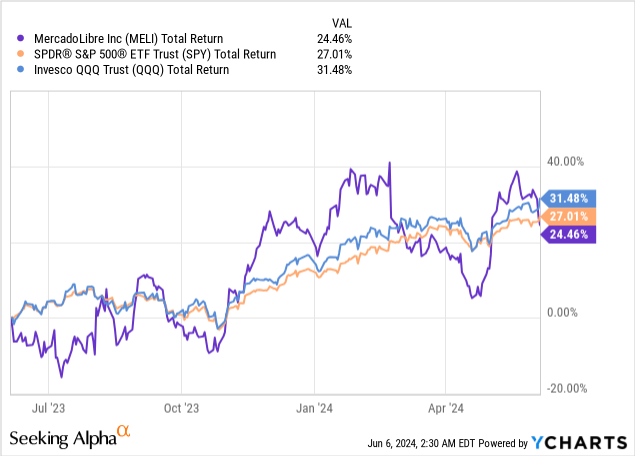

MercadoLibre’s (NASDAQ:MELI) shares have been trailing the market over the past year, despite consistently executing on its hyper-growth trajectory.

With revenues growing by approximately 40% during the period, and profit more than doubling, the valuation problem is becoming increasingly clear.

Let’s dive in.

MercadoLibre’s Underperformance

I initiated coverage on MELI stock with a Buy rating back in February, as I estimated the company will more than quadruple its EPS by 2028. In the article, I went through the company’s diversified business segments, its long-term prospects, and the significant tailwinds it enjoys as a digital leader in quickly developing geographies.

Over the past year, MELI has been underperforming the market, despite growing revenues by more than 40%, and nearly doubling its EPS. The reason is simple, the market expected these results.

This is a testament to the company’s amazing execution but also reflects a big problem that MELI does not control, and that is valuation.

Let’s start with what MELI does control.

Growth Accelerating, Margins Expanding

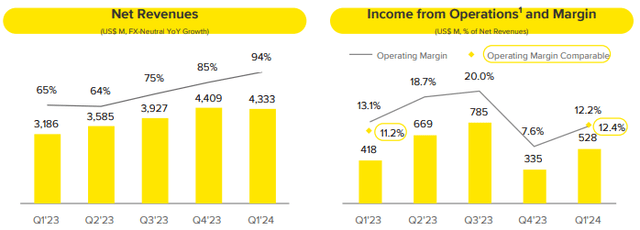

Following a disappointing report in Q4’23, with lower-than-expected margins, primarily due to one-offs, MELI came out strong in the first quarter of 2024, seeing revenue growth of 36%, and operating margins reaching a Q1 record of 12.2%.

Revenues of $4.3 billion and EPS of $6.78 both handily beat estimates. Geographically, growth was led by Brazil and Mexico, which are also the company’s largest, with revenue growth of 57%, and 59%, respectively.

Mercado Libre Q1’24 Presentation

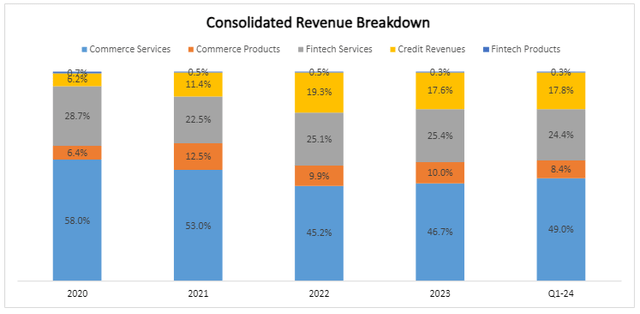

While MercadoLibre is constantly being referred to as the Amazon (AMZN) of Latin America due to its online marketplace, MercadoLibre has a huge financial services business, a space Amazon doesn’t really participate in. Other than that, there are plenty of similarities, as MELI is building its own Prime with MELI Mas, and is currently developing its advertising business.

In Q1’24, fintech and credit revenues were 43% of revenues, compared to 47% in Q1’23, as commerce services outgrew all other lines of business.

Created and calculated by the author using data from Mercado Libre financial reports.

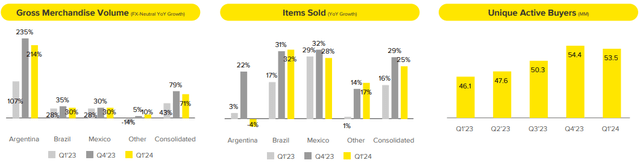

Diving deeper into the marketplace business, all operational metrics point to continued hyper-growth. GMV grew 71% on a constant currency basis, items sold increased 25%, and unique buyers reached 53.5 million.

Mercado Libre Q1’24 Presentation

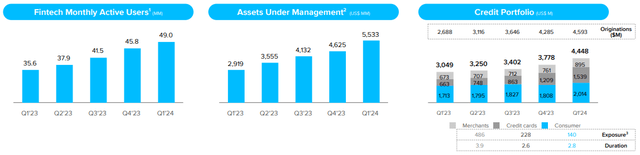

On the financial services front, monthly active users reached 49.0 million, and the credit portfolio increased to $4.5 billion, with a record quarter of originations. Despite the fast growth of the credit portfolio, MELI is maintaining healthy NIMAL margins at 31.5%, while 90-day NPLs declined and provision coverage increased.

Mercado Libre Q1’24 Presentation

Overall, this was an extraordinary quarter for MercadoLibre. The company delivered on its promise to recover margins quickly, and it continues to be the number one marketplace in Latin America, by a wide margin.

