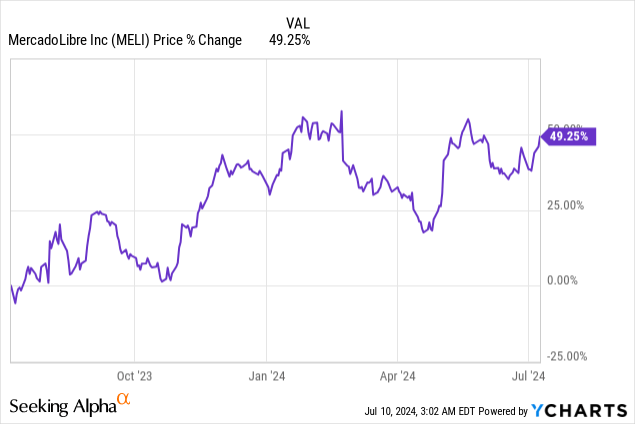

MercadoLibre (NASDAQ:MELI) is a fast-growing e-Commerce platform focused on Latin America that is seeing double-digit gross merchandise volume and revenue growth. Shares of the company have soared almost 50% in the last year as it benefits from strong e-Commerce growth, especially in countries like in Brazil and Mexico, and MercadoLibre is benefiting from a healthy profitability profile. The company is also seeing strong momentum in items sold on its e-Commerce platforms and while shares are not cheap, the MercadoLibre has revaluation potential, in my opinion!

MercadoLibre’s e-Commerce momentum is driven by Brazil and Mexico

MercadoLibre is a Latin America-focused e-Commerce and financial services company with more than 100M customers that is operating in 18 countries, but chiefly in Argentina, Brazil, and Mexico. MercadoLibre is seeing strong gross merchandise volume momentum in its e-Commerce core business, which in turn is driving revenue growth and product turnover on its platform. The market opportunity in Latin America includes a combined population of more than 500M, which makes the geography attractive from an e-Commerce penetration point of view.

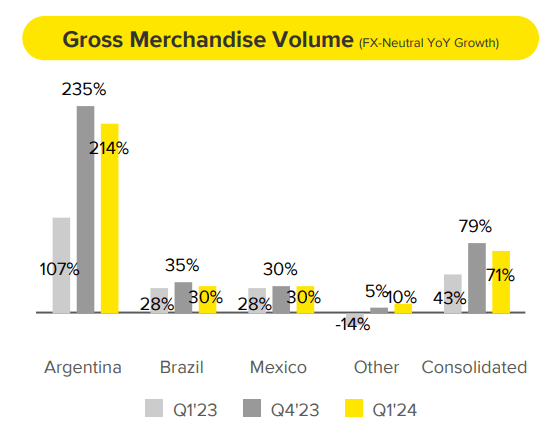

Gross merchandise volume is a key performance metric for e-Commerce companies, and it quantifies the amount of merchandise that is being sold on an e-commerce platform in a specified period. MercadoLibre’s gross merchandise volume in both Brazil and Mexico grew 30% year over year in the first quarter due to strong economic growth, a larger number of items sold on the e-Commerce platform as well as growth in customer accounts. Total consolidated gross merchandise volume in Q1’24 was $11.4B, showing 71% Y/Y growth.

Argentina’s gross merchandise volume soared 214% year over year in Q1’24, mainly because of out-of-control prices increases, which actually led to a drop in items sold on the Argentinian marketplace. Inflation in Argentina hit 276% in May, which, according to Reuters, was the highest in the world.

MercadoLibre

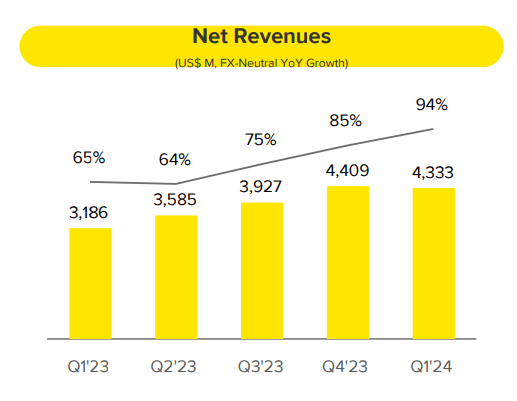

Growth in gross merchandise volume and items sold has led to sustained tailwinds for MercadoLibre’s top line: the e-Commerce company generated $4.3B in net revenues in the first fiscal quarter, showing 36% year over growth. The net revenue trajectory is upward trending as the e-Commerce company is focused mainly on fast-growing developing countries like Brazil in Latin America. In the first-quarter, 385M items were sold on the MercadoLibre e-Commerce platform, showing 25% growth on a consolidated basis. In Brazil, the largest market for MercadoLibre, the number of items sold increased 32% year over year.

MercadoLibre

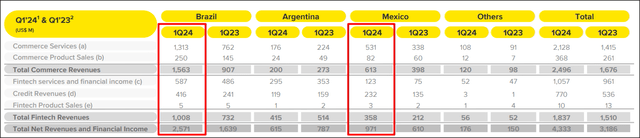

As far as MercadoLibre’s net revenues go, they split into two segments: 1) E-Commerce and 2) Fintech. In the first category, e-Commerce, MercadoLibre generated $2.5B in net revenues in Q1’24, showing a year-over-year increase of 49% while the second category, Fintech, generated $1.8B of net revenues (+22% Y/Y). MercadoLibre therefore sees its strongest growth in the e-Commerce segment, while Fintech is growing slower, at less than half the rate as e-Commerce.

