Investment Thesis

MPC Container Ships (OTCPK:MPZZF) recently reported another strong quarter. Its Q2 earnings were $84 million on revenues of $131 million. It declared a $0.10 dividend, the 11th in a row, bringing its yield to about 28%. 76 percent of 2025 and 42 percent of 2026 are already fixed at reasonably good rates.

Since I took up coverage of MPZZF in Q4 2023, the company has continued executing its fleet optimization strategy. This has resulted in a relatively new fleet on water and low operating leverage for the segment. MPZZF is currently in a net cash position, having $160 million in cash and $132 million in long-term debt as of Q2.

Compared to Q2 last year, revenues and earnings were down 32 and 40 percent, respectively. This drop is expected, given the company’s emphasis on earnings visibility through longer-duration time charters. Consider the HARPEX over the last three years:

Harpex index, 3Y [screenshot from Sep 5, 2024] (HARPEX)![Harpex index, 3Y [screenshot from Sep 5, 2024]](https://wealthbeatnews.com/wp-content/uploads/2024/09/59057848-1725540520213141.png)

In 2023, it was coming off the historically high 2021-22 market rates, while in early 2024, it has been delivering on comparably lower rates seen in 2023.

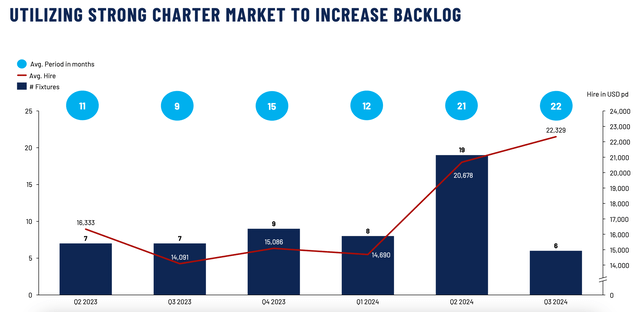

It is now able to re-contract in favorable market conditions. MPZZF also reports that contract durations have become longer. From its Q2 presentation:

Contract duration and fixtures (Q2 earnings presentation)

While it was able to contract out for about 9-11 months in early 2023, MPZZF has inked contracts of more than 20 months’ duration in 2024. The rates are also attractive. This strategy execution provides excellent dividend safety into 2025 and 2026.

Combined with the underinvestment in the feeder segment in which MPZZF operates, this company is a vehicle for exposure to a sometimes forgotten part of the global logistics supply chain: the feeders. Its shareholder-friendly communication and capital returns policy makes it well-suited for dividend investors. This segment will reach the end of the cycle later, and I am rating it a buy.

Short Company Overview

Incorporated in 2017, MPC Container Ships is an Oslo Stock Exchange-listed, Norway-domiciled tonnage provider in the intra-regional and regional (feeder) container segments.

It owns and operates a fleet of 59 ships, ranging in size from 1,200 to 5,500 TEU. In 2024, MPZZF has sold 11,600 TEU capacity, with a TEU-weighted age of 17.2 years. In the same period, it acquired 7,000 TEU capacity (avg. age 15 years) and one 1,300 TEU newbuild scheduled for delivery in 2026. These transactions have contributed to bringing the average age of its fleet down to 13.9 years.

Risks

MPZZF trades in NOK on the Oslo Stock Exchange, a relatively illiquid currency on a smaller exchange. MPZZF’s domicile is Norway, and withholding taxes may apply. The Tax Authority has more information.

Valuation

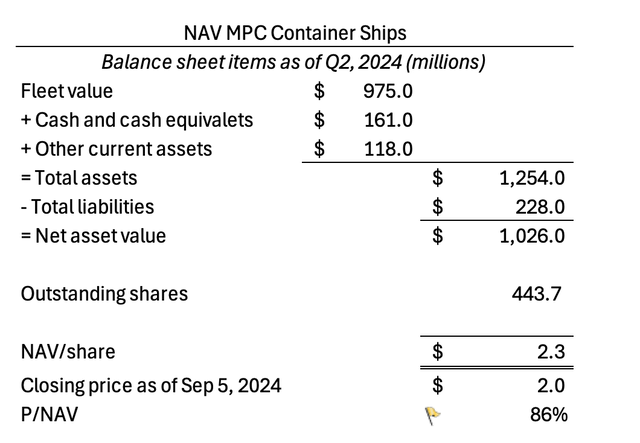

Using its last published sales and acquisitions, I estimate that the value of MPZZF’s fleet is $975 million. That would give the following NAV calculation as of Q2:

NAV calculation as of Q2 (Author’s calculations)

This calculation could indicate that MPZZF is trading slightly below NAV.

Market Outlook

Ton-Mile Demand: The Red Sea Could Be a Challenge for Years

The diversion away from the shorter Red Sea route is a fundamental driver of ton-mile demand due to the much longer route, represented by the alternative around the Cape of Good Hope.

The Houthis have expressed support for Palestine in the Israel/Gaza conflict, and some say the Houthis are an Iranian proxy. This article argues that the motivations of the Houthi extend far beyond ideological alignment with Iran and Palestine and could be based on a belief that the attacks will yield benefits.

TradeWinds spoke to a think tank that warned that “these attacks have begun to acquire their own dynamics as time goes by” and said a ceasefire in the Israel/Gaza conflict is no guarantee that the Red Sea will be safe.

The attacks have shown that an actor can pose a significant threat with relative ease and little investment. Efforts by the powerful navies of the U.S. and the U.K. have proven inadequate in staving off that threat, instead resulting in tit-for-tat exchanges with the Houthis.

While a ceasefire is probably the best chance to ensure that shipping can return to the Red Sea (and thereby significantly shorten routes), I don’t think that is likely in the near to medium term.

