Giglio Porto

The Pearl of the Tuscan Archipelago

Giglio Island is a granite rock about 21 square kilometers in size that emerges from the Tyrrhenian Sea off the coast of the Tuscan Maremma. Bathed by crystal clear emerald waters, it has a picturesque landing point (Giglio Porto), a medieval settlement on the top of the island (Giglio Castello) and a tiny seaside resort on the opposite side (Giglio Campese). A single paved road connects the three resorts, inhabited year-round by just over a thousand people.

The anxiety about progress and development that besieges the most renowned tourist places seems absent from the horizons of islanders, who still live at a slow, sustainable, human-scale pace. Adults stop on benches to talk, children play in the street or on the quayside, and cats snooze peacefully in the shade. Out of season, the harbor comes alive only during the times when the ferry arrives from the mainland and the few tourists get off. Then the ferry leaves, the quiet recomposes itself and life resumes its peaceful flow.

A Heroic Viticulture

Behold the sun’s heat, which becometh wine, / Joined to the juice that from the vine distils”. (Dante, Divine Comedy, Purgatory, Canto XXV, translated by Henry Wadsworth Longfellow, Boston 1871)

In this little paradise, a heroic viticulture, dating back as far as the Etruscans, but which fell into disuse during the last century, has been revived for the past decade or so. Here, in fact, vines have always been cultivated in patches of land overlooking the sea, reachable only on foot, with enormous effort and dedication. The resulting wine, made from Ansonaco grapes, is a true nectar of the gods, produced sometimes in a few hundred bottles, almost exclusively for local consumption.

The vines, which make their way into the ravines of the granite rock, each give one or two clusters, the grapes of which become as precious as gold. Nothing is wasted, but everything is lovingly cultivated, harvested and processed to produce a unique wine that tastes of iodine, saltiness, granite, sun, wind and Mediterranean scrub. In mid-June, I spent a few days on the island, and as I admired the bunches of grapes ripening on the small plants, I imagined how few drops of wine would flow from each one… and how many it takes to fill a bottle!

As for the dividends in my portfolio, each share carries its own drop, which combined with the others will fill a bottle of returns. Each individual share: studied, weighed, painstakingly purchased from a difficult market with savings and hardship, like the Ansonaco vines of Giglio, plucked from the granite of the island.

Harvesting Dividends

Thinking about all this made me want to retrace my very first steps in this direction, when I began my personal “harvest.” So, as soon as I got home, I went to my bank’s website and looked up the accounting of my first dividends, which is fortunately still archived and available. During 2013, I had set out to Google sites that talked about high-dividend U.S. securities. I thus began to peruse their long lists of stocks unknown to me, looking for what I thought might be right for my savings.

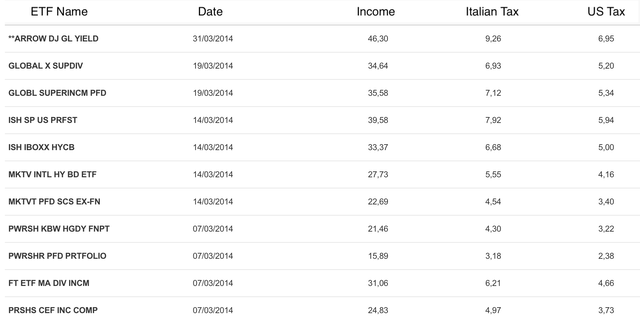

In early 2014, I began to peep into the U.S. market by exploring the world of ETFs, and in March arrived the first dividends, as shown in the below image, in which everything is calculated in euros:

