Today’s article covers MoneyLion Inc. (NYSE:ML), a cutting-edge consumer finance platform with an integrated business model.

MoneyLion’s stock has surged by more than 580% in the past year as its scalable solutions have provided tangible results. However, the question now becomes: Is MoneyLion stock overvalued, or does it have more in store?

To address the central question, we assessed various fundamental aspects and market-based indicators and concluded that MoneyLion could increase its year-over-year returns; here’s why.

Seeking Alpha

What Is MoneyLion?

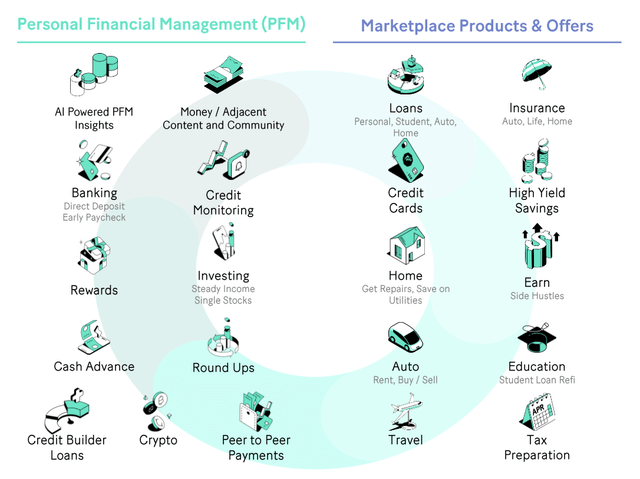

MoneyLion is a fintech application for low-credit borrowers and small check investors. The following diagram summarizes its key offerings, and a discussion follows.

Key Offerings (MoneyLion)

MoneyLion has two segments, namely its consumer business and enterprise solutions.

The company’s consumer business generates income from digital banking fees and investment platform administration. Moreover, the segment earns revenue from subscription services, such as its MoneyLion Plus offering, which withdraws a fixed amount from a client’s bank account each month, places it into an investment account, and rebates the client based on his/her platform engagement.

On the other end, MoneyLion’s enterprise segment generates income from marketplace activities and media services. In a basic sense, MoneyLion works with more than 1,100 external partners to facilitate its array of services. This allows MoneyLion to earn incentives by driving traffic to its partners, whether that be a financial institution or a general advertiser.

The following diagram summarizes MoneyLion’s segmental returns.

MoneyLion

What We Like About MoneyLion’s Stock

Systematic Support

The fintech space is experiencing rapid growth due to reasons such as digitalization, decentralization, niche market targeting, and higher engagement in investable assets such as deposit accounts and stocks. In fact, Fortune Business Insights forecasts Fintech will grow by 16.5% per annum until 2032, providing a healthy multiplier to interested investors.

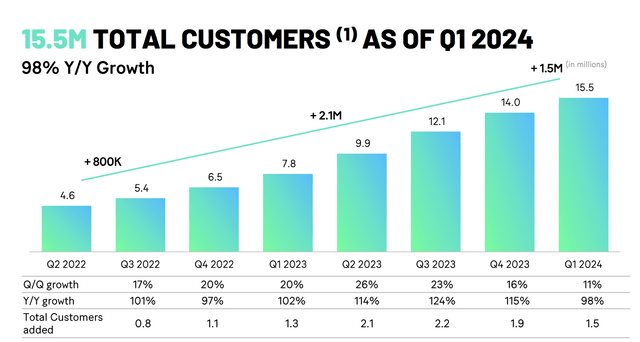

The industry/sector’s embedded growth has clearly assisted MoneyLion as the firm’s customer base is surging. In fact, it experienced 80 million inquiries in Q1 alone, converting 1.6 million of them into customers.

MoneyLion

Novelty

Fintech is a crowded arena, meaning novel solutions are required. MoneyLion’s novelty is of the essence.

