Investment Thesis: I continue to rate the stock as a Hold for now, but see potential for longer-term upside.

In a previous article back in December, I made the argument that the outlook for National Bank of Canada (TSX:NA:CA) going forward may be modest, on the basis of modest net income growth, in spite of continued growth across non-interest income for the Financial Markets segment.

Since then, the stock has appreciated by over 22%.

TradingView.com

The purpose of this article is to assess the main drivers of growth for the stock in the current environment, and whether National Bank of Canada has the capacity to see further growth from here.

Performance

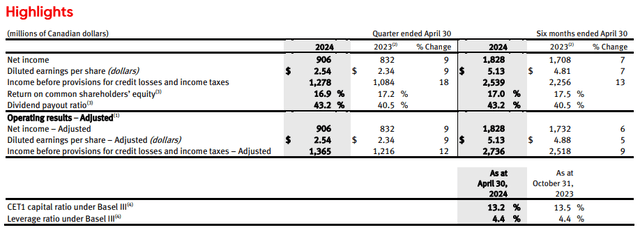

When looking at Q2 2024 earnings results as released on May 29, 2024, we can see that net income and diluted earnings per share are up by 9% each as compared to the prior year quarter, with both of these metrics also up by 7% as compared to the prior six-month period.

National Bank of Canada: Press Release Second Quarter 2024

Additionally, the $2.54 in diluted earnings per share achieved by the bank this quarter came in higher than the $2.42 estimate made by analysts. With that being said, we also observe that Personal and Commercial net income saw a decline to $311 million in Q2 from that of $335 million in the prior year quarter.

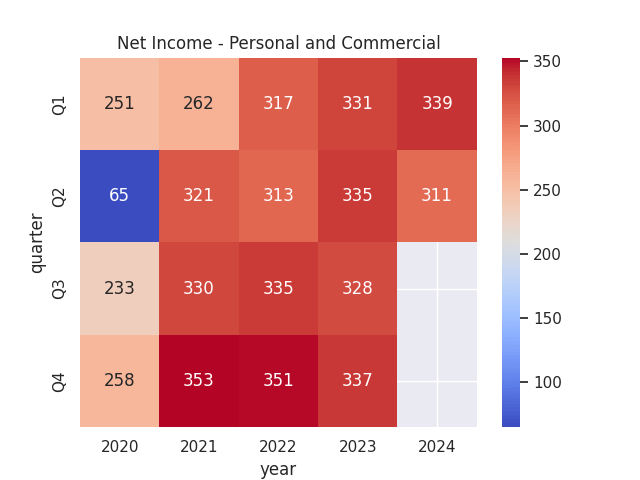

Figures (in millions of Canadian dollars) sourced from historical quarterly National Bank of Canada reports (Q1 2020 to Q2 2024). Heatmap generated by author using Python’s seaborn library.

We see that when looking at income before provisions for credit losses and income taxes – the Personal and Commercial segment accounts for the highest portion of income at 40%.

National Bank of Canada: Press Release Second Quarter 2024

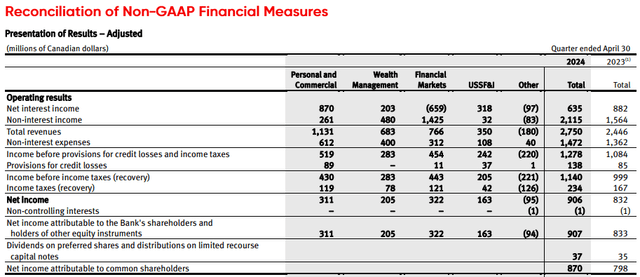

Additionally, total revenues for Personal and Commercial were up marginally from that of the prior year quarter to $1,131 million from $1,100 million – representing an increase of 2.8%. However, while total revenues for Financial Markets saw growth to $766 million from $672 million in the prior year quarter, this was primarily due to growth in non-interest income – whereas net interest income has seen a decline of $659 million in the most recent quarter.

