Introduction

I have to say I do not have many regrets when I think of investments I made in the past few years. I still own most of the companies I bought for my dividend growth portfolio since the pandemic, and I did not sell anything at a loss. While that may sound a bit cocky, note that I have a multi-decade investment horizon when I place an investment. My turnover is extremely low.

That said, my biggest regrets are stocks I did not buy – especially stocks that I gave a (Strong) Buy rating in the past. One of these companies is General Electric Company, which is now named GE Aerospace (NYSE:GE) after spinning off all non-aerospace segments.

My most recent article was written three months ago when I wrote: “Up 45% Since October: Is General Electric’s Rise Sustainable?”

Since then, GE is up another 30%! It’s now up 92% since I restarted coverage on June 10, 2023.

Writing this gives me mixed feelings. I was right, but I missed the entire rally because I did not want to add more exposure to my portfolio, which already included 22% aerospace & defense exposure.

In this article, I’ll update my thesis and explain why I’m set on buying GE stock this time – regardless of my massive position in the industry.

So, let’s get to it!

A Wide Moat Giant In The Right Place At The Right Time

On May 23, I wrote an article titled Higher For Longer? 3 Of My Favorite Dividend Stocks I Expect To Keep Flying. GE Aerospace was included.

In that non-focused article, I discussed one of the things that stands out when dealing with this aerospace giant: its moat.

An economic moat is a metaphor that refers to businesses being able to maintain a competitive advantage over their competitors in order to preserve market share and profits. Any method that a company uses to maintain a competitive edge can be considered an economic moat. – Investopedia

Wall Street Prep

GE Aerospace is a wide-moat player. In fact, I would make the case that there are not many companies with bigger moats.

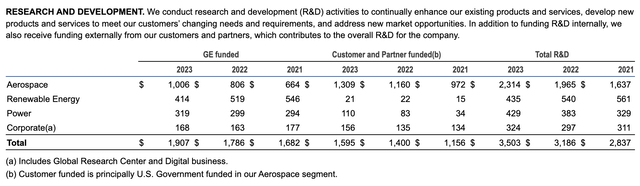

One of the reasons is research and development (“R&D”). Aerospace R&D is what drives innovation.

In the case of GE, the company benefits from its major footprint in defense, as it powers aircraft like the F-15 and F-16 through its F-110 engine platform. This makes the company a major partner of the government, benefitting its R&D.

Using last year’s numbers, GE Aerospace spent $2.3 billion on R&D! $1.3 billion of this was funded by customers and partners – that’s almost exclusively the U.S. government.

GE Aerospace

This innovation paves the road for an advantage in commercial aviation.

Even ignoring R&D, the relationships the company has with governments and airlines are hard to compete with, as it has become a trusted partner for many decades. Furthermore, adding to its moat are replacement costs, maintenance, and complexity.

Although commercial aviation went mainstream more than 60 years ago, the ability to produce highly complex engines is still limited to a few global players.

The GEnx engine, for example, includes more than a million parts that rely on a highly complex supply chain spanning multiple nations.

GE Aerospace

Furthermore, in the wide-body engine market, the company has a duopoly, with a total engine market share of 14%, which excludes its joint venture called CFM International, which has a 39% market share.

GE estimates three-quarters of commercial flights are powered by GE or GE joint venture engines. Its CFM International joint venture supplies 100% of 737 MAX engines and 60% of A320 engines, and independently it supplies widebody and regional aircraft engines. Its large installed base of engines provides ongoing predictable revenue through maintenance, repair, and replacement components independent of new aircraft deliveries. – S&P Global

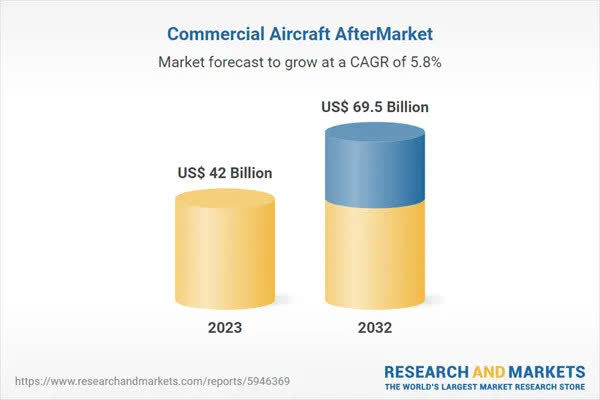

When adding that the company makes up to 65-70% of the total engine value through aftermarket sales and maintenance over the lifespan of an engine, we get an even stronger moat that is almost impenetrable for new entrants.

After all, not only are engines getting better, allowing them to be used longer, but we’re also dealing with a rapidly expanding installed base!

According to Research And Markets, the commercial aircraft aftermarket is expected to grow by 5.8% to roughly $70 billion by 2032.

