Newmont: Thank You, Jerome Powell

Investors in gold mining leader Newmont Corporation (NYSE:NEM) are enjoying their welcomed revival, as NEM has continued to outperform the S&P 500 (SP500). In my previous bullish NEM update in April 2024, I encouraged investors to remain on board, as there’s more potential upside to capitalize on. My conviction on the battered gold mining leader has played out, as demonstrated by the stock’s resurgence.

Fed Chair Jerome Powell’s semi-annual congressional testimony at Capitol Hill this week has ignited a further rally in NEM and its peers in the VanEck Gold Miners ETF (GDX). Observant investors have likely assessed that Powell didn’t rock the boat with his testimony. The market had already reflected two interest rate cuts beginning in the September FOMC meeting. After Powell’s testimony, the market’s prognostications haven’t changed materially, baking in a more than 70% probability of a 25 bps cut in September 2024.

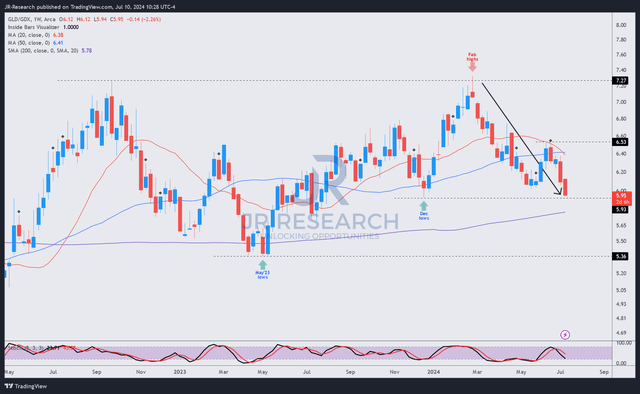

Newmont: Gold Miners Stock Outperformed

GLD/GDX price chart (weekly, medium-term, adjusted for dividends) (TradingView)

Consequently, it has also led to a broad rally in gold (GLD) and gold mining stocks. Notably, the battered gold mining stocks have outperformed GLD since February 2024. As a result, the bifurcation observed as NEM lagged the remarkable surge in GLD has narrowed markedly. I assess the market’s optimism is justified, as the macroeconomic headwinds that affected Newmont’s operational performances are expected to reduce further.

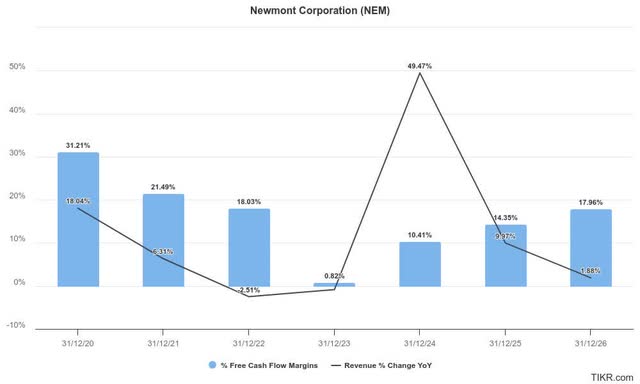

Newmont: Operating Results Could Improve Further

Newmont revenue and free cash flow estimates (TIKR)

As seen above, the company’s free cash flow margins are expected to have bottomed out in FY2023. As Newmont integrates its Newcrest acquisition and capitalizes on the anticipated synergies, it should help improve the operating efficiencies further. Furthermore, Newmont is also expected to divest non-core assets to help bring down its AISC, benefiting the gold miner as it looks to ramp production.

