Market overview

Municipal bonds maintained their seasonal strength and extended gains for the second consecutive month in July. Interest rates rose amid heightened volatility as economic data exceeded expectations, and the Federal Reserve resumed its tightening cycle and communicated a commitment to data dependence. Favorable supply-and-demand dynamics and the more stable nature of the asset class prompted outperformance versus Treasuries. The S&P Municipal Bond Index returned 0.25%, bringing the year-to-date total return to 2.78%. Triple-B rated credits and the 15-year part of the yield curve performed best.

Issuance totaled just $27 billion, 17% below the five-year average, bringing the year-to-date total to $198 billion, down 12% year over year. Reinvestment income from maturities, calls, and coupons outpaced issuance by nearly $16 billion and created a favorable net-negative supply environment. As a result, deals were oversubscribed by 5.2 times on average, well above the year-to-date average of just 4.0 times. Bid-wanted activity also underwhelmed, falling over $300 million per day, month over month, as bank portfolio liquidations ceased in late June. Concurrently, demand for the asset class has continued to strengthen. Mutual funds experienced increasingly positive fund flows, while professional retail accounts were inundated with new orders.

We believe that rich valuations and waning seasonal technicals warrant a bit more caution in the weeks ahead. Performance tends to soften in August as the market prepares for increased supply in the autumn. However, we would view any prolonged weakness as an opportunity to add duration and lock in attractive, late-cycle yields.

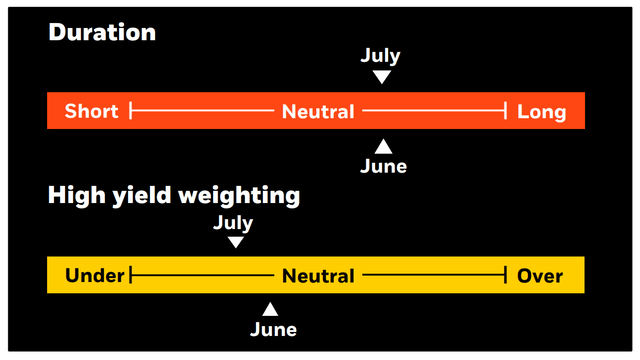

Strategy insights

We maintain a neutral-duration posture overall. We prefer an up-in-quality bias and have become increasingly selective in non-investment grade. We strongly advocate a barbell yield curve strategy, pairing front-end exposure with an increased allocation to the 15-20-year part of the curve.

Overweight

- Essential-service revenue bonds.

- Select highest quality state and local issuers with broadest tax support.

- Flagship universities.

- Select issuers in the high yield space.

Underweight

- Speculative projects with weak sponsorship, unproven technology, or unsound feasibility studies.

- Senior living and long-term care facilities in saturated markets.

- Lower rated private universities.

- Stand-alone and rural health providers.

Credit headlines

On August 1st, Fitch downgraded the United States from AAA to AA+, reflecting the expected fiscal deterioration in coming years, the growing debt burden, and the erosion of sound governance. Fitch warned that the government deficit will rise to 6.6% of GDP in 2024, driven by weak GDP, a higher interest burden, and wide state and local deficits of 1.2% of GDP. They also highlighted that the interest-to-revenue ratio for the U.S. will soar to 10% by 2025, which is 10x greater than the AAA-rated median.

We expect the municipal market will react as it did in 2011, following S&P’s downgrade of the U.S., when most bonds were unaffected. A small subset of munis with creditworthiness linked to the U.S. Treasury could be subject to negative rating action, such as pre-refunded bonds, housing bonds with federal guarantees, bonds backed by federal leases, and the bonds of state and local governments that are highly dependent on federal procurement contracts and/or direct federal employment. Still, those AAA-rated entities with a dominant proportion of own-source revenue will likely retain their ratings.

Unlike the federal government, U.S. states are in a much stronger position to deal with declining revenues. Rainy day funds are well above historical levels; pension plans have benefited from additional funding; expenditures have now aligned with pre-COVID levels; and debt service is at 50-year lows. Also, unlike the federal government, 46 states have balanced budget requirements prohibiting states from spending more than annually available revenues. Balanced-budget rules vary but typically include constitutional restrictions, limited or no deficit carryovers, and both legislature passage and the governor’s signature. Similar provisions are in place for local governments and municipal authorities. Despite increased doubts surrounding U.S. credit strength, states and local governments will remain among the highest-rated bonds within the fixed income asset class

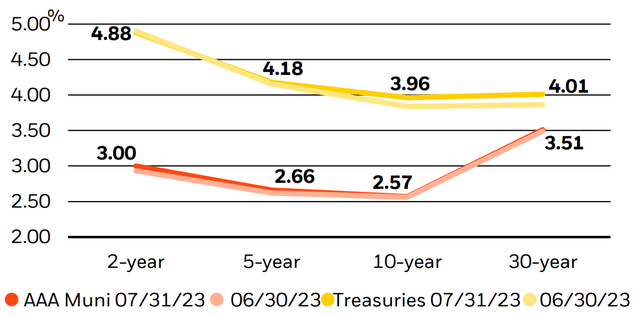

Municipal and Treasury yield movements

BlackRock, Bloomberg

Municipal performance

| July ’23 | YTD | |

| S&P Municipal Bond Index | 0.25% | 2.78% |

| Long maturities (20+ yrs.) | 0.26% | 4.87% |

| Intermediate maturities (3-15 yrs.) | 0.25% | 2.10% |

| Short maturities (6 mos.-4 yrs.) | 0.19% | 1.18% |

| High yield | 0.35% | 5.07% |

| High yield (ex-Puerto Rico) | 0.35% | 4.49% |

| General obligation (GO) bonds | 0.21% | 2.39% |

| California | 0.27% | 2.65% |

| New Jersey | 0.36% | 3.51% |

| New York | 0.24% | 3.47% |

| Pennsylvania | 0.29% | 2.69% |

| Puerto Rico | 0.32% | 8.29% |

Sources: S&P Indexes.

Investment involves risk. The two main risks related to fixed income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. There may be less information available on the financial condition of issuers of municipal securities than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. A portion of the income from tax-exempt bonds may be taxable. Some investors may be subject to Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. Past performance is no guarantee of future results.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of August 8, 2023, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to pass. Any investments named within this material may not necessarily be held in any accounts managed by BlackRock. Reliance upon information in this material is at the sole discretion of the reader.

©2023 BlackRock, Inc or its affiliates. All Rights Reserved. BlackRock is a trademark of BlackRock, Inc or its affiliates. All other trademarks are those of their respective owners.

Prepared by BlackRock Investments, LLC, member FINRA.

Not FDIC Insured • May Lose Value • No Bank Guarantee

This post originally appeared on the iShares Market Insights.

Read the full article here