MoneyLion differentiates itself from the pack in a few ways. Firstly, as mentioned in the previous section, it relies on lower credit score borrowers without assuming counterparty risk. We think this is a clever move as it allows access to a broad pool of borrowers while minimizing risk.

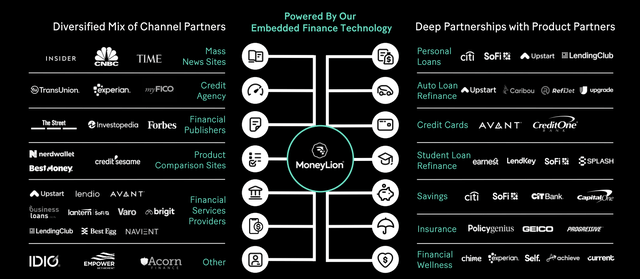

Furthermore, we believe MoneyLion’s lead generation business is a value-add. Lead generation isn’t a new concept. However, MoneyLion’s model aligns as it leverages modern machine-learning techniques to consolidate accurate targeting. Additionally, the firm’s partnerships are aligned with its core business model, which is lending. As such, it isn’t just another website selling affiliate ads; no, it’s an integrated debt intermediary with highly sophisticated technology, allowing for exponential growth prospects.

MoneyLion’s Key Partnerships (MoneyLion)

Tangible Financial Success

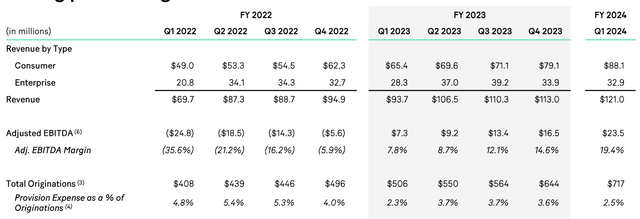

MoneyLion isn’t just a nice story; it has achieved actual financial success. The firm delivered $121 million in revenue during its latest operating quarter (Q1), surpassing estimates by $4.69 million. Additionally, MoneyLion provided positive guidance, stating it anticipates Q2 revenue to grow between 17% and 22% year-over-year to between $125 million and $130 million.

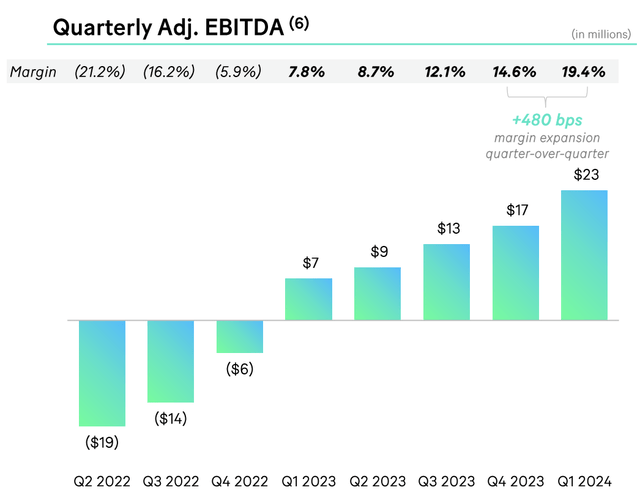

Furthermore, MoneyLion is EBITDA positive, an achievement it reached a year ago. Moreover, as visible in the diagram below, MoneyLion’s EBITDA margin has grown ever since, suggesting it might be a margin expansion story.

Q1 Results (MoneyLion)

Lastly, MoneyLion has a strong cash position. Its balance sheet hosts approximately $93.2 million in cash and $44.6 million in net receivables, allowing MoneyLion’s management to reinvest in its business model with relative comfort. Additionally, its strong cash position reduces solvency risk, a risk factor often emphasized by investors.

What We Don’t Like

The Credit Environment & Subsequent Effects

Despite benefiting from higher engagement in the past year, we believe much of it was purely due to rising loan inquiries and rising popularity in high-risk stocks. However, we foresee an altered credit market occurring in late 2024/early 2025, providing a reason to tread cautiously.

