When I last wrote about Roche Holding AG (OTCQX:RHHBY), I was worried that a lackluster near-term revenue and profit outlook, coupled with a questionable pipeline and what I regard as uninspired management, raised the risk that the stock would languish as a value trap, with iffy pipeline productivity driving the company toward more M&A to reinvigorate the clinical side and boost future growth prospects.

Since then, the shares are down slightly and have modestly unperformed the broader pharma space and management has spent over $10B to add assets through M&A.

My outlook isn’t substantially different now, though I do want to note that the company has some interesting later-stage portfolio assets that could drive an improved outlook. I still believe, though, that there’s a lot that needs to be fixed here and I still think the diagnostics business is “under-managed” relative to what it could be. I still see high single-digit total annualized return potential here, but I’d note that the 5-year and 10-year returns are only in the low single-digits, well below the double-digit returns of the industry, and I remain concerned that management isn’t focused on the right value drivers.

A Familiar Story… But Maybe A Better Outcome This Time

Looking back to 2018, the Street was very much worried about Roche’s growth prospects in the face of looming biosimilar competition for Avastin, Herceptin, and Rituxan (around 40% of company revenue at the time). It was hoped then that new drugs like Hemlibra, Ocrevus, and Tecentriq could “mind the shop” and deliver interim growth augmented by high-potential clinical candidates like balovaptan, etrolizumab, gantenerumab, HTT-ASO, and Vabysmo.

How did that all work out?

Hemlibra and Ocrevus have been great drugs for Roche, and it’s hard to fault Roche’s commercial execution here. Tecentriq has been disappointing, and particularly here of late as the drug has been losing share to Merck & Co., Inc.’s (MRK) Keytruda in adjuvant lung cancer and has missed expectations for five quarters in a row, with growth slowing to the single-digits.

Of the high-potential pipeline candidates, only Vabysmo has come through (and it has been great), though I think you could add Evrysdi and Polivy as winners that were underappreciated at the time.

The situation today isn’t so serious, with only Actemra (4% of Q1’24 sales), Xolair (about 3.5% of sales), and Perjeta (6.5% of sales) at risk of biosimilar competition through 2026. But the company’s overall performance has decelerated, with less than 2% annualized revenue growth over the past decade (and a similar growth rate back to 2006).

Looking at the pipeline today, tiragolumab (an anti-TIGIT antibody for cancer) could be a winner, but the key data from a commercialization perspective likely won’t be available until 2027, and Gilead Sciences, Inc. (GILD) could be a threat here. Gazyva in lupus could be worthwhile (the upcoming REGENCY trial is key), as could follow-on studies for Venclexta and Lunsumio, but these add-ons don’t tend to drive the same investor interest.

With that, a lot is riding on compounds like giredestrant (a potential best-in-class SERD inhibitor), prasinezumab (Parkinson’s), zilebesiran (for hypertension, partnered from Alnylam Pharmaceuticals, Inc. (ALNY)), divarasib (a strong KRAS candidate), RG6631 (previously known as RVT-301 and acquired for over $7B in 2023), and CT-388, the dual GLP-1/GIP receptor agonist for obesity that Roche acquired in the Carmot deal ($3.1B including milestones) in late 2023.

Tiragolumab could be a $6B-plus drug at its peak, prasinezumab could peak at over $5B (and it’s possible Roche could file if Phase II data are good enough), RG6631 could peak around $4B, and giredestrant and zilebesiran could peak at over $3B, and divarasib could be a $2B drug. CT-388 is harder to assess at this point; Phase I data were very encouraging (19% average weight loss, with 45% of study participants seeing 20%-plus weight loss) and obesity drugs offer multibillion-dollar potential, but it will be a crowded field when CT-388 gets to market (though still likely a multibillion-dollar drug, to say nothing of combo opportunities).

R&D Productivity – Hard To Measure, But The Data Don’t All Line Up

The notion of R&D productivity has become more popular lately, with multiple pharmaceutical companies addressing it in investor presentations. Unfortunately, there’s no one-size-fits-all way to assess this key driver.