2014 Dividends (Seeking Alpha)

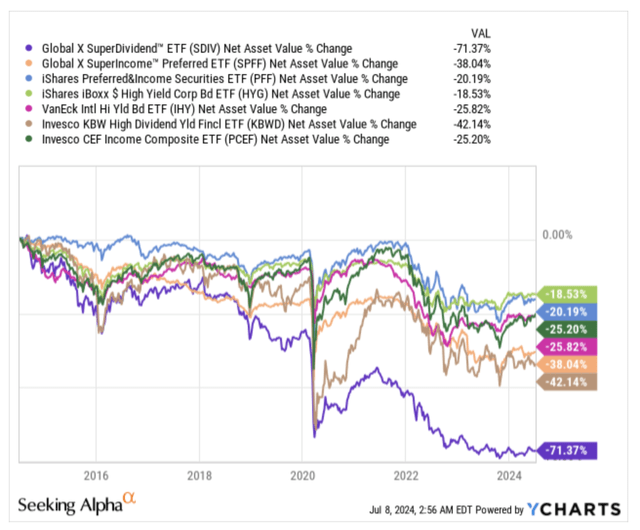

In my last article, I recounted my beginnings in the world of CEFs. CEFs, however, were a later discovery for me than ETFs, which occurred toward the end of 2014. Up to that time, the securities I had purchased had all been ETFs, some of which no longer exist today, while others have changed names or management houses. Of those that remain in existence and that I hope I have been able to identify correctly, I report below their NAV performance, indicating first the correspondence between the Italian abbreviations and the full definition of each security, according to the order in which they appear in my bank’s statement:

- GLOBAL X SUPDIV = Global X SuperDividend™ ETF (SDIV).

- GLOBL SUPERINCM PFD = Global X SuperIncome™ Preferred ETF (SPFF).

- ISH SP US PRFST = iShares Preferred and Income Securities ETF (PFF).

- ISH IBOXX HYCB = iShares iBoxx $ High Yield Corporate Bond ETF (HYG).

- MKTV INTL HY BD ETF = VanEck International High Yield Bond ETF (IHY).

- PWRSH KBW HGDY FNPT = Invesco KBW High Dividend Yield Financial ETF (KBWD).

- PRSHS CEF INC COMP = Invesco CEF Income Composite ETF (PCEF).

2014 ETFs (Seeking Alpha)

As can be seen, between then and now, all of these ETFs have lost value (some have even collapsed, as KBWD’s -42% and SDIV’s -71% attest), proving once again that creating an income portfolio is a negative art. First, one must learn to avoid losing stocks, and only then begin to plan for the future: invert, always invert, as Charlie Munger used to admonish. As far as I am concerned, this is a lesson I have learned along the way but have not yet been able to fully apply.

Ten Years Later

Be that as it may, between then and now, my portfolio has taken other paths, receiving decent slaps but also having its moments of glory. As you may know, it currently shows up with 28 securities (19 CEFs, 5 ETFs, 3 BDCs, 1 ETN) divided into three different portfolios:

Cupolone Income Portfolio (named after Brunelleschi’s Florentine dome) consists of seventeen CEFs with monthly distributions:

- BlackRock Science and Technology Trust (BST).

- Calamos Dynamic Convertible and Income Fund (CCD).

- Calamos Global Total Return Fund (CGO).

- Eaton Vance Enhanced Equity Income Fund II (EOS).

- Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund (ETO).

- Eaton Vance Tax-Advantaged Dividend Income Fund (EVT).

- Guggenheim Strategic Opportunities Fund (GOF).

- John Hancock Tax-Advantaged Dividend Income Fund (HTD).

- PIMCO Corporate & Income Strategy Fund (PCN).

- PIMCO Dynamic Income Fund (PDI).

- John Hancock Premium Dividend Fund (PDT).

- PIMCO Corporate and Income Opportunity Fund (PTY).

- Cohen & Steers Quality Income Realty Fund (RQI).

- Special Opportunities Fund (SPE).

- Cohen & Steers Infrastructure Fund (UTF).

- Reaves Utility Income Trust (UTG).

- XAI Octagon Floating Rate & Alternative Income Trust (XFLT).

Giotto Income Portfolio (named after the fourteenth-century Florentine painter and architect) includes five ETFs and one ETN with monthly distributions that adopt a covered-call strategy:

- JPMorgan Equity Premium Income ETF (JEPI).

- JPMorgan Nasdaq Equity Premium Income ETF (JEPQ).

- Global X NASDAQ 100 Covered Call ETF (QYLD).

- Global X Russell 2000 Covered Call ETF (RYLD).

- Credit Suisse X-Links Crude Oil Shares Covered Call ETNs (USOI).

- Global X S&P 500® Covered Call ETF (XYLD).

Masaccio Income Portfolio (named after the founder of Renaissance painting) contains three BDCs and two CEFs with quarterly distributions:

- Ares Capital (ARCC).

- Crescent Capital BDC, Inc. (CCAP).

- Fidus Investment (FDUS).

- Barings Corporate Investors (MCI).

- Royce Small-Cap Trust (RVT).

From the small drops of wealth from that first ETF portfolio to the current dividends/distributions, the trek has been a long one, with a multitude of stocks come and gone. But those remaining have ensured a steady flow of money that only in a few cases has been reduced by temporary cuts, later patched up, as in the case of EOS, ETO, and EVT.