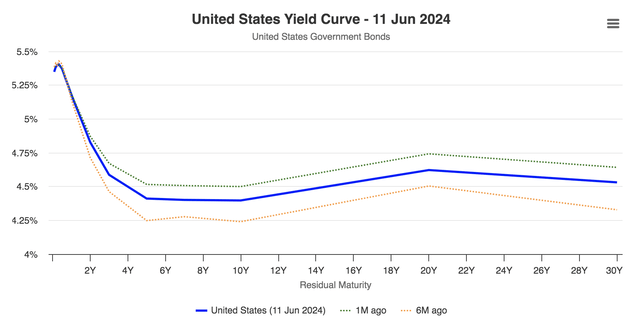

Why do we think the credit market might experience changes? Firstly, the U.S. yield curve moved lower in the past month, suggesting lower implied interest rates are likely. Moreover, as explained later, lower rates will probably occur due to economic softening.

U.S. Yield Curve (worldgovernmentbonds.com)

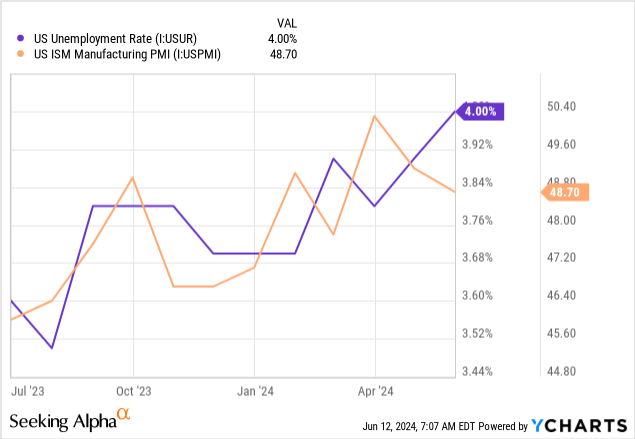

A lower interest rate view aligns with our view as we think rising unemployment rates, wavering consumer sentiment, and sub-50 PMI indicate that an expansionary monetary cycle is likely. A lower interest rate environment might spike credit spreads due to the general inverse relationship between interest rates and credit risk premiums. Additionally, real economic factors might play a role and heighten loan liquidity and default risk.

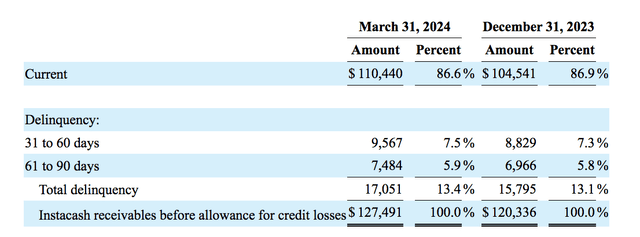

A rise in credit spreads might exacerbate the delinquency rates on high-yield consumer credit. In fact, delinquency rates in the auto, credit card, and home loan sectors have already started rising. Moreover, delinquency rates on MoneyLion’s instant cash portfolio, which offers instant loans (mostly below $1000), have started climbing, providing additional evidence that rising credit risk might be en route.

MoneyLion 10-Q

Rising credit risk might lower the appetite of banks to lend to low-credit consumers.

