Editor’s note: Seeking Alpha is proud to welcome Marquell Moore as a new contributing analyst. You can become one too! Share your best investment idea by submitting your article for review to our editors. Get published, earn money, and unlock exclusive SA Premium access. Click here to find out more »

Investment Thesis

Methode Electronics (NYSE:MEI) is a company that I like to say makes the world light up. They’re responsible for providing UI and LED systems, power distribution/sensor applications, and data processors/transceivers for automotive, industrial, consumer appliance, and tech customers. You might think that with such a large and diversified customer base, Methode Electronics would be protected from volatility in any single industry it serves. However, a closer look shows that this is simply not the case. Concentration in any single industry can be a blessing or a curse, entirely determined by that industry’s current and long-term prospects. It’s precisely because of this relationship and its heavy reliance on the automotive industry that I feel Methode Electronics is undervalued and rate it as a buy. I believe that it is this level of exposure to the automotive industry and weakness in manufacturing overall, that primarily contributed to the company’s 70% stock price decline over the past year. However, Methode has benefited and looks to continue benefiting from the EV transition in that same industry, setting the company up for long-term success.

Methode Electronics

Company Overview

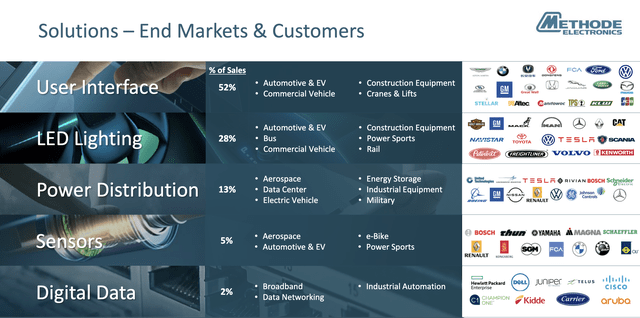

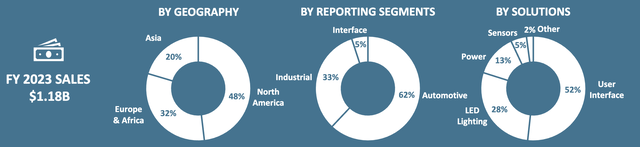

Methode Electronics engineers mechatronic solutions for OEMs across a broad range of applications detailed in the graphic above. It achieves this either by designing the technology itself or acquiring companies that complement its existing portfolio. Methode’s technology solutions serve three main segments: Interface, Industrial, and Automotive. The company recently discontinued its Medical segment operations after continued losses, but historically this only represented about 0.4% of net sales. The Interface segment, which makes up 5% of sales, offers copper transceivers for cloud computing and telecommunication equipment. Further applications include user interface solutions for appliances, POS systems, and sensors for RVs and boats. The Industrial segment, accounting for 33% of net sales, provides external lighting solutions and cabling systems with applications in aerospace, commercial vehicles, and construction equipment. The Automotive segment, Methode’s largest, accounts for 62% of revenue. This segment provides electronic and electro-mechanical solutions to automobile OEMs.

Methode Electronics

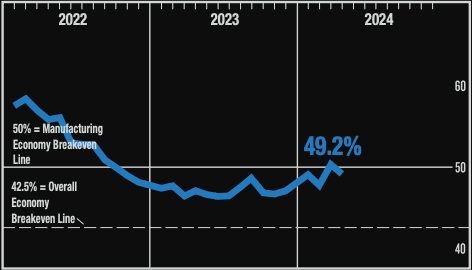

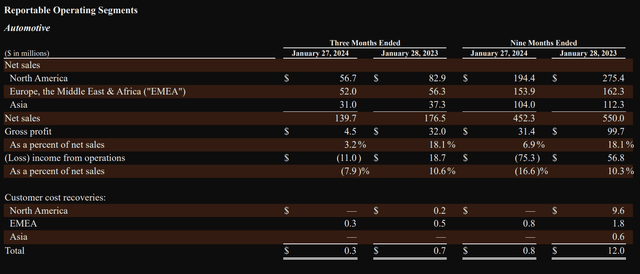

A slowdown in broader manufacturing activity coupled with price inflation due to global supply shocks, such as the recent chip shortage, is partly to blame. In April, the Manufacturing PMI was at 49.2%, following March’s 50.3%, moving back into contraction territory. This was after a 16-month streak of contraction, indicating that Methode’s customer base was less active during that time. Since Methode’s fiscal year ends in July, that slowdown will show up in this year’s annual report. For the nine months ended January 27, 2024, net sales were down 4.7% overall, and 7.4% for the third quarter. However, those figures include the added revenue from the Nordic Lights acquisition. Management explained that, when excluding the acquisition and other favorable currency translations, sales were down 15.5% for the quarter, a much more material decline when comparing on a constant basis.