Research And Markets

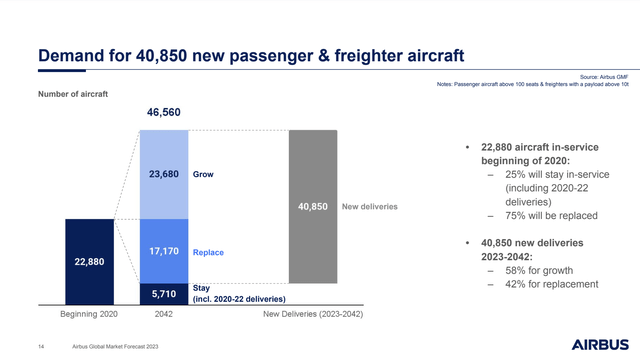

Moreover, Airbus SE (OTCPK:EADSF) expects demand for almost 41,000 new aircraft through 2042 – with less than half of these planes being replacement planes!

Airbus

Even better, as we have left the pandemic behind us, we’re going back to “normal,” which is soaring commercial aerospace demand.

As reported by Reuters on June 3 (emphasis added):

The International Air Transport Association (IATA) said it expected the worldwide industry to generate $30.5 billion of profit this year, higher than an upwardly revised $27.4 billion in 2023 as carriers keep a lid on underlying labour costs despite recent strikes.

That comes just four years after the industry collapsed to a $140 billion loss in 2020 as a result of the pandemic and is above the $25.7 billion forecast for 2024 issued in December.

“The environment is better than we had expected, particularly in Asia,” Director General Willie Walsh told Reuters on the sidelines of an annual meeting of IATA’s more than 300 members, which account for more than 80% of global air traffic.

While the road ahead will see some bumps and obstacles, I have little doubt that commercial aerospace continues to be the place to be for elevated long-term gains. This also applies to GE Aerospace – despite its latest rally.

The Risk/Reward Remains Good

In addition to the company’s wide-moat characteristics and longer-term demand tailwinds we discussed in the first part of this article, the company is hitting it out of the park financially.

For example, in the first quarter, the company reported significant growth across all key metrics:

- Orders grew by 34%, with revenue rising by 15%. This was driven by pricing, increased spare parts volume, and higher wide-body and defense engine deliveries.

- The operating profit surged by 24% to $1.5 billion, with margins expanding by 140 basis points to 19.1%.

- Free cash flow also doubled to $1.7 billion.

In addition to generating a ton of free cash flow, the company has plans to return 70-75% of its free cash flow to investors.

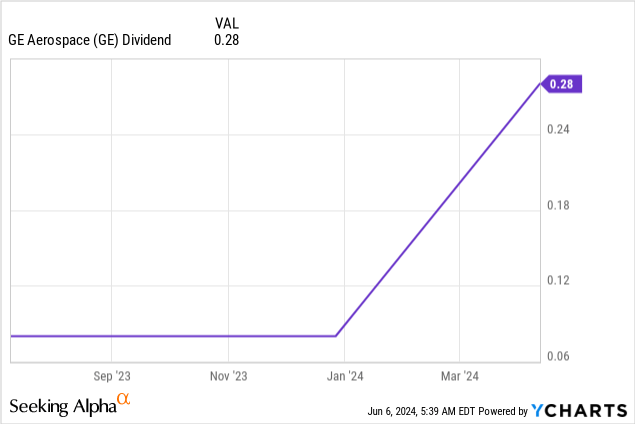

The company hiked its dividend by 250% to $0.28 per share per quarter. This translates to a yield of 0.7%. It also initiated a $15 billion buyback program, valued at more than 8% of its market cap.

While this dividend yield is disappointing, the company is on the path to generating $7.1 billion in free cash flow in 2026 (16% CAGR), which would translate to a free cash flow yield of 4%, indicating a lot of room for dividend growth (and buybacks).

It also enjoys a super healthy balance sheet with a sub-1x leverage ratio. In other words, I think it’s fair to call GE a dividend growth stock.

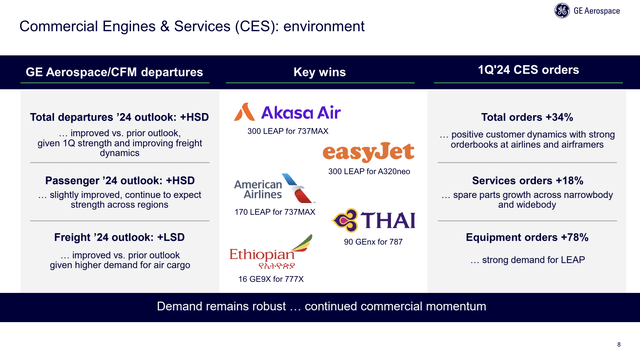

Going back to growth drivers, the Commercial Engines & Services (“CES”) segment, which is a $24 billion business with 70% from services, saw orders increase by 34% in the first quarter.