Overall, the National Bank of Canada managed to see respectable growth in net income due to continued growth across the Financial Markets and Personal and Commercial segments.

Looking Forward and Risks

National Bank of Canada’s performance has been impressive in the sense that the bank has managed to continue raising net income even though net interest income has continued to see a decline and provision for credit losses has continued to rise.

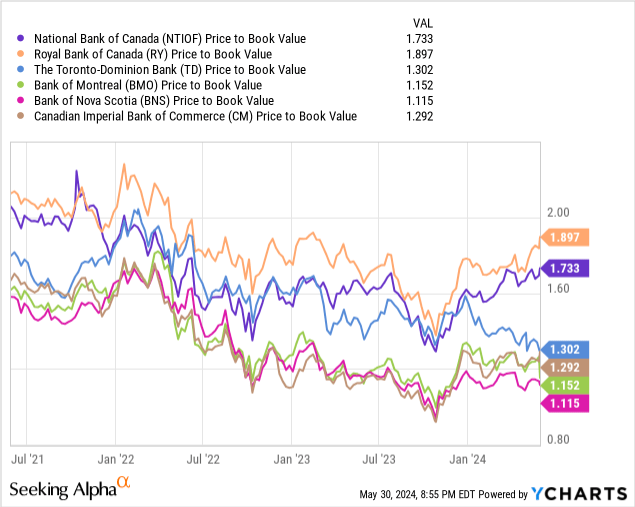

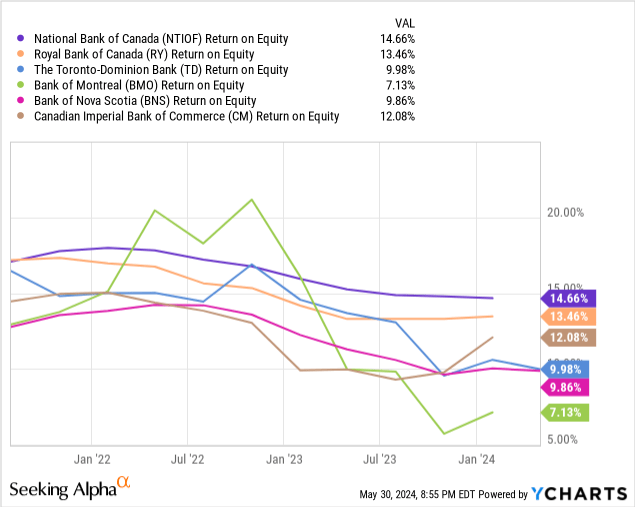

When comparing both the price to book ratio and return on equity to its peers, we can see that while National Bank of Canada is trading on the upper end of the range as compared to its peers with respect to its price to book ratio, the bank also shows the highest return to equity.

Price to Book

ycharts.com

Return on Equity

ycharts.com

In this regard, I take the view that the National Bank of Canada could have the capacity for further upside from here, given that we see rising return on equity coupled with continued net income growth despite a challenging macroeconomic environment – driven by continued strength across the Financial Markets and Personal and Commercial segments.

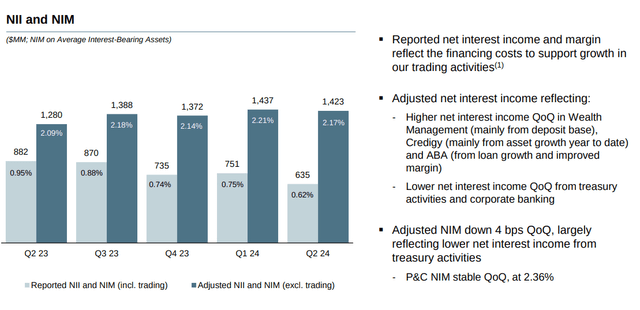

Additionally, we can see that adjusted net interest income and net interest margin has risen by 0.08% from that of the prior year quarter – as a result of higher net interest income in Wealth Management, reflecting a strong deposit base.

