W. P. Carey (WPC) spun off Net Lease Office Properties (NYSE:NLOP) in November 2023 as the REIT strategically realigned its portfolio and wanted to get rid of its unwanted office assets. The spinoff contained a number of office assets in the U.S. as well as in Europe. Net Lease Office Properties is selling some of its assets, but also generates a significant amount of adjusted FFO from its existing leases. I believe that shares of Net Lease Office Properties remain undervalued based off of book value, and they have continual revaluation potential.

Previous rating

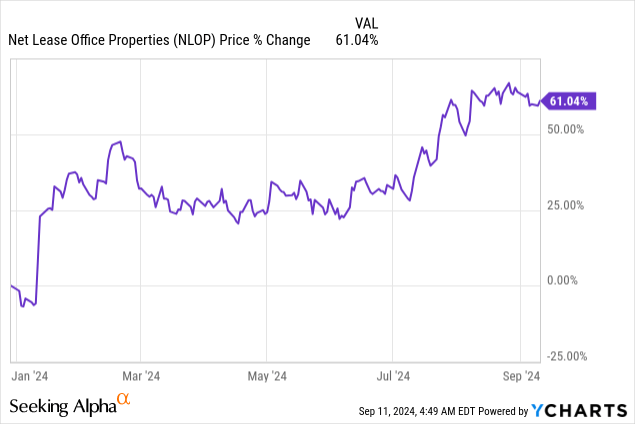

My rating on Net Lease Office Properties was strong buy in May because I saw considerable upside for the office REIT following its spin-off from W. P. Carey. Since my last work on NLOP was published, shares have revalued ~20% higher, but they are still cheap and offer investors an attractive investment opportunity. The REIT is also achieving attractive prices on its asset sales and shares remain widely undervalued, in my opinion.

Net Lease Office Properties continued to sell assets in Q2

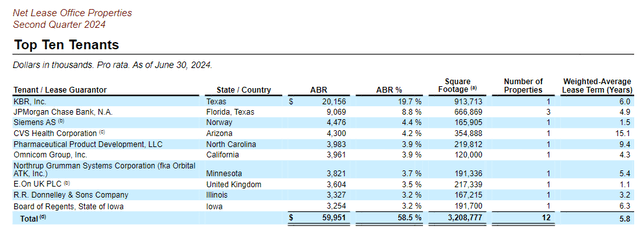

Net Lease Office Properties owned 47 office properties in U.S. and European cities at the end of the June quarter. The REIT’s property portfolio generated $102.5M in annualized base-rent in the second-quarter and had an occupancy of 82.7%. The REIT’s top ten office tenants include banks like JPMorgan Chase (JPM), CVS Health (CVS) and KBR. By far the largest tenant is KBR which represented approximately 20% of the Net Lease Office Properties’ annualized base-rent.

Net Lease Office Properties

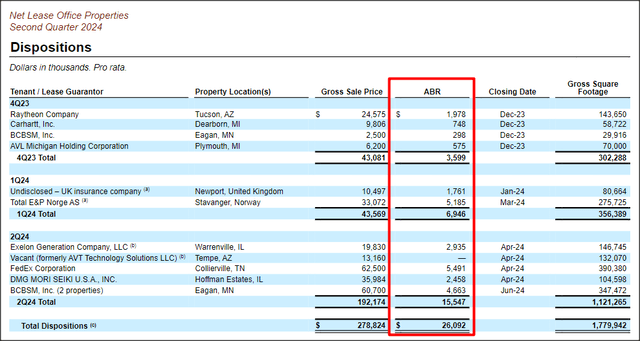

Net Lease Office Properties is selling down its office assets, which also means the REIT is seeing a shrinking net operating income and adjusted FFO basis. In the second-quarter, the REIT sold 6 office assets for $192.2M, meaning Net Lease Office Properties is set to lose more than $15.5M in annualized base-rent going forward. After the end of the second-quarter, Net Lease Office Properties announced the sale of yet another office property to CVS Health Corporation (a top ten tenant) for $71.5M. After this sale, Net Lease Office Properties owned 46 office assets.

Net Lease Office Properties

Net Lease Office Properties seems to receive good prices on its asset dispositions: in the second quarter, the ABR multiplier on office sales was 12.4x, compared to an average of 10.7X since office properties sales ticked off in Q4’23. The multipliers show that Net Lease Office Properties is not selling offices at fire-sale prices, but that the REIT is getting good value here.

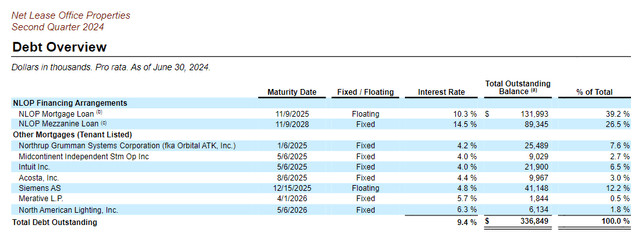

The proceeds of asset sales are applied against Net Lease Office Properties’ debt, of which NLOP had $336.8M at the end of the June quarter. Since the company’s combined assets are still worth much more than Net Lease Office Properties’ financial obligations, I believe NLOP remains an attractive investment for U.S. office investors.