The company is chiefly growing through better penetration (a higher number of items sold) in its key markets. The biggest market by far is Brazil, which generated $2.6B of revenues (both e-Commerce and Fintech) and therefore represented 59% of MercadoLibre’s consolidated net revenues. Brazil is followed by Mexico, with net revenues of $971M and a revenue share of 22%.

MercadoLibre

Highly profitable e-Commerce business

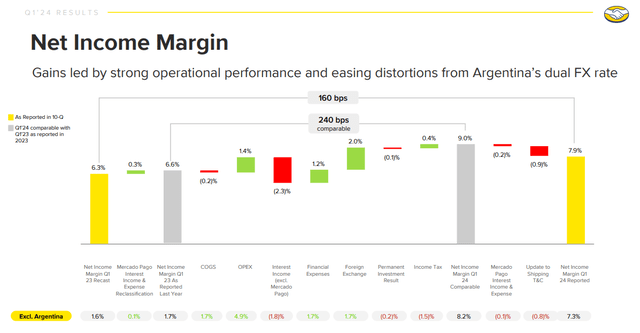

MercadoLibre is not only seeing double-digit growth in its core markets and its consolidated top line, but the e-Commerce platform is also widely profitable on a net income basis. In the first-quarter, MercadoLibre generated a net profit of $344M, showing year-over-year growth of 71%. The e-Commerce platform’s net income margin also improved to 7.9% (+1.6 PP Y/Y) due to strong execution in Brazil and Mexico and lower currency headwinds related to the company’s business in Argentina.

MercadoLibre

MercadoLibre’s valuation

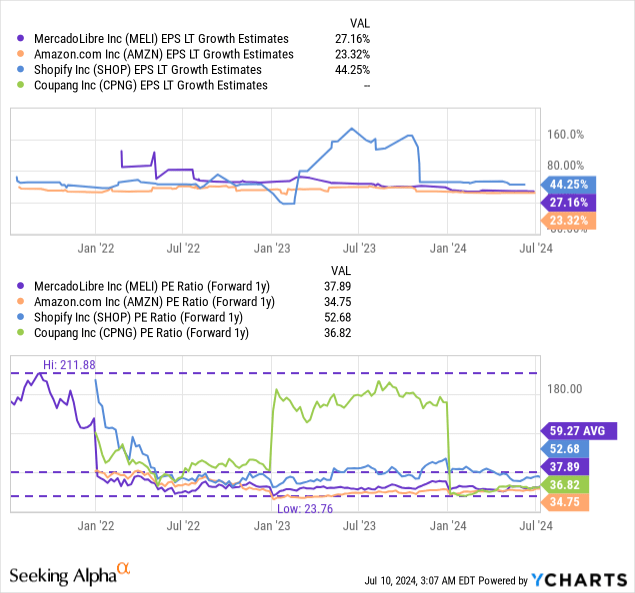

MercadoLibre is a fast-growing e-Commerce platform with an attached Fintech business, and the enterprise has revaluation potential, especially in the context of its enormous top line and gross merchandise volume growth. MercadoLibre is currently valued at a price-to-earnings ratio of 37.8X — based off of FY 2025 earnings — but the e-Commerce company is also growing more quickly than Amazon (AMZN), the world’s largest e-Commerce platform.

Amazon is trading at a P/E ratio of 34.8X, but Amazon’s business includes a large Cloud business, Amazon Web Services, which is a driver of the company’s topline growth. From an earnings growth point of view, MercadoLibre is growing faster than Amazon (even without a Cloud business) which works in favor of the Latin American company: MercadoLibre’s long term EPS estimates call for 27% annual growth compared to 23% for Amazon and 44% for Shopify (SHOP).

Shopify, another retail-focused e-Commerce platform, that is growing its top line around 20% annually, is trading at a P/E ratio of 52.7X, but Shopify only recently achieved GAAP profitability, so this high price-to-earnings ratio is set to drop going forward.

I believe MercadoLibre’s strong GMV and revenue momentum, which is achieved mainly from Brazil and Mexico, justifies a much higher valuation factor for the e-Commerce company. In my opinion, MercadoLibre’s could trade at a 45.0X P/E ratio, given its high double-digit growth rates in gross merchandise value and its impressive outlook for EPS growth. At a 45.0X P/E ratio, MercadoLibre would still be much lower valued than Shopify — which I consider to represent enormous growth value for investors — and have a fair value in the region of $2,045. This is a dynamic number, and it could rise or fall in-line with the company’s GMV and topline growth.

Risks with MercadoLibre

The biggest risk with MercadoLibre is the potential devaluation of currencies, in Latin America in general, but in Argentina especially. Argentina is seeing soaring price inflation, which can skew MercadoLibre’s financial results and make profits achieved in this country much less valuable for investors outside of Argentina. What would change my mind about MercadoLibre is if the company were to see slowing gross merchandise volume growth in Brazil and Mexico.

Final thoughts

MercadoLibre is a highly-promising, fast-growing e-Commerce and financial services platform with significant gross merchandise volume and revenue momentum in Latin America and especially in its two core markets, Brazil and Mexico. MercadoLibre is also widely profitable on a net income basis, although I do see continual revenue and earnings risks in Argentina given its run-away pace of inflation. Shares of MercadoLibre have upside revaluation potential given its strong business momentum in its key markets and with the company’s earnings expected to continue to grow in the double-digits in the years ahead, I believe shares are set for new highs in the near term!

Read the full article here