National Bank of Canada: Investor Presentation Second Quarter 2024

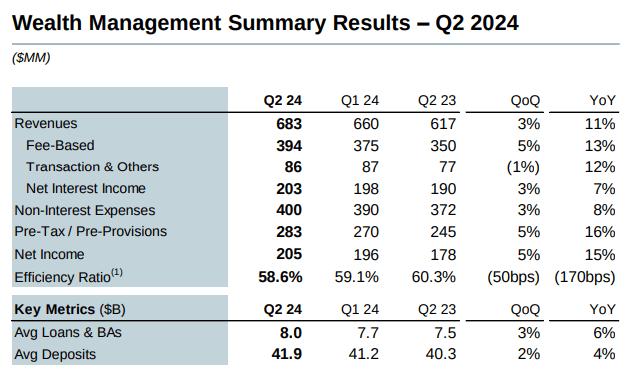

Additionally, we see that revenues for the wealth management segment are up by 11% year-on-year, with average loans & BAs growing faster than that of average deposits on a percentage basis:

National Bank of Canada: Investor Presentation Second Quarter 2024

In this regard, I take the view that the National Bank of Canada’s strategy to continue bolstering net interest income through its Wealth Management segment is a prudent move, as continued growth in fee-based expenses reflects investor appetite for stocks and other fixed-income products – which is in significant part due to lower fears of a recession ahead. Assuming this trajectory continues, then we can expect to see further growth for the Wealth Management segment from here.

Competitors such as BMO Wealth Management (BMO) also saw significant growth, with an increase of 19% to $254 million in adjusted net income due to growth in client assets and stronger global markets. In this regard, growth across the wealth management segment stands to benefit National Bank of Canada’s competitors as well. That said, given the strong growth we have seen for the bank across the Financial Markets and Personal and Commercial segments as well, I take the view that the bank’s capacity for further net income growth is favorable as compared to its peers.

In terms of potential risks for National Bank of Canada at this time, we have seen that it has been predominantly non-interest income that has driven overall growth in revenue and earnings. This could potentially be an issue for the bank going forward, as the Bank of Canada – regardless of whether rates will be cut on June 5 or not – has been taking a cautious approach to the issue of reducing interest rates.

In this regard, there could be a risk that we see downside in the stock if the growth we have been seeing in non-interest income starts to reverse. This could be the case if the effects of higher rates start to significantly impact trading revenues – i.e., should we see a slowdown in broader economic activity in the case that rates stay higher for longer, then this stands to impact growth across the equity markets, which could have a knock-on effect for growth in trading revenues more broadly – given that equities account for the highest portion of trading revenues.

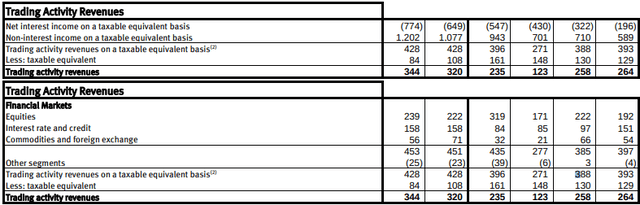

For instance, we have seen that trading activity revenues were up to $344 million from that of $258 million in the prior year quarter. However, we see that growth in equities over this period was up by 7%.

National Bank of Canada: Press Release Second Quarter 2024

Should we see a situation where equity growth slows further – which could be the case if interest rates continue to remain high – then this could negatively impact non-interest income.

Conclusion

To conclude, National Bank of Canada has seen impressive earnings growth in spite of a challenging macroeconomic environment. That said, the bank is highly dependent on further growth in non-interest income to sustain overall growth, and should continually higher rates negatively affect trading revenue going forward, then we could see a reversal in growth for the stock.

While I continue to rate the stock as a Hold for the present time, I see potential for longer-term upside based on the bank’s overall resiliency in a challenging macroeconomic environment.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here