. Tell me what you think about it in the comment section below!

Thanks for reading!

Read the full article here