Investment Thesis

MoneyLion Inc. (NYSE:ML) is one of my favorite inflection stocks (yes, I own it). What makes it an inflection stock? It means two key factors are at play: a stable customer adoption curve and increasing free cash flows.

A stable adoption curve doesn’t necessarily mean rapid growth all the time. Instead, stability means the business is predictable, which is crucial. Why?

Because a consistent level of customer demand increases the multiple that investors are willing to pay. As an inflection investor, getting the multiple right can be the difference between thriving and struggling in 2024.

Moreover, if a business can grow rapidly without taking on debt, it becomes even more attractive. ML excels at expanding its business without incurring debt, making it significantly undervalued. Unlike many other similar banks, ML’s unique ability in this area will earn it a higher multiple over time.

So, here’s why I’m very bullish on ML.

Price target of $125 by mid-2025.

Why MoneyLion? Why Now?

MoneyLion is a financial services company that leverages technology to offer accessible and cost-effective financial solutions to consumers. They excel in streamlining the process of obtaining financial products like credit cards and loans.

One of MoneyLion’s standout features is its ability to acquire new customers discounted to the cost typically incurred by other companies. This efficiency enables them to offer their services at significantly lower prices, making financial products more accessible to a broader audience.

By utilizing social media and user data, MoneyLion provides personalized financial recommendations and products tailored to individual needs and preferences. Similar to how social media platforms use personal information to curate content and ads, MoneyLion uses financial data to offer relevant financial products.

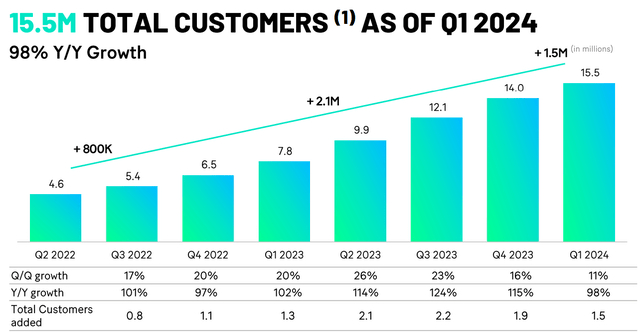

ML investor presentation

As illustrated above, ML’s customer adoption curve continues to thrive. It’s impressive that since I started recommending this stock, they’ve grown from just under 10 million to nearly 20 million customers. These figures are no longer insignificant.

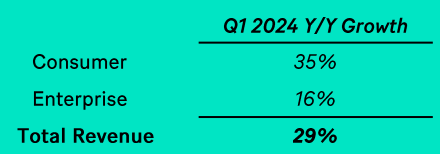

Moving on, can MoneyLion sufficiently grow its Enterprise segment so that it could be viewed more as a fintech providing software to enterprise customers? Naturally, if that narrative were to unfold, this would lead to its stock being valued as a SaaS stock rather than a neobank stock.

ML investor presentation

In case you’re unfamiliar with the difference, software services are rewarded with a P/Sales ratio, while consumer neobanks, even lending banks without significant debt, are valued with a banking multiple. For now, this is an interesting, but largely theoretical debt, since ML’s stock is so cheap, but it’s something I’m keeping an eye on moving forward.

Given this context, let’s discuss its financials in more detail.

MoneyLion To Grow At 20% CAGR in 2024

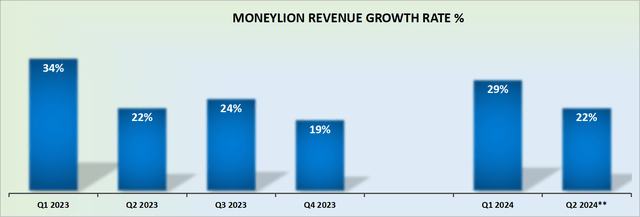

ML revenue growth rates

MoneyLion’s Q1 2024 results delivered the strongest revenue growth in the fastest in the last four quarters. Let this sink in. This company is demonstrating to all that its growth days are not in the rearview mirror. Is this significant? Oh my, yes. If you get a profitable growth company that can reaccelerate its growth rates, you get what I call a bananas multiple on the stock.

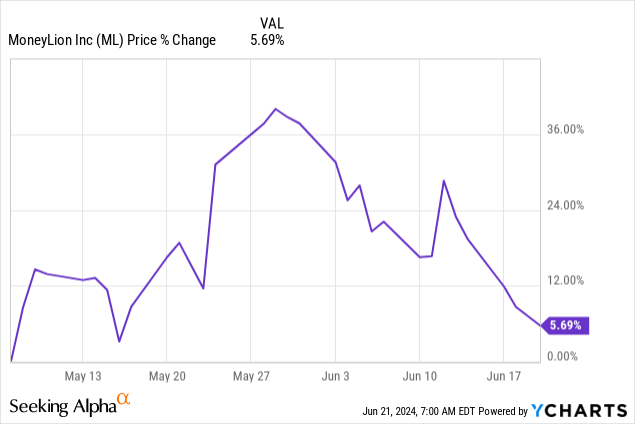

And what I find most fascinating, is that since MoneyLion’s Q1 2024 results came out on 7 May, the stock has barely moved higher.

So, not only do you have a business that is rapidly growing, but more importantly, you have a business that just delivered an acceleration on its topline. And to flummox matters, the market appears demonstrably disenchanted?

I know this sounds really difficult to believe, but the market will reward businesses with strong free cash flow again. Just like the night turns to day. It won’t always be out of favor.

ML Stock Valuation — 7x EBITDA

In the past, I believed that ML could be on a path towards $100 million of EBITDA at some point in 2025, as a forward run rate.

Now, consider this. For Q1 2024, EBITDA margins stood at 19%. However, context matters. Let’s look back to what ML was previously guiding for Q1 2024.

ML Q1 2024 results

ML stated guided for an EBITDA margin of 15% at the high-end for Q1 2024. However, when its EBITDA figures ultimately came out, they were 400 basis points higher.

Consequently, when ML guides for about 16% EBITDA margins at the high end for Q2, I’m thoroughly convinced that they will, in fact, reach this.

Consequently, I now believe that ML should be able to reach 19% EBITDA margins by the time it exits 2024. Altogether, I believe that ML could probably reach $110 million of EBITDA, as a forward run-rate at some point in early 2025.

This puts the stock priced at approximately 7x EBITDA. Bargain. A total bargain.

The Bottom Line

In conclusion, MoneyLion Inc. stock is undeniably compelling, particularly when considering its current valuation at approximately 7x EBITDA.

As an investor, I am convinced that this valuation significantly underestimates the company’s potential for growth and profitability. With MoneyLion’s demonstrated ability to efficiently acquire customers and expand its revenue streams, coupled with its trajectory towards higher EBITDA margins, ML stock presents itself as a steal at its current price.

Read the full article here