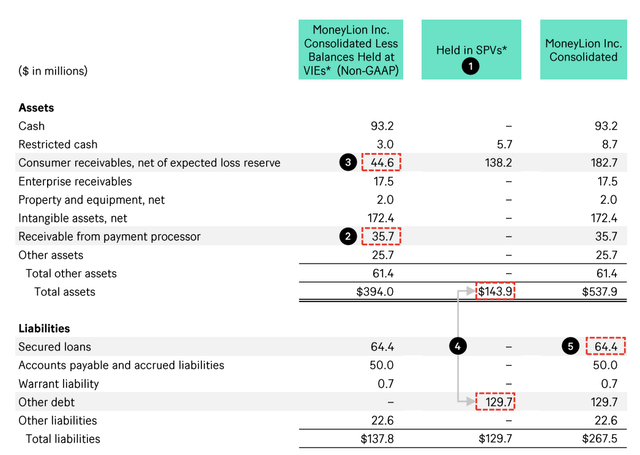

SPV Risk

MoneyLion has a special-purpose vehicle (SPV) that it uses for credit arrangements. According to our understanding, the company currently has around $129.7 million (12.55 interest rate) in available credit secured by this SPV.

Our issue is that the credit facility is secured by receivables, and, as mentioned before, we are worried about delinquency rates and their subsequent influence on partnership revenue. As such, we believe MoneyLion’s option to use SPVs to onboard credit is risky.

MoneyLion

Rising Industry Competition

Another concern is MoneyLion’s rising industry competition. For example, it is competing with companies like LearnVest, Betterment, and even JPMorgan (JPM), which recently launched its no-fee app, YouInvest.

A rising concept introduces rising competition. Thus, the question beckons: Will MoneyLion outpace its competitors? Only time will tell, but we think rising competition is always a risk factor.

Valuation & Technical Analysis

Some might argue that MoneyLion’s stock has reached overvalued territory after its year-over-year surge. However, we argue it remains relatively undervalued, as its forward price-to-sales (P/S) ratio of 1.72x falls below some of those of its peers. Moreover, the company has illustrated exceptional revenue growth, suggesting its P/S ratio is well-placed.

| Variable | Value | Sector Median |

| Price-to-Sales | 1.87x | 2.53x |

| Forward Price-to-Sales | 1.72x | 2.44x |

| 3-Y Revenue CAGR | 67.70% | Link To Peer Comparison |

Source: Seeking Alpha

We decided to focus on MoneyLion’s P/S ratio as it is an early-stage growth company likely focused on scalability instead of efficiency. Nevertheless, let’s conduct a technical analysis of MoneyLion’s stock to consolidate our argument.

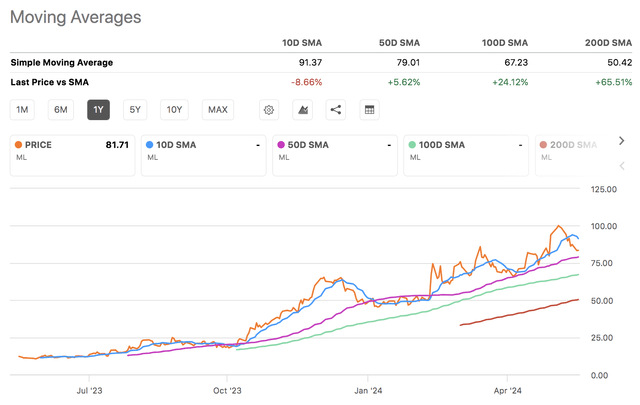

MoneyLion’s simple moving averages show that it recently dipped below its 10-day moving average while remaining above its 50-, 100-, and 200-day moving averages. This might signal a trend reversal. However, we think MoneyLion’s relative strength index of 48.23x and its put/call ratio of merely 0.28 contradict this notion. In essence, we expect the trend to resume.

Seeking Alpha

Final Verdict

We think MoneyLion’s stock is well-placed and ready for additional upside. Although risks such as a questionable credit market outlook and rising competition might present obstacles, we remain positive.

In our view, MoneyLion’s exponential growth stems from systematic support and novel features. Its consumer segment is experiencing high engagement, likely due to its unique subscription service and data-driven debt market targeting. Furthermore, MoneyLion has interesting enterprise solutions, including high-volume external party engagement, allowing for multiple revenue streams.

Lastly, our analysis of MoneyLion’s valuation and technical indicators suggests relative value is in store.

We hereby assign a buy rating to MoneyLion.

Read the full article here