Investment Thesis

Navios Maritime Partners (NYSE:NMM) deals in owning and operating tanker vessels and dry cargo. It provides shipping services mainly in Asia, Europe, and America. The company has recently reported its strong quarterly results and I believe it can sustain this performance in the next quarters as a result of positive industry trends and its expansion of vessels.

About NMM

NMM is a global company that owns and operates tanker vessels and dry cargo. The majority of the company’s revenue is earned by charging customers for the use of its vessels to transport their dry, liquid, and containerized goods. These seaborne shipping services are offered under long-term charters. Its business is geographically diversified in Asia, Europe, and America and each of the geographic regions contributes 63.40%, 22.90%, and 13.65%, respectively to the company’s total revenue. The company’s portfolio consists of 175 vessels, diversified across three segments and more than fifteen asset classes. It is highly focused on a mixed fleet of tankers, dry bulk, and containership vessels to utilize sector-specific opportunities. It has also actively managed to grow its fleet by 45 vessels in the NNA merger, and 29 vessels in the NMCI merger.

Financials

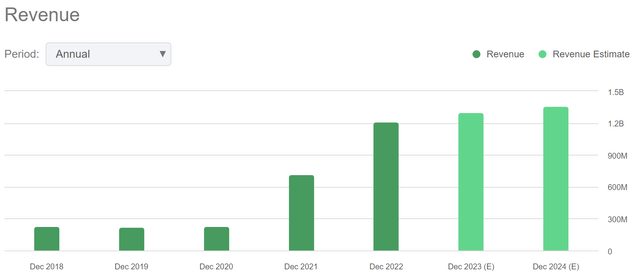

Revenue Trends of NMM (Seeking Alpha)

The company has experienced a slight decrease in revenue in the period of pandemic as its revenue has decreased 5.18% YoY in FY2019 compared to FY2018. The pandemic negatively affected the seaborne trade activities. However, since FY2021 the company has experienced higher tanker rates than its long-term averages because of solid supply and demand fundamentals, which is also reflected in its financial performance of FY2021. The company has reported revenue of $713.18 million in FY2021, which is 214.5% growth compared to $226.77 million in FY2020. It has managed to sustain this solid growth in FY2022 as well and reported $1.21 billion which is 69.7% YoY growth.

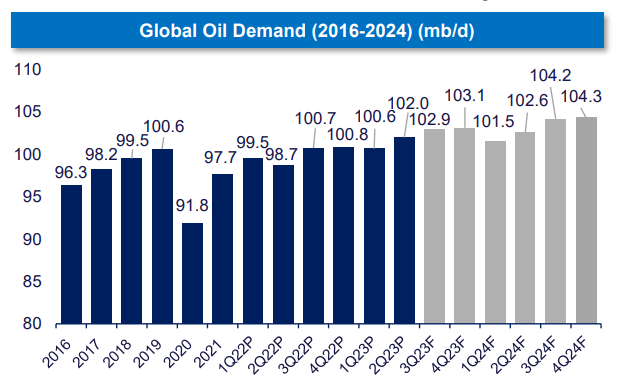

The seaborne trade activities were impacted after the pandemic, and later it experienced a hurdle to rebound the growth as a result of inflationary pressures and geopolitical issues. However, the scenarios are gradually changing in 2023. Though the growth has not surpassed the pre-pandemic levels, it is still steady. The tanker business highly depends on the global oil demand. Economic growth is said to drive the oil demand, as they are 85% correlated. According to a recent projection by the IMF, world GDP can rise by 3% in 2023 and 3% in 2024. The oil demand is also anticipated to grow as marine trade activities for one of the major dry commodities such as Iron Ore is estimated to grow by 2% in China and 3% in Europe. All these positive growth factors have created opportunities for the participants. Identifying these opportunities, the company has planned and completed some acquisitions of vessels to expand its capabilities. It has taken delivery of three newbuilding Capesize vessels. Recently, in August it also agreed to acquire one Kamsarmax vessel for $28.0 million, which is expected to be delivered in the third quarter. In addition, the company has also agreed to execute the acquisition of two newbuilding Japanese MR2 product tanker vessels. These vessels are expected to be delivered between 2026 to 2027. I believe this expansion can significantly increase the revenue of NMM as it helps the company in the accommodation of larger cargo volumes and facilitates it to capture the growing demand by creating capacity for additional shipping contracts. As per my analysis, this growth might be sustained for a longer period as a result of a rise in energy trade and population growth, which can boost trades of essential commodities.

Global Oil Demand Estimates (Investor Presentation: Slide No: 20)

The company recently reported its quarterly results. It reported revenue of $346.93 million, up 23.61% compared to $280.66 million in Q2FY22. This growth was mainly fueled by to expansion of the fleet and a marginal increase in the Time Charter Equivalent (TCE) rate. The company has managed to beat the market’s revenue expectations by $28.94 million, or 9.1%. Net income dropped by 4.95% YoY from $118.16 million to $112.30 million. The decrease in net income was driven by a rise in time charter, voyage expenses, and rise in debt. The decreased net income resulted in an EPS of $3.65. However, the company has managed to surpass the market’s EPS consensus by $0.77 or 26.7%. NMM reported $270.05 million in liquidity and adjusted EBITDA stood at $201.6 million.

