MicroStrategy Incorporated (NASDAQ:MSTR) has announced a 10-for-1 stock split. Stock splits do not normally affect the value of a business, but in this case we could see some interesting market dynamics play out which make this a potentially very bullish development.

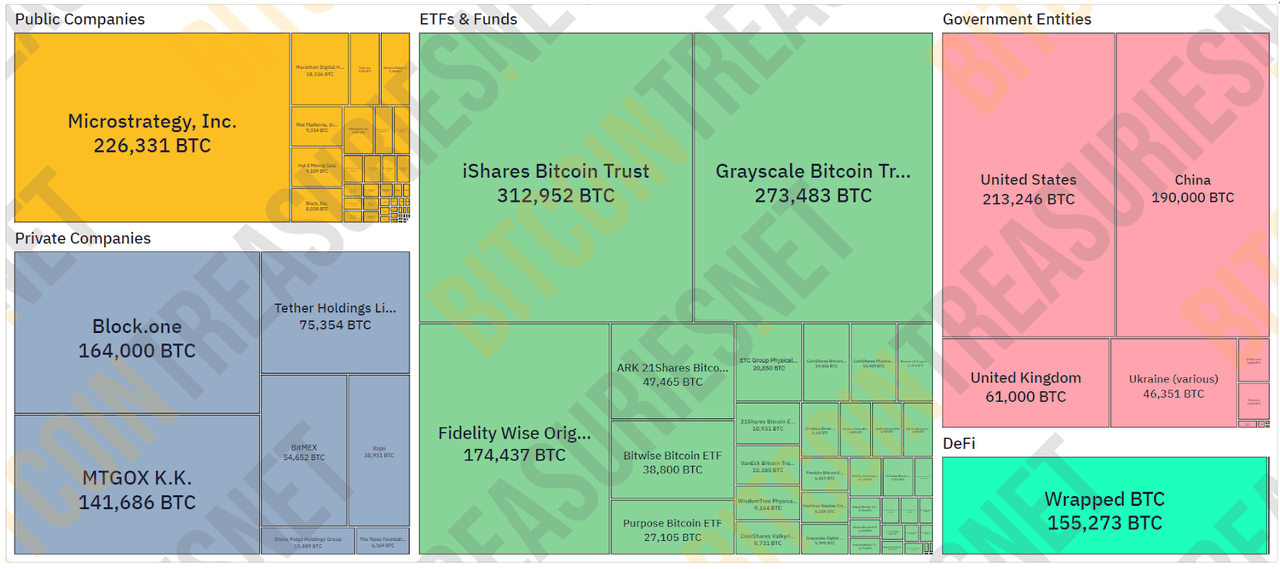

I have covered the possible consequences of MSTR’s inclusion into the S&P 500 Index. MSTR has largely been running a strategy of securing fiat financing from debt and equity markets to continue to acquire Bitcoin (BTC-USD). It is currently one of the largest holders of BTC in the world, holding even more than the United States government.

Bitcoin Treasuries (bitcointreasuries.net)

MSTR’s inclusion into major indices allows it to issue shares with a permanent forced buyer in the form of passive index funds. All the capital can be used to purchase more BTC which drives up the value of BTC and the value of MSTR’s leveraged balance sheet. The real winner here would be BTC, but MSTR’s enormous treasury could eventually evolve into a cash flow engine. The reflexivity of such market dynamics needs to be considered because in BTC you have an asset with complete supply inelasticity with respect to price.

In this article, I’d like to outline another reflexive market dynamic which is now more likely because of the recently announced stock split. Currently, MSTR shares are trading at around $1,400 per share. Post-split (and assuming the same price) they will be trading at $140 per share. The main consequence here is it allows for a more liquid options market which helps increase the share price by raising the number of short put-generated bids and the potential for a gamma squeeze to play out. It also gives investors more ways to hedge and speculate on the stock.

Options on US securities have a 100x multiplier. When the share price is over $1,000, each contract controls over $100,000 of notional value. This prices out a lot of smaller retail traders which together make up a non-trivial bloc of trading volume. The meme stocks of early 2021 are an example of the force that retail traders can exert over markets, within isolated incidents.