Growth Opportunities & Competition

MercadoLibre operates in the fast-growing LATAM market, primarily in Brazil and Mexico. These are two geographies primed for disruption, with growing populations, improving economies, supportive regulators, an ambitious working class, and a strong digitalization trend.

The company’s offerings are virtually tailor-made for this backdrop, as it offers essential products and services at a quality the LATAM population has never experienced.

MercadoLibre is not the only company trying to capitalize on this huge opportunity, with prominent competitors in both the e-commerce and fintech fronts.

In e-commerce, companies like Amazon and PDD’s Temu (PDD) are also in the field. In fintech, there’s another company I cover, Nu Holdings (NU), along with many others.

Despite intense competition, the opportunity in Latin America is huge, and it’s clear MercadoLibre is going to be the number one or number two player in most verticals it’ll enter.

So, we have a very large opportunity, combined with exceptional execution.

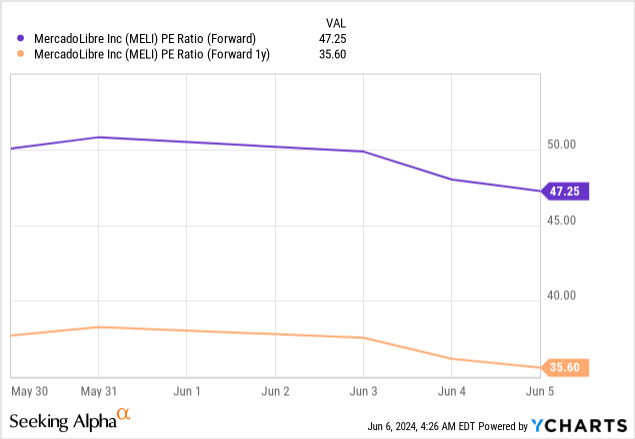

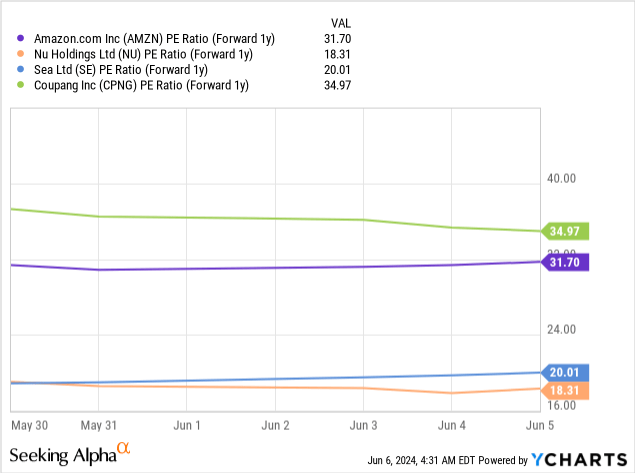

The Problem Is, Of Course, Valuation

MercadoLibre is trading at 47 times 2024 earnings, based on current consensus estimates, and 36 times 2025 estimates.

That is higher than Amazon, and much higher than Nu, another LATAM disruptor. While Amazon is expected to grow much slower than MELI, its risk set is much lower. When it comes to Nu, it is a capital-light business (unlike MELI), and it’s expected to grow faster as well.

It’s also higher than Sea Limited (SE), which has a similar business more focused on Southeast Asia, and Coupang (CPNG), which is a South Korean comparable.

There are puts and takes on why MercadoLibre is better executing, faster growing, less risky, or has more opportunities, but the bottom line is that buying MercadoLibre at these levels is buying high.

That’s the main reason why the stock has been essentially flat since my previous article, and why it’s been trailing the market despite its extraordinary results.

Long-Term View On Valuation

In the near term, valuation is quite significant. It’s undeniable that MercadoLibre’s numbers were exceptional, and yet the stock didn’t budge. Continuing on that line of thought, it’s hard to imagine what MELI could bring in the upcoming quarters that will make the stock respond with a sharp increase, considering the very high expectations we already discussed.

With all that said, in the long term, the company’s growth prospects, and its proven ability to execute on them, are a clear path to market-beating performance of the stock as well.

These are current consensus estimates for MELI’s EPS growth until 2028, which I compiled from several service providers:

Created by the author based on compiled consensus estimates.

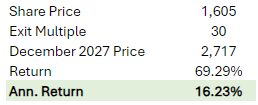

I think there’s a much higher probability that MELI surpasses these expectations rather than misses them, but let’s stick to them. Let’s also take an exit multiple of 30x, which seems reasonable to me, considering the company will have a significant growth runway ahead of it.

Created and calculated by the author.

That will get us an annual return above 16% based on today’s share price, with a price target of $2,717 by December 2027. While that is attractive, I believe there are many opportunities that have a higher upside in the near term.

I believe MercadoLibre will outperform the market in the long term, but I wouldn’t rush into buying it at current levels as well. Therefore, I’m downgrading the stock to a Hold.

I expect the stock to end the year at around 38x times 2025 EPS, equaling a price target of $1,715 a share.

In my previous article, I overlooked the valuation hurdle, and I also expected faster margin expansion. As the company rightfully continues to invest in its future, the margin expansion pace will be slower, but it means less upside in the near term as well.

Conclusion

MercadoLibre is an extraordinary business, with a top-quality management team that is undeniably executing on the company’s huge growth opportunity.

Despite the exceptional results, the stock has been underperforming, due to the company’s over-demanding valuation.

I believe that for MercadoLibre to outperform in the near term, it’ll have to handily beat the very high expectations the market has set for it. While I do expect consistent beats, I don’t expect them to be significant enough to drive further valuation expansion, as MELI already enjoys a significant premium over lower-quality yet very strong peers.

Therefore, I rate MELI a Hold.

Read the full article here