Morgan Stanley’s pharmaceutical analysts looked at productivity in terms of the percentage of Phase I drugs that eventually go on to approval. From 2007 to 2023, Roche was a little better than average at 8.5% (Gilead and Vertex Pharmaceuticals Incorporated (VRTX) led at 18% and 15%, respectively, while Eli Lilly and Company (LLY) and Merck trailed at around 6%).

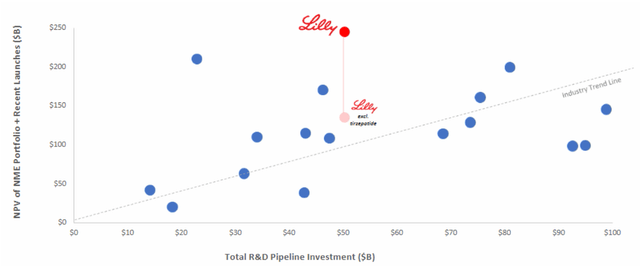

Roche addresses this themselves during their September 30, 2023, Pharma investor event, noting that they spend $5.7B on R&D for each new molecule that is commercialized, putting them a little above the average at $4.7B, with a range of $2.8B to $6.2B. Lilly produced a similar analysis showing that while there is a correlation between R&D spending and value creation, it’s not strictly one-to-one.

R&D spending drives revenue from new drugs (Lilly)

I don’t pretend to have a perfect and proprietary way to analyze R&D productivity, but I will say this much – Roche spends a lot on R&D (around $65B over the last five years, or around 21% of total revenue) and billions more on M&A, but has only generated low single-digit revenue growth over the last decade-plus.

Diagnostics – It Is What It Is

I’ve long been critical of Roche’s Diagnostics business, feeling that management has under-invested in the business and prioritized near-term margins and cash flows over building a more dynamic business over the long term. Compared to companies like Danaher Corporation (DHR) or Abbott Laboratories (ABT), I do still think this criticism is valid, though Roche has continued to do well in areas like molecular diagnostics and tissue diagnostics.

Some of my irritation stems from Roche surrendering leadership in areas like diabetes and life sciences and missing opportunities in areas like cell analysis. The company’s recent presentation for this group was somewhat encouraging, though, with management highlighting a deep portfolio of new tests (including a deep menu of mass spec-based tests to complement its new i601 system for clinical mass spectroscopy), new testing approaches for oncology (including liquid biopsy) and Alzheimer’s, and (at long last), a continuous monitoring solution for diabetes. I also note that management highlighted a nanopore-based sequencing system in development, so Roche may well re-enter the sequencing market against the likes of Illumina, Inc. (ILMN), Oxford Nanopore Technologies plc (OTCPK:ONTTF), Pacific Biosciences of California, Inc. (PACB), and Thermo Fisher Scientific Inc. (TMO) at some point.

The Outlook

My biggest concern at this point is whether or not Roche has the capability to accelerate its earnings and cash flow growth, as 2% trailing revenue growth, 3% trailing EPS growth, and slightly negative free cash flow growth clearly hasn’t been getting the job done. Some of this could be inherent to the nature of running a large multinational pharmaceutical company – backing away from oncology isn’t an option, but that’s a tough market commercially speaking and newer areas of growth like neuroscience are challenging from an R&D/clinical success perspective.

Given that I’m modeling close to 4% long-term revenue growth for Roche (including risk-weighted contributions from the pipeline), I wouldn’t say I’m exactly bearish on Roche. Likewise, I see the company generating mid-30%s operating margins for years to come, as well as FCF margins in the mid-20%’s. Still, I think there’s room for improvement here and that such improvement could unlock more value.

Discounting those cash flows back suggests a fair value today in the high-$30s, and I get a similar value with my EPS-based approach (five-year EPS growth correlates pretty closely to what multiples the market is willing to pay for a large pharma company).

The Bottom Line

With Roche around 10% undervalued today and potentially priced for high single-digit total annualized long-term returns, I still see an argument for owning the shares. While positive pipeline developments could unlock even more growth and value, the flip side is true if late-stage studies disappoint or rivals post even better data. All of this said, I have to admit a growing impatience with the trajectory of this business and while I still recommend (and own) the shares, I’ve started considering other options in the space.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here