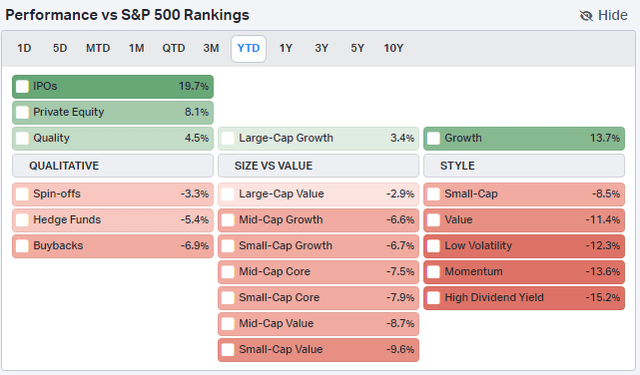

It has been a lousy year for income investors relative to the growth theme. The high-dividend factor is down about 15% on the year (compared to the S&P 500’s total return). Still, many strategists expect small caps, value, and quality companies that are growing their dividend to return to relative favor in 2024. I am generally in that camp given where valuations are, and as the turn of the year often leads to a rethinking of asset allocation stances.

I have a buy rating on MPLX LP (NYSE:MPLX). I see units modestly undervalued today, and despite an EPS miss, the MLP has a strong execution history and the ability to increase its payout over the ensuing quarters.

High Dividend Equities Struggle Relative to Growth in 2023

Koyfin Charts

According to the company website, MPLX is a diversified, large-cap master limited partnership (MLP) formed by Marathon Petroleum Corporation (MPC) that owns and operates midstream energy infrastructure and logistics assets and provides fuels distribution services. It also owns crude oil and natural gas gathering systems and pipelines as well as natural gas and natural gas liquids (NGL) processing and fractionation facilities in key U.S. supply basins. It operates in two segments, Logistics and Storage (L&S), and Gathering and Processing (G&P).

The Ohio-based $36.1 billion market cap Oil and Gas Storage and Transportation industry company within the Energy sector trades at a low 9.7 forward non-GAAP price-to-earnings ratio and pays a high 9.4% forward dividend yield as of December 15, 2023. Ahead of earnings due out next month, units trade with a low 10% implied volatility percentage while short interest on the stock is material at 3.0%.

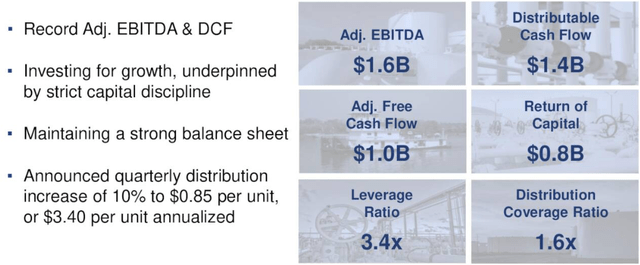

Back in October, MPLX reported a decent quarter, but it missed on the bottom line. Q3 GAAP EPS of $0.89 fell short of the Wall Street consensus expectation of $0.93 while revenue of $2.9 billion was a steep 14% decline from year-ago levels, though that figure topped estimates. Adjusted EBITDA verified at a record $1.596 billion and distributable cash flow also notched a high-water mark. Its G&P segment performed well in the previous quarter, but the L&S segment outperformed, driven by strong tariff rates.

NGL price declines continue to ding the G&P slice, though ongoing investments into the Permian region should lead to stronger cash flow in the years ahead. As such, the 10% increase in the partnership’s distribution could be a sign of more unitholder-friendly payouts to come should pipeline expansion projects turn more profitable and capital allocation decisions by the management continue to be well executed.

Q3 Business Update

MPLX IR

Key risks include weakness in the macroeconomic picture as well as weaker oil and gas demand domestically, potentially hurting its dividend payout policy.