ISM World

Now, moving on to the expenses, as I said earlier, 52% of Methode’s business is conducted outside of North America, representing an inherent supply chain risk. Shocks like the Red Sea and Suez Canal crisis and the Russian-Ukraine war, as they did for many other companies, choked the supply chain and raised the costs of getting products to market, mainly through increased transportation expenses. Now, when a business has tremendous pricing power, this is less of an issue because it can simply raise the price of its products. But for a business like Methode, where competition is based on contract bids, price hikes aren’t really an option. The best alternative is to negotiate with customers for cost recoupment, but when customers are experiencing 16 months of contraction in business, this is a difficult task. Management doesn’t detail a recoupment target, but it has referenced some difficulty in cost recovery in the past. The cost inflation eats away at margins, and any difficulty recovering those costs puts margin recovery under threat.

While we have experienced some success in recouping cost recoveries, we expect these headwinds will be with us, at least through the remainder of fiscal year ‘23. (Q1 2023 Earnings Transcript)

The company is currently reorganizing its management, after Donald Duda, who led Methode since 2000, retired. Avi Avula stepped in as interim CEO last December while announcing his chief priority in reviewing expenses to restore profitability. However, in May, he was replaced as interim CEO by Kevin Nystrom. Mr. Nystrom and previously appointed interim CFO David Rawden are both managers at the consulting firm AlixPartners, and it is because of this shared background that I feel now Methode has a unified vision for becoming profitable again. The potential short-term success that these two managers generate could act as the foundation for their permanent successors.

The biggest reason for the poor performance this past year is Methode’s ties to the automotive industry. Sixty-two percent of Methode’s business has been negatively affected by a slowdown in the automotive industry caused by labor strikes, supply shocks, and a general wind-down in new programs as a result of a weak economy. The result is that automotive manufacturers launch fewer new programs, which reduces the number of revenue opportunities that Methode can bid on. Aside from traditional automotive program roll-offs, in the third quarter, management also noted weakness in EV demand. Electric vehicles are a growing market for the company compared to traditional ICE vehicles because of the added power distribution business opportunities specific to EVs.

Methode Electronics

For the nine months ended January 27, 2024, net sales in the automotive segment were down 17.76%. Then, taking into account the cost inflation and operational inefficiencies, management noted that operating income decreased to a loss of $75.3 million.

Methode Electronics Financial Statements

Bright Prospects for Recovery

Methode’s recovery strategy can be divided into two types of growth: organic and inorganic. First, on organic growth, the company has broad opportunities in data centers as the world looks to invest in AI and cloud computing. Methode provides electrical components for these data centers. Management did, however, note some inventory overhang in FY 2023, but as of the third quarter for this fiscal year, that seems to be improving. Finally, broader applications like commercial vehicles and construction equipment tend to move in line with the economy.

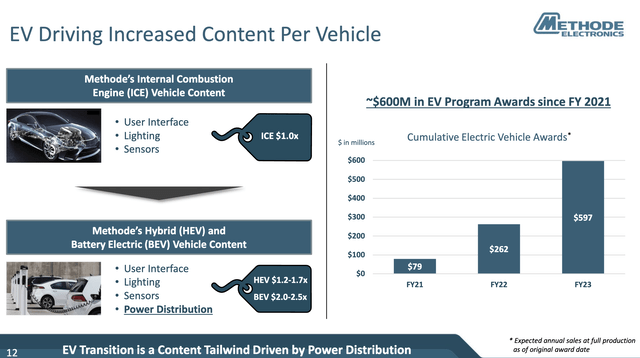

The automotive segment will also improve as the economy (especially North America) improves. Union contracts have already been negotiated, and supply chain shocks have eased over the past year. The segment is becoming increasingly attractive for Methode due to a growing emphasis on sustainability that directly correlates with a rise in EV demand. As seen in the EV Content Penetration graphic, the more advanced technology of EVs prompts OEMs to launch new programs aimed at integrating that technology and complying with more sustainable environmental regulations.

For Methode, the transition creates opportunities to expand its market presence by supplying the solutions to meet these demands. The long-term transition to EVs will continue to gain strength, and EV programs already represent about 20% of net sales. Their share of sales will continue to grow as the company pursues higher content penetration. Management has made it clear that the recent performance slump is attributed to a weak automotive industry. However, I believe that Methode’s exposure to this sector is what makes long-term success possible, as the company continues to capitalize on the EV transition.

