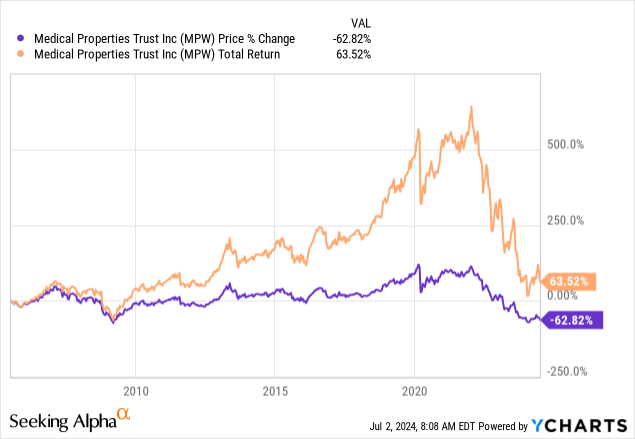

Today’s article turns to Medical Properties Trust, Inc. (NYSE:MPW), a medical real estate investment trust (REIT) that owns properties in the U.S., UK, and Europe. Although having produced solid historical results, MPW REIT has failed to replicate its past success in recent times, leading to a nearly 60% year-over-year drop in market value. Much of Medical Properties Trust’s concerns stemmed from concentration risk, systematic risk, and constituent woes. However, time has passed. As such, I think an updated analysis of the REIT is in order.

Herewith are my latest findings on MPW REIT.

Portfolio

Overview

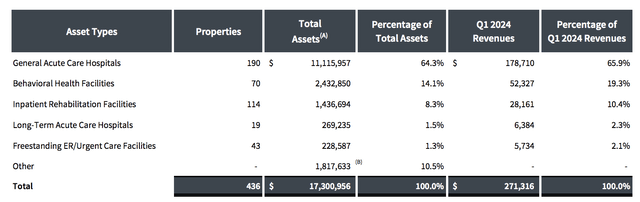

For those unaware, Medical Properties Trust is a medical REIT that primarily invests in acute care hospitals, behavioral health facilities, rehabilitation facilities, and urgent care facilities. Approximately 60% of its asset base is located in the U.S., 24% in the United Kingdom, and the rest in other areas of Europe.

Portfolio Exposure (Medical Properties Trust)

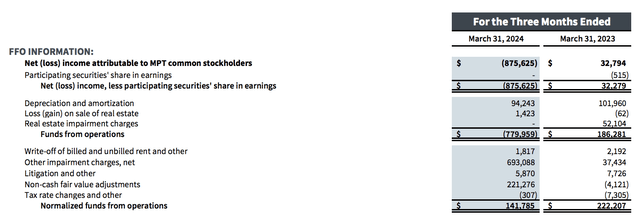

MPW REIT has had a rough year or two. The REIT posted a net loss in Q1, largely due to asset impairments (discussed later). Moreover, it has experienced slower rental demand, diminishing its accounting income. Nevertheless, the REIT’s Funds from Operations (FFO) line item shows that its economic value hasn’t suffered as much as its accounting value.

Income & FFO (Medical Properties Trust)

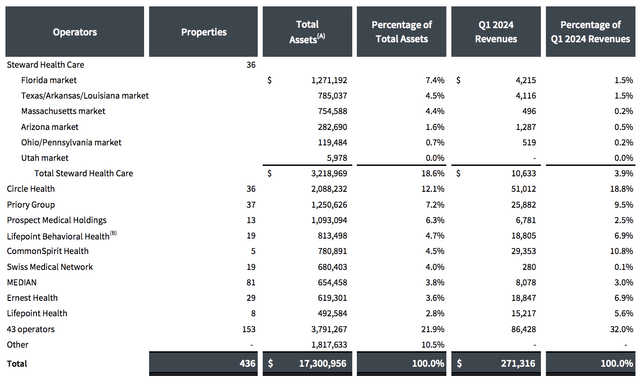

A look at Medical Properties Trust’s portfolio shows that approximately 18.6% of its total equity assets contained Steward Health Care’s properties. However, only 1.8% of its portfolio’s rent is derived from Steward. This is because Steward filed for bankruptcy during the quarter, leading to a loss of rent and an impairment of MPW REIT’s asset base, leading the REIT into a loss. Moreover, MPW REIT wrote a loan to Steward (on which it defaulted), which added to Q1 impairments.