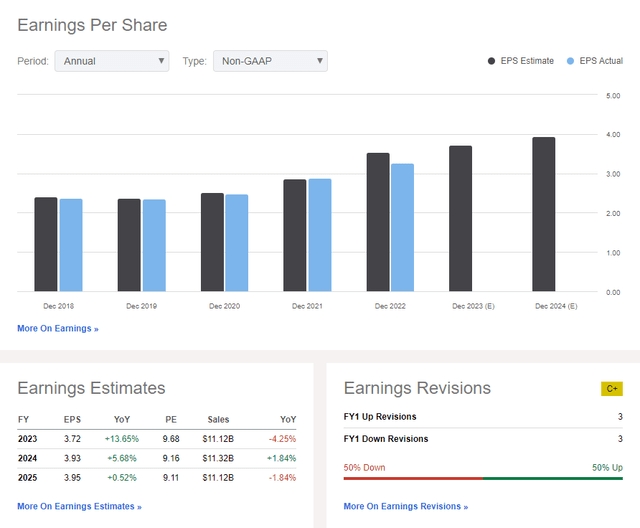

On valuation, the consensus analyst opinion shows that EPS is expected to rise about 14% this year with out-year EPS growth decelerating through 2025. The top line is forecast to hover near $11 billion. Dividends, meanwhile, are expected to rise over the coming quarters – the management team has said that the primary method by which to return cash to unitholders is through dividend payments.

The firm has balance sheet flexibility to continue to increase the unit payout rate by roughly 10% annually given that leverage is near 3.4x, per BofA, and distribution coverage is adequate around 1.6x. Given that cash on the balance sheet is about $960 million as of the end of Q3, I would expect the yield to potentially grow over the coming quarters.

MPLX: Earnings & Revenue Outlook

Seeking Alpha

If we assume $3.80 of normalized EPS over the next 12 months and apply the stock’s 5-year average non-GAAP forward price-to-earnings ratio of 10.4, then units should price near $39.50. Amid higher interest rates today, even if we discount that by 10%, the stock is still near fair value, and considering the high dividend rate, it’s worth owning for yield-focused investors, though MPLX is somewhat expensive on a price-to-book basis today.

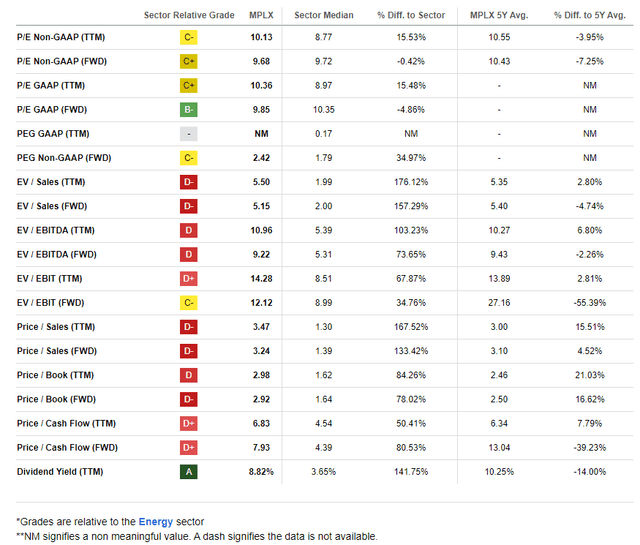

MPLX: Mixed Valuation Metrics, High Yield

Seeking Alpha

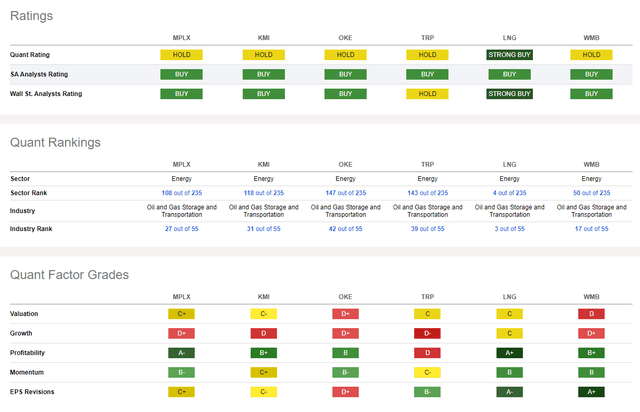

Compared to its peers, MPLX features a lukewarm valuation, but earnings and sales multiples across the Oil & Gas Transportation space are mixed. What’s more, top and bottom-line growth is often not the primary reason for owning a high-payout MLP, so weak growth metrics do not concern me as they would for companies in other sectors. What’s impressive is MPLX’s robust profitability metrics while its consistently high unit-price momentum is just about the best in its industry. Finally, EPS revisions have been mixed lately following the Q3 bottom-line miss.

