‘Compounder’ stocks are an interesting breed for a couple of reasons.

– First, people have such a wide variety of ways that they like to define and screen for them, and

– Second, investing in the right ones can make you a LOT of money over a long-term investing horizon.

Many have a view that finding a compounder is a game of ‘inputs’ – in that, a business that is in the right market, with the right management, and with a highly profitable business model will likely make you a strong return over the long term. We don’t have anything against this approach, and it’s sure to find you some great companies.

However, in our book, we care about results.

A strong business doesn’t show itself through its narratives, management talking points, or auxiliary data – a strong business shows itself through incredible financial results.

People can spin all kinds of stories, but at the end of the day, investing is a game of inputs and outputs. Does the ‘box’ you’re putting your money in actually deliver? Does the series of business decisions and systems currently in place outperform other cohesions of systems and capital?

Today, we’re going to be spending some time today talking about MSCI Inc. (NYSE:MSCI), a business that we think stands up to our definition of a true compounder. Not only does the company boast incredible results, but it’s currently trading for a steal, presenting an opportunity.

Without further ado, let’s dive in and explain why we’re so bullish on this great company.

What Makes A Compounder?

In order to talk more about what makes MSCI so special, it’s important that we first lay out what we mean when we’re talking about a ‘compounder’.

In short, we look for three things that tell us whether or not a company might be able to grow an investment at a higher-than-average rate for a longer-than-average period of time.

First, we look for growing top line results. In the words of Bob Dylan, “That he not busy being born is busy dying“.

In other words, is the company constantly improving? Constantly growing? Since revenue is the lifeblood of a company, if it’s not growing, at least at the rate of inflation & GDP growth, then there might be a problem.

Second, we look for growing bottom line results.

We don’t need to see margin expansion, as sometimes the best businesses are simply constrained by the market they are in. However, it’s important that bottom line results are growing apace with revenues, otherwise there might be a problem with market competition, scaling, or a million other things.

–

Between these two key data points, we’re looking for companies that are increasing the scale of the business, as well as the utility / reward to investors. These two points serve as a proxy for ‘demand‘ for shares.

Finally, we look for a shrinking diluted share count.

If management is actively retiring company shares from the open market, it signals a few things- that a company is in a strong financial position, and its leaders understand the importance of rewarding shareholders over the long term.

This is the ‘supply‘ side.

For us, the whole package needs to be aligned to consider something a ‘compounder’ – increasing demand for shares, and a decreasing supply of them. In most markets, this imbalance should drive prices up.

Why Is MSCI A Compounder?

But why talk about MSCI?

In short, because this great company meets our criterion perfectly.

At a base level, in case you’re new to MSCI, the company provides data and index products to mostly institutional investors.

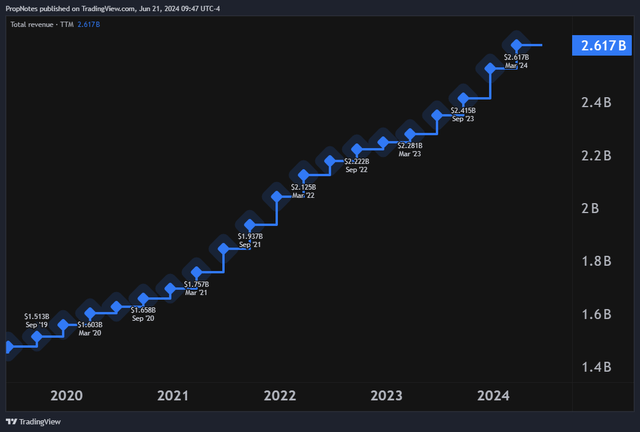

Over the last 5 years (and beyond that), MSCI has grown revenues like clockwork, at a rapid pace over that period:

TradingView

Since 2019, TTM sales have increased from $1.47 billion to $2.61 billion, an impressive CAGR of 12.1%, which is very high for any publicly listed company.

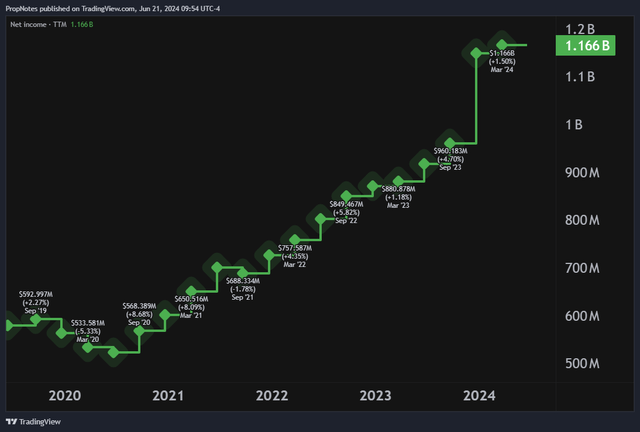

At the same time, TTM net income has grown from ~$550 million to more than $1.1 billion, a clean double in only five years:

TradingView

This CAGR growth rate is around 15%, which is even more impressive than the top line expansion.

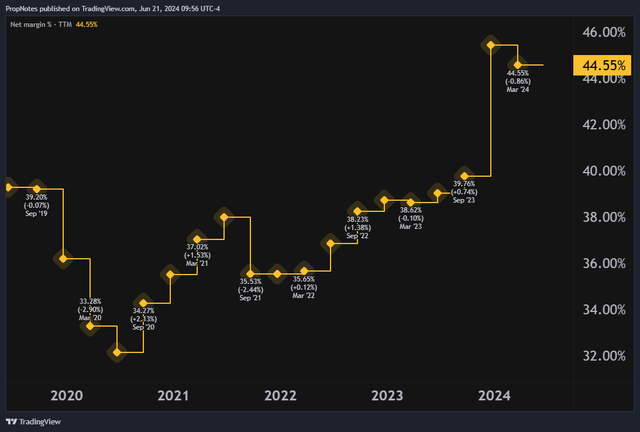

This means that profits are not only dropping to the bottom line, but that the company is getting more efficient at cash conversion. As you can see below, margins have been gently sloping upward over the last 5 years from the low 30% range to above 40%, which should excite investors tremendously:

TradingView

Put together, it’s clear that management has done a good job of growing demand for MSCI shares.