Net Lease Office Properties

Near-term lease expirations are a risk

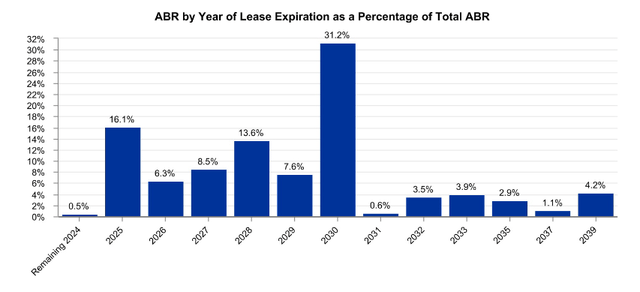

W. P. Carey spun off Net Lease Office Properties because the office market has come under considerable pressure during and after the COVID-19 pandemic. The drive towards remote working has led to falling occupancy rates for office real estate, which affected income projections and property valuations negatively. Further, Net Lease Office Properties has a considerable amount of near term lease expirations: according to the REIT’s updated lease expiration schedule for Q2, the company is set to see more than 16% of its leases expire in FY 2025. Given the comparatively weak negotiating position of landlords in the office market right now, there is a risk that Net Lease Office Properties will have to make lease rate concessions to tenants, which would add pressure on the REIT’s AFFO base.

Net Lease Office Properties

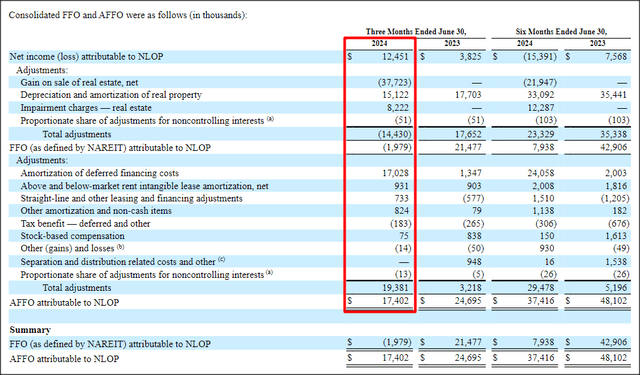

Net Lease Office Properties’ asset sales have led to a shrinking AFFO base, and further asset sales may result in additional declines in adjusted FFO. In Q2’24, Net Lease Office Properties’ offices generated $17.4M in adjusted FFO, showing a decline of 30% year-over-year. Since shares of NLOP still trade way below book value, there is a still an investment opportunity for investors, however.

Net Lease Office Properties

Large valuation discount based off of book value…

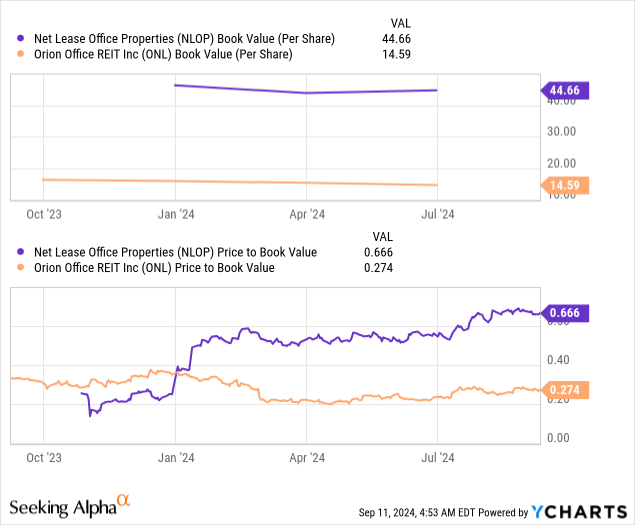

Despite a solid increase in Net Lease Office Properties’ share price of 61% year-to-date, I consider the office spin-off to be undervalued. Currently, Net Lease Office Properties is trading at a 33% discount to book value, which is a lower discount than at the beginning of the year, but shares are still undervalued, especially if the REIT were to sell additional assets above book value. At the end of Q2’24, Net Lease Office Properties had a book value of $44.66 which compares against a share price of $30 which shows a healthy safety margin as well.

A comparable REIT is Orion Office REIT (ONL), which was spun off from Realty Income (O), and which is even trading at a much lower P/BV ratio of 0.27X. I consider the safety margin in the case of Orion Office REIT to be even larger than for Net Lease Office Properties. In the longer term, I would expect NLOP’s share price (assuming no asset sales below book value) to converge upon its book value per-share, which currently stands at $44.66 per-share.

In terms of current AFFO, Net Lease Office Properties generated $1.18 per-share in Q2’24 which implies annualized adjusted FFO potential of $4.72 per-share. This means shares of NLOP trade at just about 6.5X annualized adjusted FFO, which is hardly an aggressive multiplier for a profitable REIT.

Risks with NLOP

The relatively high amount of near term lease expirations is clearly a risk for the REIT. Net Lease Office Properties is likely to face growing pressure on its adjusted FFO in FY 2025 as some tenants may seek lease concessions. The bargaining power of tenants has considerably increased in the office market in the last several years, which could have a negative impact on the REIT’s adjusted FFO even in case it decided to sell no more assets. What would change my mind about NLOP is if the company were to sell office assets well below book value.

Final thoughts

Despite the risks, Net Lease Office Properties could be an attractive investment for investors in the troubled U.S. office market. The main reason for this is that the office REIT is trading well below book value, indicating that investors are still very much concerned about the state of the U.S. office market. Further, Net Lease Office Properties is selling some of its office properties, and at good prices. I believe Net Lease Office Properties represents deep value for U.S. office investors, and consider NLOP to offer an attractive risk profile as well.

Read the full article here