MSTR is a stock with a sizable likelihood of experiencing an options-fueled rally thanks to gamma and short squeezes. I had discussed this in my previous article about MSTR, even predicting that in certain cases, the stock could soar past $5,000 per share (which would be $500 per share, split adjusted). To be clear, I believe that in this context, it would look like a characteristic spike and drop from a squeeze, not a sustainable rally which sets a new floor for the price.

The lower share price thanks to the split will allow retail options volume to enhance the liquidity of the overall options market. Imagine people selling cash secured puts on MSTR. This makes sense as a trade because the stock has an enormous implied volatility and the earned premiums could be substantial. Cash secured puts are effectively a bid below the spot price too. People who want to buy in 5% lower might sell puts with strike prices in the 5% lower region, and this establishes a buy pressure at that region. As these bids are stacked up, it sets a natural resistance for the stock price.

The post-split stock price also makes the minimum betting size for call options less expensive. An ATM call option expiring in January 2025 costs $41,000. The cost would only be $4,100 after the split.

Fundamentals-Based Triggers for a Gamma Squeeze

As I stated in my last article:

A lesser known form of reflexive market behavior is called the gamma squeeze. Gamma is the convexity offered by an option contract. It measures how much delta changes with respect to the price of the underlying stock. Gamma squeezes happen when traders buy a lot of call options from market makers. Market makers generally try to maintain a directionally neutral portfolio. If they sell a lot of call options to traders, this means they are inherently short the upside. The instantaneous amount they are short is seen in the total delta of the call options they sold. To get back to directionally neutral, they must buy delta units of the underlying stock.

What’s remarkable is that options deliver a lot of delta for a very low amount of capital. Thus, a relatively small amount of capital can be used to force real market participants (market makers) to buy a huge amount of underlying stock. And it gets even better. As the stock rises, the calls become closer to being in-the-money and this increases the delta of the calls, which increases how much stock the market makers have to buy, which increases the stock price. A reflexive loop is thus created.

And this was where the name “gamma squeeze” comes from. Gamma dictates how much additional shares market makers must buy, since it is the change in delta (ie. how much market makers need to be long to hedge out the option) with respect to the underlying price. More gamma means more shares must be purchased. More calls purchased by traders means more gamma the market maker has to hedge out.

This is what happened to GameStop (GME) back in January 2021. It started as a short squeeze but also turned into a gamma squeeze as retail traders piled into call options. I believe that something very similar can happen to MSTR, once the reflexive dynamics inherent to index inclusion becomes more clear to people.

I think a stock split will only make such an event more likely. The thing is that now it could be triggered from a multitude of different things. You see, MSTR currently has a 15% short interest. Much of the short interest is likely shorts betting that the premium of MSTR shares over its BTC treasury will close over time. This trade would be structured as long BTC (presumably via the ETFs) and short MSTR.

While I’m sympathetic to this view, I think it betrays ignorance of what is really going on. Firstly, MSTR investors are largely interested in the prospect of increasing the BTC per share over time, just as investors in other companies might be interested in a business increasing its book value per share over time. The fact that BTC per share increases over time means that there needs to be a premium to the current amount of BTC per share. Otherwise, you’d be saying that no company should ever trade above book value of equity.