But it’s not just the demand side, the ‘supply’ side for shares is also headed in the right direction.

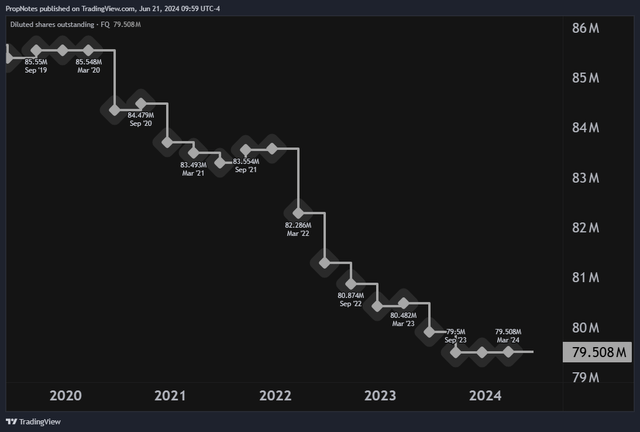

Since 2019, the diluted share count for MSCI has fallen by 7%, from 85 million to 79 million:

TradingView

And, while this isn’t as impressive as the top line growth, it does show that management is focused on returns to shareholders, or, at the very least, avoiding dilution.

When you add it all up, MSCI’s track record is nothing short of fantastic from a financial POV. It has the ingredients necessary to potential compound an investment’s capital over time.

Why Now?

But why now? Why is now the right time to buy into this company?

In short, because the company is trading at a ‘good’ price.

Over time, there are two variables to consider when investing into a stock – the results, and the valuation. As we’ve discussed, the results are there, is the valuation?

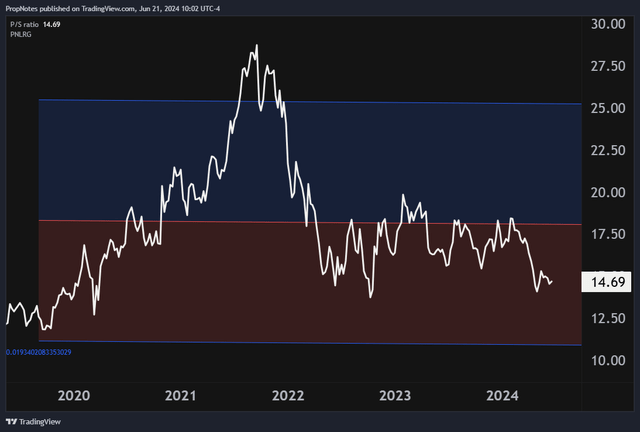

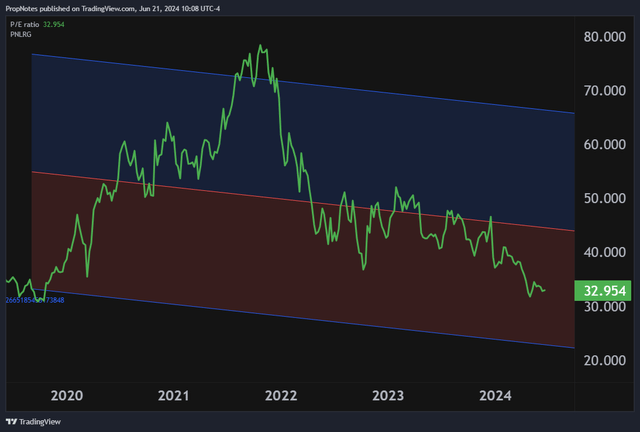

Right now, MSCI is trading at 14x sales(!), and roughly 33x net income. While these numbers sound very high, this is a similar situation to Visa (V) and Mastercard (MA), where the sales multiple is so elevated only because the company’s margins are so incredibly strong.

When viewed against the company’s historical multiple, MSCI, right now, appears attractively priced, hovering on the lower end of average over the last 5 years:

TradingView

You can see this range with the blue and red channels which represent the standard deviation of the linear regression. Right now, MSCI shares are trading at the most attractive multiple in a long time.

The net income multiple also appears to be trading in roughly the same area, near 5 year lows:

TradingView

Ultimately, we expect these valuations to expand somewhat, or at least mean revert, over time.

Remember, buying ‘low’ is the key, and these charts and multiples show that the multiple is well priced for what we’re getting.

A good price for a good value.

Risks

There are a few risks to be aware of here.

MSCI’s business is strong, but bad moves by management could weaken competitive advantages. If other index / data companies begin to capture market share, then MSCI may need to invest at a higher-than-average rate in sales, product, and marketing to reclaim the throne. This could dent results and hurt returns to shareholders.

That said, almost all of the company’s indices have money trading behind them when it comes to fund complexion, which makes MSCI’s moat quite strong.

Additionally, the multiple could compress more, if growth or profitability comes under fire. While we think the present multiple represents a solid opportunity, but things may change in the future that cause the company’s admittedly expensive nominal valuation to come back down, closer to being in line with the S&P 500. That could cause losses to investors.

Summary

All in all though, it’s hard to see MSCI as anything other than a strong value at a good price. Results are growing, the share count is shrinking, and the multiple appears reasonable. What else do you need?

Pounce, before this deal goes away.

We rate MSCI a ‘Strong Buy’.

Cheers!

Read the full article here