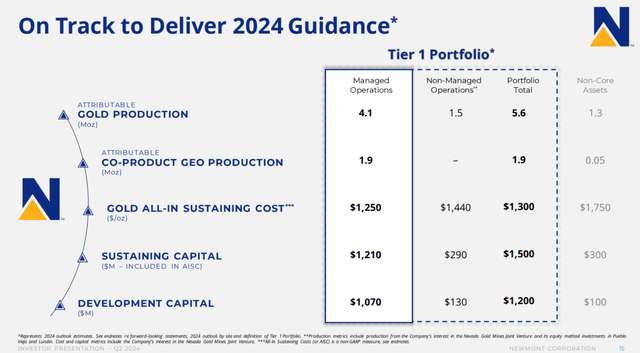

Newmont guidance (Newmont filings)

The corroboration from the Fed’s implied signaling (not rejecting the market’s rate cut assessment) is also expected to be constructive. As a result, it should provide more clarity for investors that inflation and supply chain challenges that beset the gold mining industry are expected to weaken.

Coupled with the underlying bullishness in gold prices, I assess that it should underpin a robust production increase, helping Newmont to lift its FCF margins markedly. Hence, Wall Street’s optimism isn’t misplaced, as the relative outperformance of NEM demonstrates the conviction of gold mining investors.

NEM: Valuation Is Still Reasonable

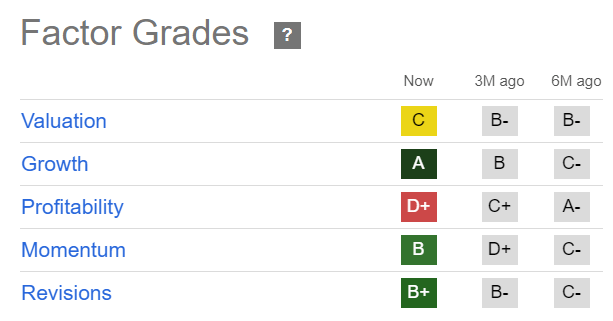

NEM Quant Grades (Seeking Alpha)

While no longer as cheap as it was after outperforming the S&P 500 from the bottom in February, NEM still isn’t expensive (“C” valuation grade). Accordingly, the forward adjusted EBITDA multiple of 7.4x is still more than 10% below its sector median. The “A” growth grade underscores my thesis that the gold mining leader’s profitability is expected to recover further.

As a result, NEM’s forward adjusted PEG ratio of 0.9 remains markedly below its sector median of 1.38. In other words, I have assessed that Newmont has the potential to continue rising further as it executes its multi-year production ramp.

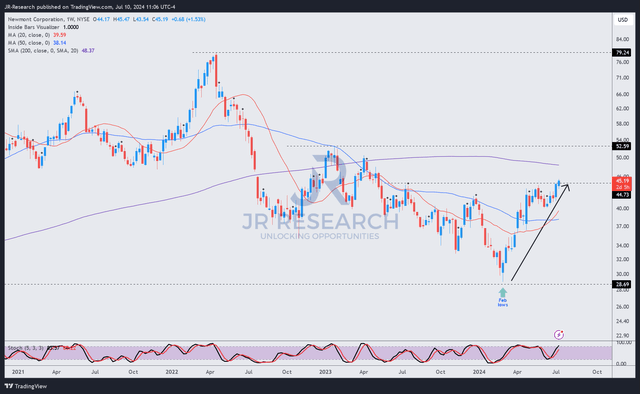

Is NEM Stock A Buy, Sell, Or Hold?

NEM price chart (weekly, medium-term, adjusted for dividends) (TradingView)

Furthermore, NEM’s forward dividend yield of almost 2.3% is reasonable. It’s higher than the 10Y average of 1.95%, which could appeal to income investors reallocating.

However, the 2Y (US2Y) is still hovering close to the 4.62% level. Therefore, a significant valuation re-rating is unlikely in the near term. Notwithstanding my caution, NEM’s price action has indicated increasingly bullish signals, suggesting a decisive breakout above the $45 level has become my base case.

Bolstered by the stock’s appealing valuation and potential for significant operating leverage gains as it emerges from its cycle lows, NEM investors are urged to remain on board. Gold mining investors looking to add exposure should consider Newmont’s robust Tier-1 portfolio and its potential ability to lower its AISC over the next three years. Upgraded Wall Street estimates also underpin increasing optimism about the bullish thesis.

If NEM buyers achieve a decisive breakout from the current levels, I assess a further rally before a potential consolidation zone close to the $52 level.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here