EPS Estimate Calculation (Value Quest)

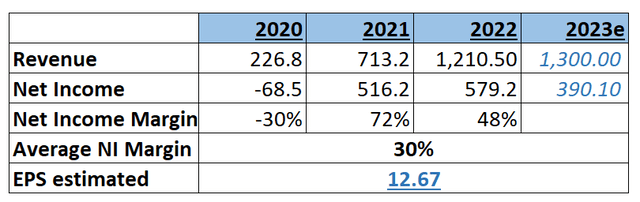

The firm managed to perform well despite the macroeconomic pressures, which reflects its resiliency. I believe the company can sustain this growth in the future as the management has confirmed that supply & demand fundamentals are intact, and the company is continuously focused on expanding its capabilities which can help it to capitalize on the growing opportunities. According to Seeking Alpha, the company’s revenue might be $1.30 billion, which is 7.44% YoY growth. After considering the rising seaborne trade activities and supply & demand fundamentals, I think Seeking Alpha’s revenue estimate is accurate. The company’s 3-year average net income margin is 30%. I believe NMM can maintain the net income margin of 30% in the coming period as the management has confirmed that the supply & demand fundamentals are still intact. Therefore, I am estimating a net income margin of 30% for FY2023, which gives an EPS of $12.67.

What are the Risks Faced by NMM?

Rising Debt:

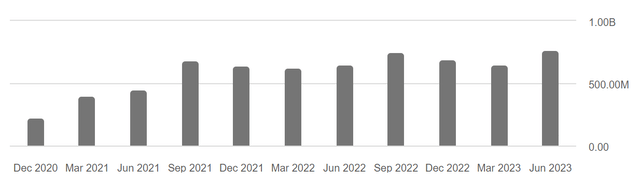

Long-Term Debt Trend of NMM (Seeking Alpha)

The company’s debt has increased significantly in the last few years. Its long-term debt was $763.4 in Jun 2023 which is 234% growth compared to Dec 2020. NMM’s 36% debt has a fixed interest rate of 5.6% while the other 64% has a floating interest rate of 7.8%. The company’s large part of the company’s debt is subject to changes in market interest rates. Currently, the interest rates are rising in the market to counter the rising inflation. Therefore, if the interest rates continue to rise in the coming period, it can significantly affect the company’s net income margins.

Dependency on the Chinese Market:

China is one of the prominent markets for the company, as it imports large quantities of raw materials from other countries and exports significant amounts of semifinished and finished goods. For instance, in 2022, China imported iron ore of 1093 billion tons which represented approximately 74% of the international marine iron ore trade. It also contributed 19% to the global marine coal movements in 2022. If the levels of imports and exports decrease due to changes in the country’s economic policies, it can negatively impact the company’s charter business and reduce its profit margins.

Valuation

The oil demand is highly interlinked with global GDP growth. The world GDP and oil demand are estimated to grow decently in 2023 which can create significant opportunities for the shipping industry. I believe the company’s plans to expand its vessels through acquisitions can accelerate its growth by helping it serve a large number of customers and capture the growing demand in the market.

After considering all the above factors and revenue & net income margin estimates, I am estimating EPS of $12.67 for FY2023, which gives the forward P/E ratio of 1.68x. The company’s forward P/E ratio of 1.68x is 90.3% lower compared to the sector median of 17.30x. NMM’s primary competitors are Global Ship Lease (GSL), Genco Shipping & Trading (GNK), Diana Shipping (DSX), and Safe Bulkers (SB) as all of them offer marine transportation and have market capital in the same range.

Peer comparison of P/E ratios (Value Quest)

The company’s forward P/E ratio of 1.68x is 76.4% lower compared to the industry average P/E ratio of 7.11x. The comparison of forward P/E ratio of NMM with industry average and sector median P/E ratio indicates the company is significantly undervalued.

I believe the company might grow in the coming quarters as a result of positive demand in the industry and intact supply & demand fundamentals which can help it to trade at industry average P/E ratio as according to mean reversion theory P/E ratio has tendency to trend back to average P/E ratio. Therefore, I estimate the company might trade at an industry average P/E ratio of 7.11x in the coming period, giving the target price of $90.08, which is a 324% upside compared to the current share price of $21.23.

Conclusion

NMM has performed solidly in the second quarter despite macroeconomic pressures. The industry has various supportive growth factors which can help demand to remain stable for a longer period, and NMM’s current expansions of its vessels can help it cater to growing demand. However, it is exposed to risk of fluctuations in imports and exports of China and rising interest rates, which can contract its profit margins. The stock is undervalued, and we can expect significant growth from the current price levels as a result of rising sector-specific global opportunities and its expansion of vessels. Considering all the above factors, I assign a buy rating to NMM.

Read the full article here