Tenant Concentration (Medical Properties Trust)

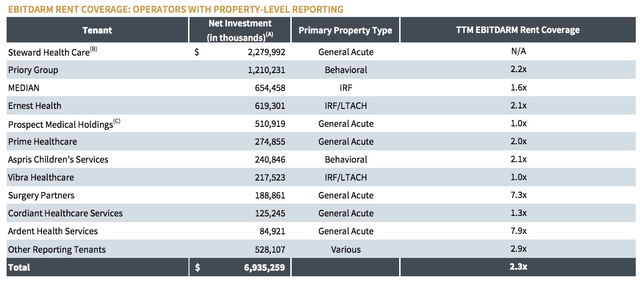

Despite suffering setbacks from Steward, MPW REIT’s other constituents have positive rent coverage ratios. Additionally, MPW REIT has a fund-level interest coverage ratio of 2.5x, suggesting its broader portfolio has coped. Although reports suggest that Prospect Medical Holdings is overdue on rent and faces liquidity issues, the data shows that MPW REIT’s ex-Steward portfolio has positive metrics.

Rent Coverage Ratios (Medical Properties Trust)

My Take

Steward

It goes without saying that Steward is the main talking point, so I want to emphasize Steward’s issues. However, readers are likely unaware of adjacent concerns, which I’ll discuss in this section.

First, Steward secured a $225 million loan after entering a Chapter 11 bankruptcy. I like the fact that third parties like Sound Point Capital, Brigade Agency Services, and Chamberlain Commercial Funding facilitated the loan instead of MPW REIT. Medical Properties had previously granted its tenant a loan and aimed to do so once more before Steward secured third-party financing. I believe this reduced MPW REIT’s concentration risk (versus what could’ve been).

I expect Steward to sell properties to repay the loan, which might be problematic given the elevated interest rate environment and the execution risk embedded in large asset sales like hospitals. This execution risk was proved when UnitedHealth’s (UNH) Optum backed out of a deal to buy Steward’s physician group. In other words, we could see a series of deal breakdowns in the coming quarters due to numerous asset and liability-level concerns.

Regardless of whether Steward’s assets will be sold and whether they will be sold promptly and equitably, I think MPW REIT has retained its credit risk overhang, especially as it still holds an equity position in Steward. Don’t be surprised if additional impairments occur in the next few quarters.

Additional Factors

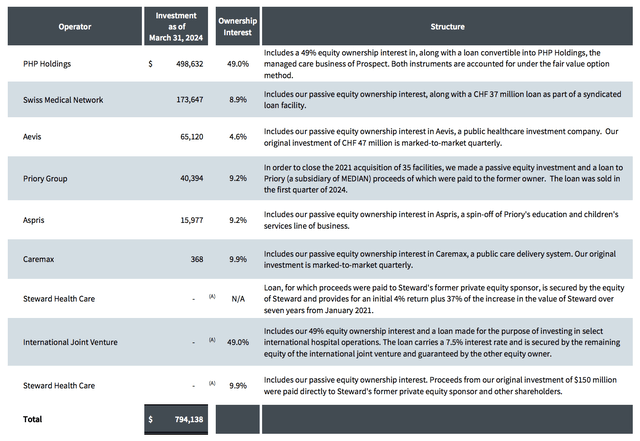

To my knowledge, unlike many REITs, Medical Properties Trust has equity ownership in some of its tenants, allowing it to partake in operational income and execute loan underwriting. I don’t like this aspect as I believe it can 1) confuse the REIT’s financial statements and 2) enhance concentration risk.

Ownership Interest (Medical Properties Trust)

Lastly, on a positive note, I think MPW’s broad-based metrics, which I mentioned earlier, are good. I won’t be surprised if the REIT’s asset value increases once interest rates drop. Moreover, I believe easing U.S. inflation might reduce household expenditures and provide additional scope for hospital earnings via co-payments and other healthcare insurance methods.