De-Globalization: More Ports, More Routes—More Feeders

The FT writes a series on “the causes and consequences of this new era of greater state intervention in the economy,” in a world where “globalisation [is] on the retreat.” This article discusses how China responds to U.S. and U.K. product tariffs by investing in “connector countries,” such as Vietnam, Mexico, Hungary, Ireland, and Singapore. The purpose is to avoid the tariffs by shifting their supply chains to countries unaffected by tariffs. This is just one example of how the world gradually moves away from China as the number one manufacturing hub.

Liner Business Models: The Maersk-Hapag Gemini Cooperation

As the big liners are MPZZF’s and its peers’ most important customers, one must look at what goes on in that space. From February 2025, Maersk and Hapag-Lloyd will run their businesses as the Gemini Cooperation. This newly formed alliance aims to run a hub-and-spoke network with “industry-leading reliability.” According to MPZZF CEO Constantin Baack, who spoke about this alliance in its latest earnings call, it will benefit a feeder tonnage provider such as itself.

An analysis on Seatrade Maritime recently looked at direct port calls vs. the hub and spoke approach. Its findings suggest that

that hub-and-spoke models are not prevailing; instead, there is a shift towards direct services, as they often utilise smaller vessels offering a more resilient option compared to the larger vessels typically associated with hub-and-spoke networks.

This shift toward smaller ships benefits MPZZF by focusing on smaller segments.

From MPZZF’s point of view, the new alliance and the shift to direct services diversify its customer base. Two of its most important customers, Maersk and Hapag, have entered into a new operating model, while others, such as MSC, continue as before. Regardless of the success or failure of the Gemini Cooperation—it has set very ambitious reliability targets of 90%—MPZZF will have customers using different operating models.

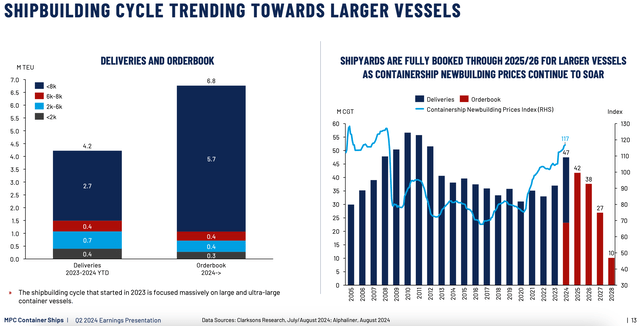

Orderbook Tilted Toward Larger Ships—Feeders Aging

MPZZF presents two slides in its earnings presentation that explain this issue well. Out of 6.8 million TEU in the order book, just 10 percent are vessels smaller than 6,000 TEU:

Order book composition (Q2 presentation)

At the ongoing SMM in Hamburg, newbuilding prices were discussed in a session hosted by TradeWinds. MPZZF’s CEO commented that they have an investment case for retrofits on vessels as small as 1,700 TEU. This shows how prices on newbuilds and long delivery times affect orders.

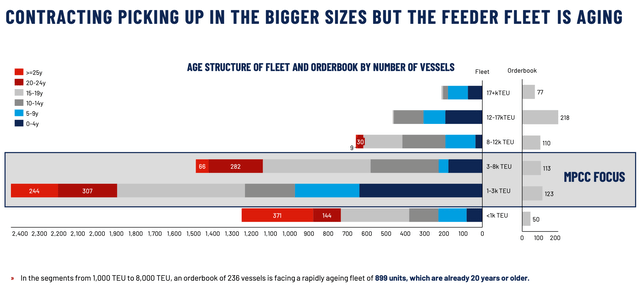

Turning our attention to the age of ships on the water, we note that MPZZF’s segments are characterized by aging ships. Almost 900 ships on the water are twenty years or older, but only 236 vessels are in the order book in those segments.

This point is explored further in this July 1 article on Seatrade Maritime.

These old vessels will become scrapping candidates as emissions requirements will gradually become stricter in the next few years, and customers seek to decarbonize their supply chains. This gives MPZZF an advantage in the future.

Fleet age structure (Q2 earnings presentation)

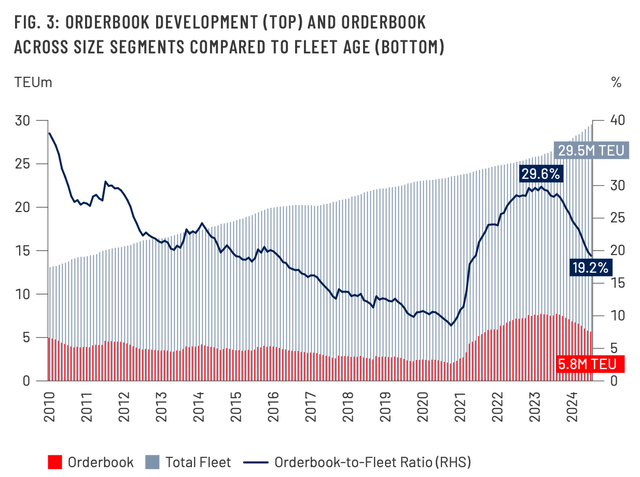

Finally, the overall order book has also shrunk relative to tonnage on the water in the past year. From a record 29.6% in 2024, the ratio has decreased to 19.2%. From MPZZF’s earnings report:

Orderbook-to-fleet ratio (Q2 earnings report, p. 13)

Conclusion

This article has reviewed container feeder tonnage provider MPC Container Ships and considered its feasibility as an investment for exposure to that segment. It found that MPC Container’s strong balance sheet and earnings visibility provide some insulation from the volatile market in which it operates. It appears to be trading slightly below NAV currently. However, due to the volatile nature of shipping, investors should be prepared for swings in value.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here