The only two that cut the distribution without yet restoring it were CGO (September 2022) and PDT (June 2023). SPE has a variable distribution based on NAV and recalculated from year to year. The ETFs all have variable dividends, as do the BDCs and the two CEFs with quarterly distributions in the Masaccio portfolio.

But let’s look in detail at the dividend history of the past five years for each security in my current portfolio, and from launch to present for those born after 2019. The spikes that appear in the charts represent special year-end dividends/distributions.

Cupolone Income Portfolio

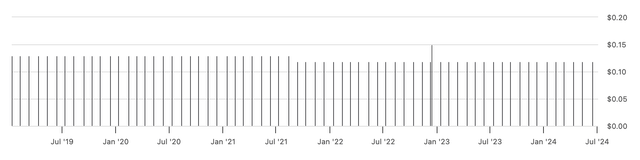

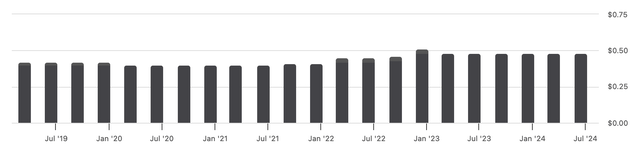

BlackRock Science and Technology Trust (BST)

Distribution rate at current market price: 7.81%.

BST (Seeking Alpha)

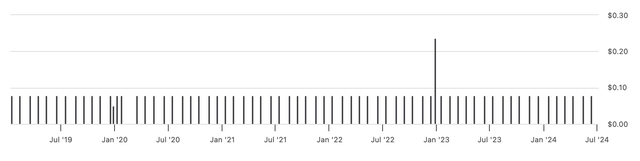

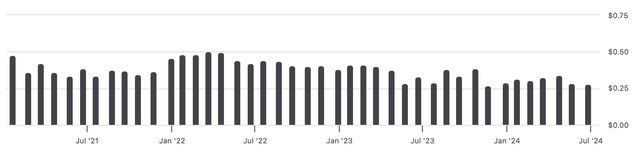

Calamos Dynamic Convertible and Income Fund (CCD)

Distribution rate at current market price: 10.01%.

CCD (Seeking Alpha)

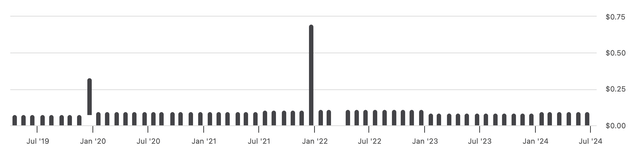

Calamos Global Total Return Fund (CGO)

Distribution rate at current market price: 8.39%.

CGO (Seeking Alpha)

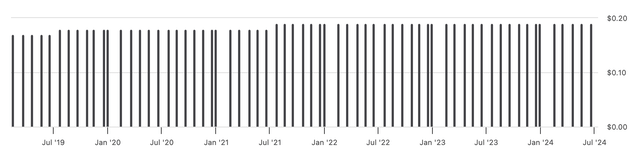

Eaton Vance Enhanced Equity Income Fund II (EOS)

Distribution rate at current market price: 8.16%.

EOS (Seeking Alpha)

Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund (ETO)

Distribution rate at current market price: 8.03%.

ETO (Seeking Alpha)

Eaton Vance Tax-Advantaged Dividend Income Fund (EVT)

Distribution rate at current market price: 8.42%.

EVT (Seeking Alpha)

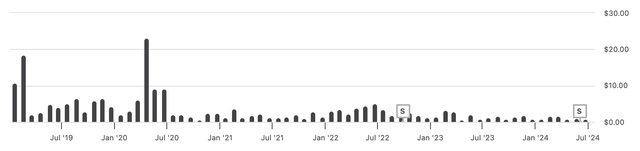

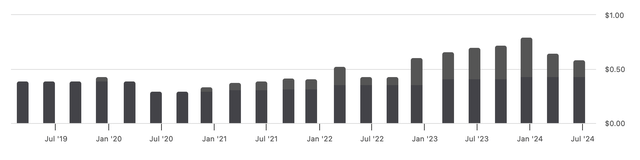

Guggenheim Strategic Opportunities Fund (GOF)

Distribution rate at current market price: 14.42%.

