Investment Thesis

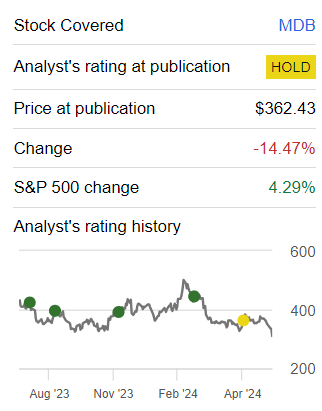

MongoDB (NASDAQ:MDB) sees its stock fall 25% premarket. And here’s how I described MongoDB last time.

Author’s work on MDB

The problem for investors is that high-growth companies rarely go on sale. They only go on sale when the outlook is horrid. And up until that moment, growth stocks carry a growth premium.

As such, even after the premarket drop, MongoDB is still priced at 85x forward non-GAAP EPS. An exorbitant figure. Consequently, I argue, that investors would do well to call it a day here before things get even cheaper. As MongoDB’s high valuation isn’t reflective of its underlying prospects.

Rapid Recap

Last month I said,

I fail to see the appeal of paying more than 80x forward non-GAAP operating profits for this stock. Therefore, I’m now moving to the sidelines on this one.

Author’s work on MDB

As an investor, you are forced to make tough decisions. Do you recognize that you are wrong and move to the sidelines? Or do you double down on your conviction irrespective of the facts?

Last month I was forced to make this decision. I decided to go to the sidelines on MDB after I’ve been a strong bull over the past year (see above). Today, with the benefit of hindsight, we can see that this was the right decision to make. And now, looking ahead, I’m severely questioning the appeal of this stock.

MongoDB’s Near-Term Prospects

MongoDB provides a way for organizing and handling data, making it easier for developers to build applications, especially ones that handle a lot of different types of data.

As noted during the earnings call, one of its key issues pertains to the slower-than-expected growth in Atlas consumption. This slowdown was higher than anticipated at the beginning of the fiscal year.

MongoDB notes that recently acquired workloads have started to slow down earlier than expected. Despite fine-tuning the process and incentive structures to focus on higher growth potential workloads, the operational adjustments took time to take effect, resulting in a less-than-stellar performance in new business acquisition for Q1.

Given this background, let’s now discuss its fundamentals in more detail.

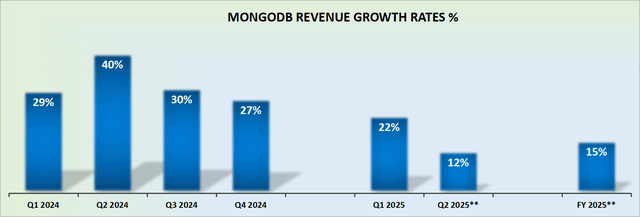

MongoDB Reduces Its Revenue Guide

MDB revenue growth rates

Certain companies are given the benefit of the doubt that they are being conservative with their guidance until it’s clear that they are not being conservative, but rather accurate.

MongoDB is guiding for approximately 15% CAGR for this fiscal year. That’s the best-case scenario. This is a company that many investors, myself included, were bedazzled by its narrative.

A narrative that overly stressed the growth and prospects of its MongoDB Atlas, while disregarding the fact that its Atlas cloud business was simply cannibalizing its legacy on-premise business. This is akin to moving money from one pocket to another, resulting in no real change.

With this framework in mind, let’s discuss its valuation.

MDB Stock Valuation — 85x Forward Non-GAAP EPS

Previously, investors were expecting MongoDB to not only reach $2.50 of non-GAAP EPS this year but potentially even increase this EPS figure slightly towards $2.70 or thereabouts. Indeed, investors would have been eyeing up $3.00 of non-GAAP EPS at some point in the next several quarters as a forward run-rate.

However, given that MongoDB has now downwards revised its non-GAAP EPS guidance to approximately $2.30, it seems highly likely that even by fiscal 2026 (the next fiscal year), MongoDB will not reach this high earnings per share target. This would necessitate MongoDB’s underlying EPS growing by 30% y/y. A figure that strikes me as punchy and unreasonable, particularly given that MongoDB’s topline is growing at approximately 15% CAGR.

Consequently, a more realistic figure for MongoDB to reach at some point in the next twelve months will be around $2.70 of non-GAAP EPS. This leaves MongoDB priced at 85x forward non-GAAP EPS. A valuation that is wholly unjustified for what MongoDB offers investors.

Upside Risks — Why The Stock Could Rally From Here

MongoDB has a long history of being conservative with its guidance. Management could be acting conservatively with its guidance and next quarter, after a short recent, its growth rates could once again reaccelerate.

Furthermore, despite recent challenges, the company’s focus on high-growth segments like MongoDB Atlas and AI-powered app modernization presents opportunities for future expansion.

As organizations increasingly prioritize digital transformation and AI integration, MongoDB’s flexible document-based architecture positions it as a key player in a rapidly growing total addressable market.

The Bottom Line

In conclusion, MongoDB’s high valuation and challenges in Atlas consumption growth, should prompt many investors to reconsider its prospects.

Despite its innovative data management solutions for developers, the company’s near-term prospects are clouded by slower-than-expected growth and downward revisions in revenue guidance.

As an investor, it’s crucial to weigh the narrative against the underlying fundamentals, especially considering MongoDB’s high forward non-GAAP EPS multiple of 85x.

All in all, I believe there are much better stocks to buy right now than MDB.

Read the full article here