Competitor Analysis

Seeking Alpha

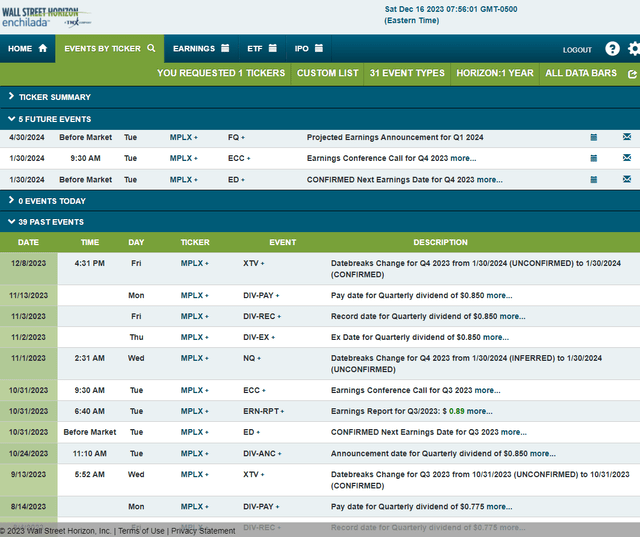

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q4 2023 earnings date of Tuesday, January 30 BMO with a conference call later that morning. You can listen live here. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

Wall Street Horizon

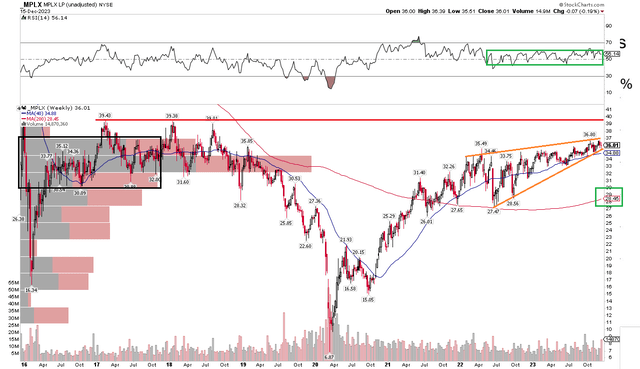

The Technical Take

MPLX has been a dividend machine over recent years. Making the ride easy on unitholders is that the stock has been steadily rising for the last handful of quarters. Notice in the chart below that units have increased markedly from the bottom in early 2020. The weekly view illustrates that the bulls are in control given that the 40-week moving average, comparable to the 200-day moving average, is positively sloped while the 200-week moving average is also trending up. Moreover, the RSI momentum gauge at the top of the graph shows that modestly positive momentum persists.

Also take a look at where key resistance is seen. The $39 to $40 zone was met with selling pressure on a few occasions from early 2017 through mid-2018, and we are just now encountering that spot again. What’s different this time is that the chart reveals a potentially bearish pattern – a rising wedge. A series of higher highs and higher lows is intuitively bullish, but technicians consider this consolidation as a negative signal. So long as MPLX is above $33 – the low from the summer – then units look fine to me technically. Additionally, a breakout above $40 would support the case for a significant appreciation of units. For now, with a high amount of volume by price in the $28 to $39 area, there is a fair amount of traffic for both the bulls and the bears to navigate.

Overall, the chart is neutral with a long-term uptrend soon approaching noted resistance while momentum remains healthy.

MPLX: Strong Momentum, Rising Wedge with Price Nearing Long-Term Resistance

Stockcharts.com

The Bottom Line

I have a buy rating on MPLX. I see units modestly undervalued, but with a high and sustainable distribution rate, I see units as a solid vehicle for delivering a dividend stream.

Read the full article here