This growth was driven by strong demand for LEAP engines and spare parts across multiple platforms, with major wins including more than 300 LEAP-1B engines for Akasa Air and significant contracts for wide-body engines with Thai Airways, Ethiopian Airlines, and LATAM Group.

GE Aerospace

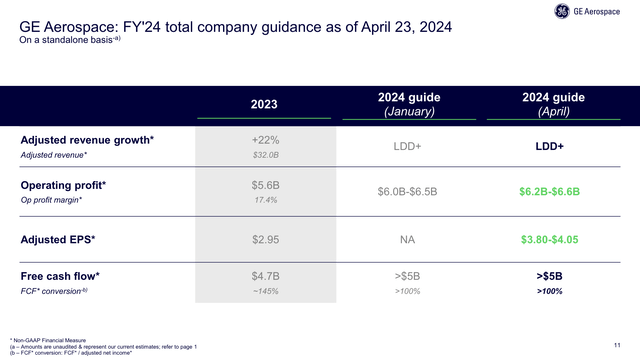

Meanwhile, the defense segment saw 34% higher orders, resulting in a 1.1x book-to-bill ratio ($1.10 in new orders for every $1.00 in finished work). Growth was so strong that the company upped its guidance, expecting at least $6.2 billion in full-year revenues – up from $6.0 billion. It is also expected to turn more than 100% of its net income into free cash flow, which is a sign of earnings quality.

GE Aerospace

So, what does this mean for shareholders?

Valuation

If I said GE Aerospace is cheap, I would be lying. After its impressive rally, it’s far from cheap. However, I’m comfortably sticking to my Buy rating.

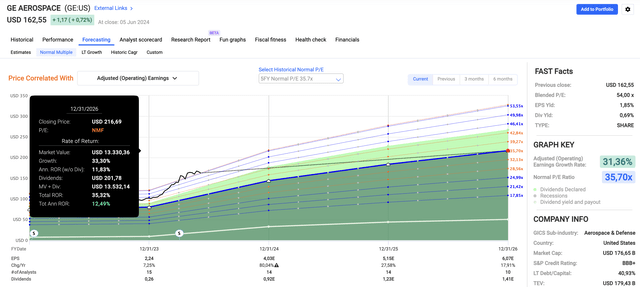

Using the FactSet data in the chart below, GE trades at a blended P/E ratio of 54.0x, which seems like a lofty number.

The good news is that this year, EPS is expected to grow by 80%, potentially followed by 28% and 18% growth in 2025 and 2026, respectively.

FAST Graphs

As such, I believe it is fair to apply its five-year normalized P/E ratio of 35.7x. This would imply an annual return of 12.5%, giving GE a fair stock price target of $217, 33% above the current price.

Currently, I’m looking for an entry, which includes managing my cash reserves, after I have been an aggressive buyer of a few companies this year, including Texas Pacific Land Corporation (TPL) and Old Dominion Freight Line, Inc. (ODFL), which accounted for a big part of my cash.

In other words, I don’t have as much cash, as I did not expect to start two new (so far) positions this year.

Nonetheless, while further expanding a 22% aerospace position may go a bit far, I have little doubt GE is one of the best wide-moat stocks on the market – even at these prices.

Takeaway

Looking back at my investment choices, I’m mostly satisfied, but missing out on General Electric (now GE Aerospace) still stings.

Since restarting coverage in June 2023, GE is up 92%.

The company’s strong moat, driven by its extensive R&D, partnerships, and dominance in both commercial and defense sectors, makes it an industry leader. Financially, GE is thriving as well, with impressive growth in orders, revenue, and free cash flow.

Although the stock isn’t cheap after its rally, its future growth potential keeps it on my buy list. Despite my already substantial aerospace exposure, I’m set on adding GE to my portfolio as soon as possible.

Pros & Cons

Pros:

- Wide Moat: GE Aerospace has an impressive moat, driven by significant government-supported R&D investments, a huge market share, and strong customer/supplier relationships.

- Financial Strength: The company has shown a strong financial performance with double-digit growth in orders, revenue, and free cash flow.

- Dividend Growth: The recent dividend hike and a $15 billion buyback program are a good start to what is likely to be a long period of elevated dividend growth.

- Market Dominance: GE powers a significant portion of global commercial flights, with a massive market share in both narrow-body and wide-body engines.

- Growth Potential: GE has favorable growth projections for EPS and free cash flow, with a fair stock price target 33% above the current price.

Cons:

- Valuation: After its impressive rally, GE isn’t cheap. Its current P/E ratio is lofty, which might limit short-term upside. It also leaves GE little room for error when it comes to reporting future financial results.

- Market Volatility: The aerospace industry can be volatile, with external factors like geopolitical tensions and economic downturns impacting its performance.

Read the full article here