GOF (Seeking Alpha)

John Hancock Tax-Advantaged Dividend Income Fund (HTD)

Distribution rate at current market price: 8.14%.

HTD (Seeking Alpha)

PIMCO Corporate & Income Strategy Fund (PCN)

Distribution rate at current market price: 10.10%.

PCN (Seeking Alpha)

PIMCO Dynamic Income Fund (PDI)

Distribution rate at current market price: 13.88%.

PDI (Seeking Alpha)

John Hancock Premium Dividend Fund (PDT)

Distribution rate at current market price: 8.43%.

PDT (Seeking Alpha)

PIMCO Corporate and Income Opportunity Fund (PTY)

Distribution rate at current market price: 9.86%.

PTY (Seeking Alpha)

Cohen & Steers Quality Income Realty Fund (RQI)

Distribution rate at current market price: 8.24%.

RQI (Seeking Alpha)

Special Opportunities Fund (SPE)

Distribution rate at current market price: 8.51%.

SPE (Seeking Alpha)

Cohen & Steers Infrastructure Fund (UTF)

Distribution rate at current market price: 8.14%.

UTF (Seeking Alpha)

Reaves Utility Income Trust (UTG)

Distribution rate at current market price: 8.31%.

UTG (Seeking Alpha)

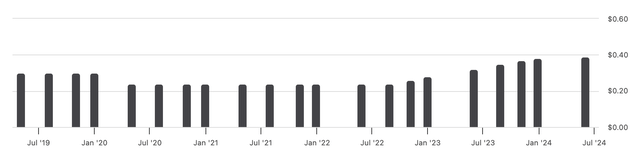

XAI Octagon Floating Rate & Alternative Income Trust (XFLT)

Distribution rate at current market price: 14.39%.

XFLT (Seeking Alpha)

Giotto Income Portfolio

With regard to the return of ETFs, the 12-Month Yield is given, i.e., “the sum of an investment’s total trailing 12-month interest and dividend payments divided by the last month’s ending share price (NAV) plus any capital gains distributed over the same period.” (Morningstar)

JPMorgan Equity Premium Income ETF (JEPI)

12-Month Yield: 7.34%.

JEPI (Seeking Alpha)

JPMorgan Nasdaq Equity Premium Income ETF (JEPQ)

12-Month Yield: 8.77%.

JEPQ (Seeking Alpha)

Global X NASDAQ 100 Covered Call ETF (QYLD)

12-Month Yield: 11.64%.

QYLD (Seeking Alpha)

Global X Russell 2000 Covered Call ETF (RYLD)

12-Month Yield: 12.52%.

RYLD (Seeking Alpha)

Credit Suisse X-Links Crude Oil Shares Covered Call ETNs (USOI)

12-Month Yield: 19.37%.

USOI (Seeking Alpha)

Global X S&P 500® Covered Call ETF (XYLD)

12-Month Yield: 9.35%.

XYLD (Seeking Alpha)

Note: Only the last three years were reported for XYLD.

Masaccio Income Portfolio

With regard to the return of the 3 BDCs, the Forward Dividend Yield is given, i.e., “an estimated annual yield calculated by taking the most recent regular dividend payment for a stock, applied across the regular dividend payment for a year, and dividing it by the current price.” (Morningstar)

Ares Capital (ARCC)

Forward Dividend Yield: 9.10%.

ARCC (Seeking Alpha)

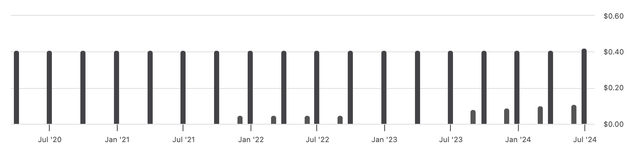

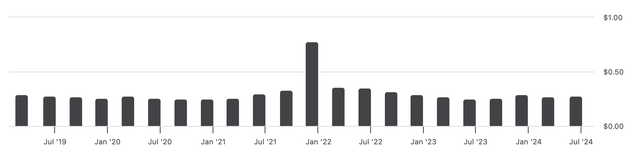

Crescent Capital BDC, Inc. (CCAP)

Forward Dividend Yield: 9.07% (the small bars are special dividends.)

CCAP (Seeking Alpha)

Fidus Investment (FDUS)

Forward Dividend Yield: 13.04%.

FDUS (Seeking Alpha)

Barings Corporate Investors (MCI)

Distribution rate at current market price: 8.34%.