Global Inflation Forecast (Statista)

Liability-Level

Overview & My Take

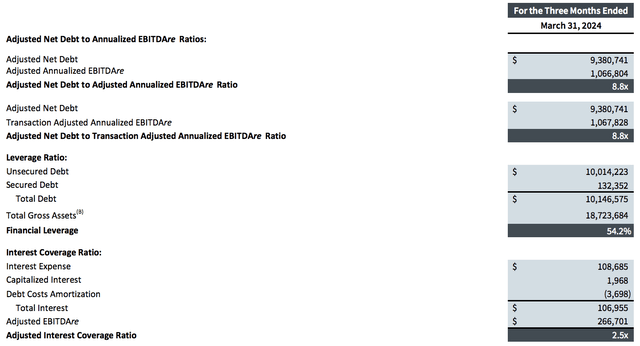

Medical Properties Trust’s key debt metrics show that its interest is covered by a multiple of 2.5x and that it has a net debt-to-adjusted EBITDA ratio of 8.8x. I think the REIT’s debt-to-EBITDA ratio is slightly high, given that a theoretically good ratio is around 3x. However, I reiterated that I believe its IC ratios illustrate sound coverage of debt obligations.

Debt Metrics (Medical Properties Trust)

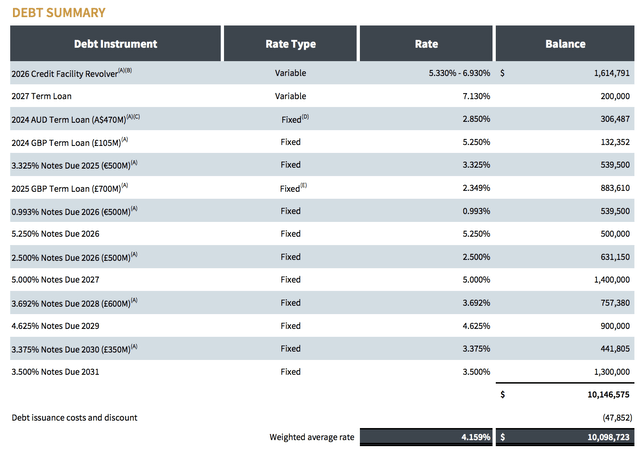

Furthermore, Medical Properties Trust has a leverage ratio of 54.2% at a weighted cost of debt of 4.159%. Additionally, about 89% of the REIT’s debt expires beyond 2033, meaning its obligations are long-term.

I like the REIT’s debt structure due to the tenure of its obligations. Additionally, I think the REIT has modest gearing, which allows it to leverage up when interest rates drop.

Debt Schedule (Medical Properties Trust)

Valuation & Dividends

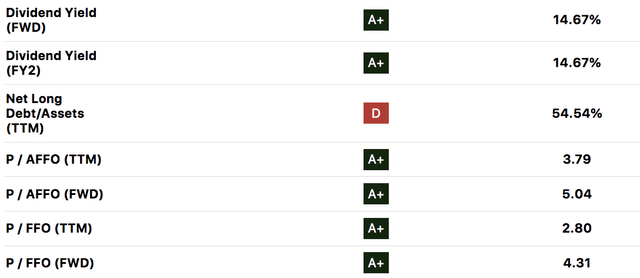

MPW REIT’s price-to-funds from operations of 2.8x stands out as it is at a sector median discount of approximately 77.95%. Moreover, MPW REIT’s price-to-adjusted funds from operations ratio of 3.79x is at a discount of approximately 71.8%, conveying a similar picture.

Aside: P-FFO is a more conventionally used metric, while the P-AFFO is preferred by those seeking a more economic-value outlook.

Despite being statistically undervalued, I’d like to highlight the risk that we might be looking at a value trap here, as I believe MPW REIT’s fundamentals aren’t all copacetic. Nonetheless, I think it’s worth having a nudge as a slight improvement in the REIT’s salient features might spark a deep value/turnaround opportunity.

Seeking Alpha

Lastly, MPW REIT has a forward dividend yield of 14.67%, which I deem solid, especially given the REIT’s interest coverage and debt capital structure. Moreover, some analysts believe the REIT’s recent accounting losses justify a series of dividend cuts. Although I think Steward’s overhang could result in dividend payout risk, I believe the REIT’s economic value shows it might sustain a respectable dividend.

Final Word

Medical Properties Trust’s recent drawdown likely presents a buying opportunity. Although the REIT possesses fundamental doubts, I believe its dividends are well-aligned. Moreover, a rebound after its latest drop is possible, especially after Steward Health Care’s refinancing package.

Factors such as the REIT’s concentration risk and vested interest in struggling entities are of concern. Nevertheless, I think most factors suggest MPW REIT is a promising recovery play.

Consensus: Bullish

Read the full article here