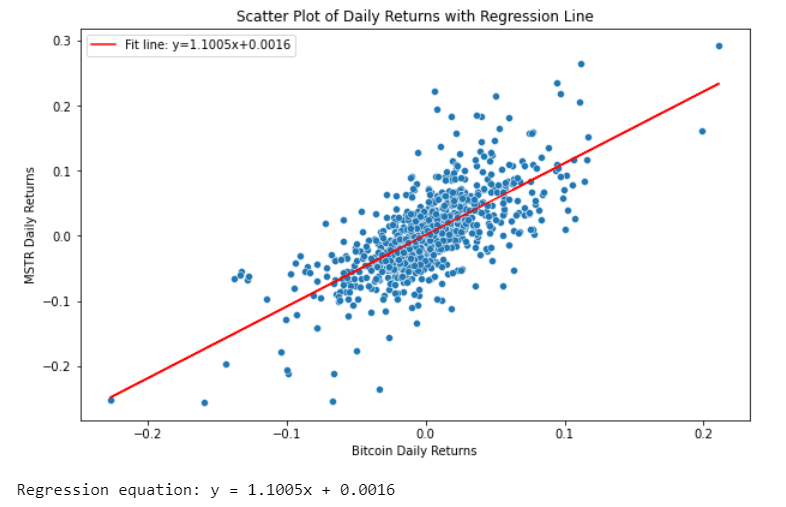

Secondly, MSTR is a leveraged business and there is a persistent upward drift added to this leverage. As BTC goes up, MSTR can go up higher. But as BTC goes down, MSTR maintains some buoyancy. This can be seen in the following scatterplot and regression line using daily returns of MSTR and BTC since January 2021 (just after MSTR started its now famous Bitcoin strategy).

MSTR and BTC Daily Returns Scatterplot and Regression (Author)

The y-intercept of 0.0016 is, for lack of a better word, alpha. MSTR is about 1.1x more volatile than BTC, which is a reflection of a leveraged capital structure, but MSTR’s daily returns have 16 basis points of daily upside bias on average. This daily upside bias obviously compounds because MSTR has far outperformed merely 1.1x BTC over the time frame within the length of this study.

MSTR and BTC (Seeking Alpha)

The third thing is that MSTR is an operating business and they could eventually explore ways to extract income from the BTC treasury itself. As a simple example, they could loan out BTC and earn a return. With the advent of a few new developments in crypto, it would also be possible to stake BTC to secure other blockchains and earn an income. Because MSTR is the biggest corporate holder of BTC, they have a unique competitive advantage in monetizing the treasury in this regard.

All three of these facts point to MSTR’s premium being justified. It could and probably will even expand over time. This is a pretty bleak fundamental picture for the shorts. If the long BTC, short MSTR trade becomes more crowded, we could see an MSTR short squeeze causing the current premium to explode much higher. Even though BTC would likely increase in such a scenario and prevent these traders from blowing up their accounts, the short squeeze would still happen on MSTR, leading to extremely wild upside.

And to bring this back to the stock split, the subsequent increase of liquidity and interest in MSTR options will allow a gamma squeeze to make a short squeeze scenario even more extreme. The most potent component here is the short-dated options with very high gamma and with a price that is low enough for average retail traders to pile in en masse. It all starts with the stock split.

Risks

The main risk to this thesis is the BTC price action. In the last three months, this has been quite unimpressive. MSTR, as a leveraged BTC play, has seen very choppy trading. The stock split and subsequent consequences regarding the options markets won’t really matter if BTC’s price doesn’t start outperforming soon.

As I write this, BTC is currently sitting in bear market territory with an over 20% drawdown from the peak set in March. The sentiment hasn’t been great with the observation of the German government selling its BTC holdings and Mt. Gox creditors potentially liquidating their settlements.

I also think that it is good to remain level headed when considering Bitcoin. It is very easy to get sucked into narratives that are detached from reality. I wholeheartedly disagreed with the narrative that the spot ETF inflows represented broad bullishness on BTC from Wall Street. I presented that case in an article titled “Bitcoin Reality Check.” This MSTR thesis doesn’t go far without good BTC price action.

The other risk is that the options liquidity does not pick up like what I am forecasting. I think a robust way to measure this is to see if the open interest on MSTR options expands by more than a factor of 10 a few weeks after the split. This would signal that people who have been priced out of the MSTR options market are now able to come in.

If open interest does not pick up, then I think we can disregard the thesis of people selling more puts to set a buy wall or resistance point. However, I would see this as neutral on the probability of a gamma squeeze scenario playing out. Those things are a bit like black swan events: massively consequential but very unpredictable in terms of when they might occur. I do believe that lowering the minimum buy-in size of option contracts sets favorable conditions.

The Bottom Line

MSTR is now more ready than ever to see parabolic rallies thanks to its unique positioning as the publicly traded company with the most BTC. The adoption of BTC treasuries by more companies, such as the recent news with Semler Scientific, will only enrich MSTR even more as an early adopter. The stock split is bullish when we consider it in light of the other factors at play.

I am reinstating my buy rating on MSTR. I think we’ll soon see higher highs with BTC and MSTR is sure to benefit.

Read the full article here