MCI (Seeking Alpha)

Royce Small-Cap Trust (RVT)

Distribution rate at current market price: 7.82%.

RVT (Seeking Alpha)

Future Resolutions

As can be appreciated, the regularity of dividends/distributions over the past five years has been consistent for all stocks that were part of my portfolio.

Despite this, and while I am grateful to the managers of the securities in my portfolio for consistent returns, I think I will close some positions currently in the red the moment they should break even again. These include CGO, which I probably bought at too high a price and whose volatility at one point caused me to take a capital loss close to 40 percent: it’s a microcap, no wonder, but I would prefer more solidity.

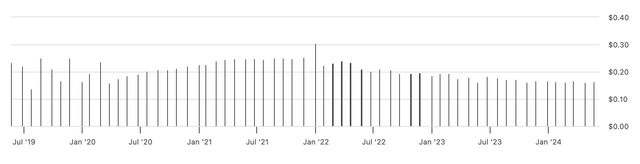

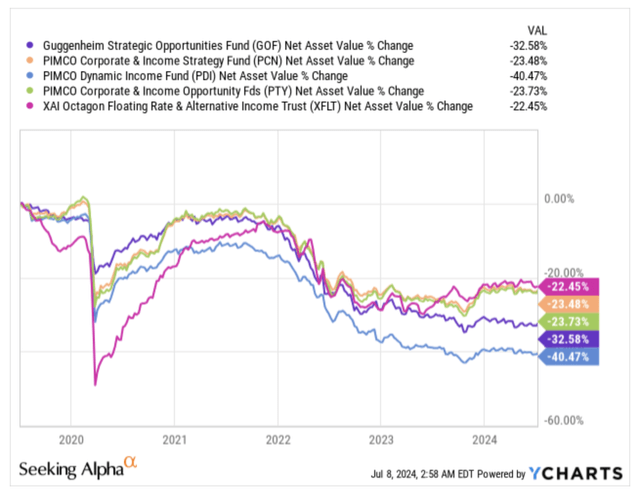

I have some concerns also about the four fixed-income CEFs (GOF, PCN, PDI and PTY) and XFLT. Given their NAV performance in the last five years, I keep having doubts about the long-term sustainability of the double-digit distributions they pay out, but it is a question I have been asking myself for some time and so far, it has not been answered negatively (indeed, in some cases special year-end distributions have even been paid). Should they return to parity, I think I would lighten them up, if not even close these positions.

CEFs (Seeking Alpha)

This question also applies in part to QYLD and RYLD, which, however, pay variable dividends. On both I still have hopes for recovery, although on the latter I would not mind one day being able to close the position, preferably without losses.

A separate discourse is deserved for RVT, which shows a largely positive NAV since launch, but even this one I probably bought at too high a price and its performance in my portfolio has not thrilled me completely. Again, I will decide the moment it (hopefully) breaks even again.

All the other securities are permanently part of my portfolio and I have no intention of easing (and even less closing) their positions: it is a patrol of 16 CEFs, ETFs and BDCs (BST, EOS, ETO, EVT, HTD, PDT, RQI, UTF, UTG, JEPI, JEPQ, XYLD, ARCC, CCAP, FDUS, MCI) plus USOI, which I hold more for fiscal reasons, as I have already explained in the past.

I would like to expand my positions in FDUS and MCI, the latest entrants, to bring them up to the level of the other stocks that I am more convinced about, but at these prices I am afraid of averaging too much upward. We will see later, if and when I have lightened my other positions.

The Final Sip

As I have repeatedly stated in my previous articles, I am convinced that those of us who invest in high-income vehicles use dividends and distributions from their securities as a complementary source of income. This fact prompts me to advocate ever more strongly that, in addition to the sustainability of such a source of money, maximum attention must also be paid to maintaining the purchasing power of the capital initially committed (something that I had not paid full attention to ten years ago, as evidenced by the subsequent evolution of my first ETFs).

This is a reason why in recent years I have increasingly turned toward selecting securities for my portfolio whose NAV shows a positive trend, demonstrating that dividend payments do not burden the value of the assets in any way, which even tends to increase over time.

The fact that right now my current portfolio is in profit, even if only by one and a half percentage points, attests to the validity of a good part of the choices made at the time of its creation, some years ago. A good part, but not all. Let’s just say that, for the last five mentioned funds, I continue to navigate by sight in stormy waters, hoping that on the horizon is the soothing quiet of Giglio Island.

Read the full article here