The technological applications it provides compete with other global providers, looking to offer the right mix of affordability and quality to potential customers. Methode can achieve affordability as new management addresses the operational inefficiencies noted throughout the year and progresses on any remaining cost recoveries from easing cost inflation. The quality is achieved through strategic acquisitions that augment its existing portfolio of solutions, like its recent Nordic Lights purchase.

Methode Electronics

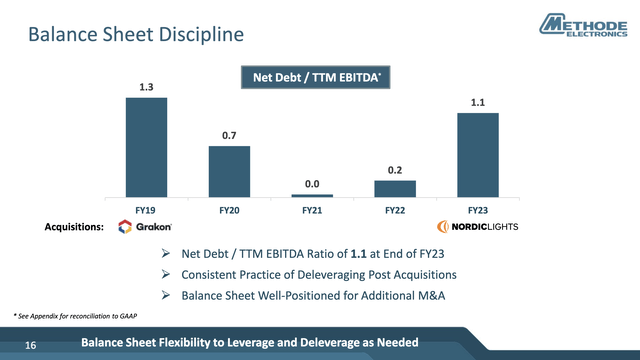

Acquisitions that leverage existing manufacturing and operational capabilities provide deeper content penetration per customer. Nordic Lights complements Methode’s own LED lighting solutions and others that have applications in EVs and commercial vehicles/equipment. For the nine months reported so far this fiscal year, Nordic Lights has accounted for $63.3 million of Methode’s $837.2 million net sales and offset Methode’s loss of $66.0 million with its $2.8 million in earnings. Acquisitions like this will continue to be possible as long as Methode maintains a strong balance sheet and strategy of only taking on debt when an acquisition opportunity is discovered and using the proceeds to pay down that debt.

Historically, this discipline has performed well as the increased cash flow from the acquisition goes towards reducing debt liability. In FY18, before acquiring Grakon, a company that provides lighting systems across the vehicle market, Methode’s $246.1 million in cash more than covered its $57.8 million of debt while its EBITDA was $146.4 million. From fiscal years 2019 to 2021, EBITDA totaled $524.9 million while net debt fell from $209.4 million in 2019 to $134.8 in 2020 ($100 million of which was precautionary liquidity in response to Covid-19) and to $6.9 million in 2021. This balance sheet discipline is a testament to what Methode can do in a healthy market.

A similar situation is unfolding with the more recent Nordic acquisition, but in a weaker market. Before the acquisition, in FY22, Methode’s net debt stood at $38.5 million while it recorded EBITDA of $164.3 million. The year of the acquisition, FY23, net debt rose to $146.6 million and EBITDA fell to $139.9 million. For the nine months reported this fiscal year, net debt was $208.4 million and EBITDA so far is $(7.2) million. The declining EBITDA as a result of the factors described above limits Methode’s ability to repay its debt. If that were to continue, the company would have to forgo certain acquisitions, which hurt its long-term prospects.

Methode Electronics

Performance Relative To Peers

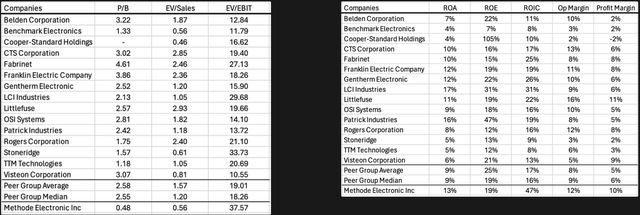

Now looking at the peer group for Methode, we can see that it’s trading below the median P/B and EV/Sales for its peers, at 0.48x and 0.56x respectively. But that’s not as important without knowing how the company performs relative to its peer group. Looking at that, we can see that it either matches or surpasses its peers across all operating performance metrics based on ten-year averages. Essentially, an above-average asset is selling for a below-average price.

This peer group has varying levels of exposure to the automotive sector, affecting their respective stock prices differently depending on that exposure. While Methode is heavily weighted towards the automotive sector, its acquisitions address these risks by offering technological solutions that diversify its portfolio of applications. Returning to Nordic Lights, for example, the purchase not only strengthened its automotive business, but also offers lighting systems for heavy machinery and infrastructure applications. Additionally, as inventory overhang for electrical components in data centers eases and construction continues, this growth opportunity will persist as it did in the past.

These efforts to diversify, coupled with its superior operating performance, make Methode a compelling choice for investors. Unlike some peers, which may be less diversified or have less efficient operations, Methode is positioned to capitalize on growth opportunities in multiple industries, thereby reducing the risk of a slowdown related to a single sector.

Company Financial Statements

But multiples only tell how valuable an asset is relative to others. Since Methode’s operating and net loss is at $50.5 million and $66 million respectively, it’s better to capture that info within a valuation.

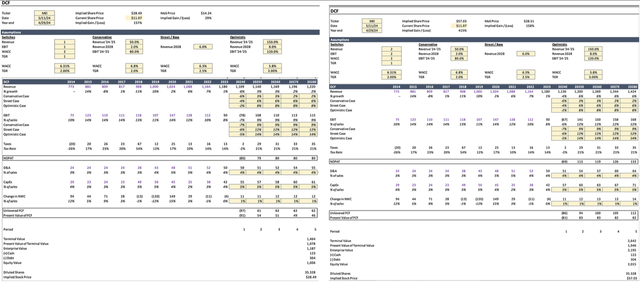

Taking a close look, a DCF analysis for both conservative and base scenarios prices the company between a range of $28.49 and $57.03 per share or an enterprise value range of $1,187 million and $2,195 million. Compared to a current enterprise value of $668.84 million, and the numbers suggest an undervalued asset even when accounting for losses in the current fiscal year.

Valuation: Scenario Analysis

Starting with the base scenario, sales of $1,136 million are general consensus among analysts given the performance for the nine months that ended January 27, 2024. This number captures the slowdown in revenue Methode is currently experiencing. Management has stated that it targets a 6% CAGR of sales over any three-year period. However, I believe for the three-year period ending in 2025, the company will miss its 6% CAGR target but will get back on target by 2028. Considering the 1% growth in revenue last year, the forecasted decline for this year, and the suspension of forward guidance by management, I believed using 6% as a sales growth number until 2028 was appropriate to avoid overestimating growth for the 2025 fiscal year. Based on historical performance and as the broader manufacturing (especially automotive) sector turns back in its favor, I feel that this level of sustained growth is achievable for a base case.

To arrive at EBIT, for the 2024 forecast, I based it on the performance so far this year. I used the average EBIT of the past three quarters as an estimate for the Q4 figure to arrive at a full-year estimate. For the following years’ forecast, I applied the historical EBIT margin of 12% to arrive at those estimates. This implies the belief that cost inflation will subside as the company addresses the operational inefficiencies of the current year. The conservative forecast implies that revenue growth is 50% worse than the base case for the years 2024 to 2026, then slows to about 2% until 2028. This suggests a continued slowdown in manufacturing and the automotive industry. For EBIT, the conservative case implies that margins are about 80% of the base case estimates, indicating more long-term cost inflation. The terminal growth rate for each case is 2.5%.

Then, to arrive at free cash flow estimates, I applied the forecasted inputs of capital expenditures, D&A, and changes in net working capital, which are based on an average of their historical share of sales. After the necessary calculations, we have a valuation range between $28.49 and $57.03 per share. This represents a 142% upside for investors from the bear case for Methode’s performance estimate.

Methode Electronics Financial Statements and Author’s Calculations

Assessment of Risks and Conclusion

The company’s continued dependence on the automotive sector remains a significant risk, particularly with the growing share of sales from EV programs. Any future downturn experienced by automotive OEMs could materially affect the company’s operations. Speaking of operational performance, any breach or risk of breach of debt covenants or deterioration of creditworthiness could hinder any potential acquisitions. So far this year, the company has experienced operational inefficiencies at its plants, contributing to its poor performance. This increases the risk of breaching debt covenants and complicates acquisition strategies.

During this year’s third quarter, management noted that the company breached its consolidated leverage ratio covenant for its revolving credit facility, forcing management to renegotiate terms and take on higher interest expenses. The weighted-average interest rate on US dollar and euro-denominated borrowing under their credit agreement was 7.2% and 5.6% respectively, as of October 28, 2023. After breaching the covenant, those interest rates rose to 7.4% and 5.9% as of January 27, 2024. This increased interest expense poses another challenge to management’s efforts to return to profitability.

Speaking of management, any future issues in finding a new permanent CEO and CFO complicate any long-term strategy for profitability. Not to mention the $120,000 in weekly consulting fees paid to AlixPartners for the services of Nystrom and Rawden, adds another layer of complication. From the start of last fiscal year to May 1, 2024, Methode has paid $1.4 million in consulting fees to AlixPartners. With these added expenses, dividends to shareholders are under threat. Although Methode has continued to pay its $0.14 per share dividend, this year’s profit losses and increased fixed expenses make their continuance less likely in the short term. However, any suspension has yet to be announced.

Nonetheless, taking into account the company’s growth opportunities and absent a continued downturn in the automotive industry, Methode is positioned to achieve long-term growth and continue returning value to shareholders.

Read the full article here