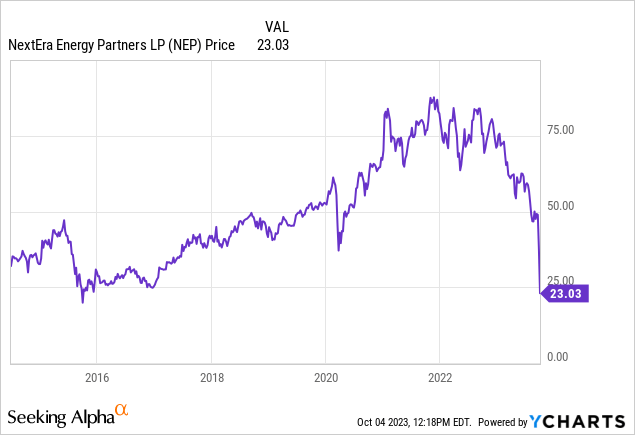

NextEra Energy Partners (NYSE:NEP) has plunged to apparently distressed levels, with a distribution yield well into the double digits. The stock has plunged 50% over the past week alone, triggered by an announcement that the company has lowered its targeted distribution growth rate. I suspect many investors may consider the stock a “slam dunk” at current prices, as a 15% yield looks highly attractive even against the lower 6% targeted growth rate. The problem here is debt, but not the kind that you typically come across. The higher interest rate environment and plunging stock price have made buying out the convertible equity portfolio financings prohibitively expensive and representing a serious liquidity risk. I expect the parent NextEra Energy (NEE) to eventually make a bid for NEP in order to address these concerns, among others. Investors should steer far clear of this stock.

NEP Stock Price

In my last and first report on NEP in August, I recommended readers to avoid buying the stock. At the time, NEP was highly touted by my peers, but I couldn’t reconcile the math to see why this wasn’t just a 7% yield with poor growth prospects. The stock has been clobbered since then and now trades lower than it did 10 years ago.

I didn’t go far enough. My goal in that report was merely to tame bullish expectations. To that aim, identifying that higher interest rates would significantly hold back growth far from the company’s then-target of 8% to 12% distribution growth was just enough. But had I spent more time understanding the ramifications of the convertible equity portfolio financings, then I would have instead rated the stock a clear short. I am kicking myself for that – and to add insult to injury, I even sold a couple puts at a $25 strike price that I have since covered at a nonsignificant loss. Even after a big valuation reset, I must downgrade the stock to a sell – better late than never.

Why Is NextEra Energy Partners Stock Falling?

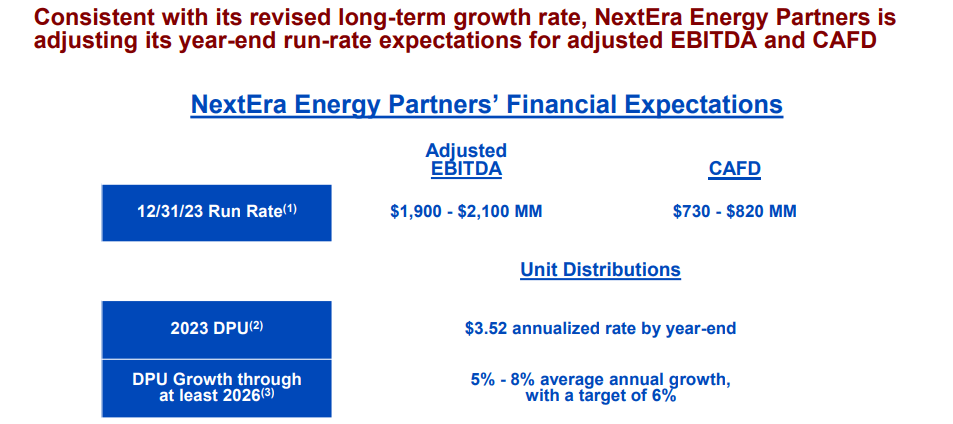

To the unsuspecting eye, the extent of NEP’s stock price plunge looks unjustified. Sure, the stock deserved to fall after lowering both adjusted EBITDA and cash available for distribution (‘CAFD’) guidance from prior targets of $2.4 billion and $860 million, respectively. But the 50% plunge at first glance looks overdone, given that management is still targeting 6% distribution growth through 2026.

September 2023 Presentation

The problem is that 6% growth still looks too aggressive. In my prior report, I have already discussed how higher interest rates should bring growth down to a crawl (due to the company’s heavy reliance on external acquisitions to drive growth), but there I missed something: the convertible equity financing buyouts.

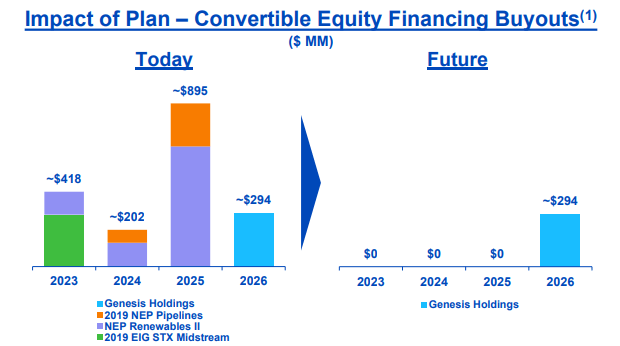

This was an issue that was frequently dismissed due to the company having previously outlined plans to sell off their natural gas pipeline portfolio to raise funds, as well as parent NEE suspending $157 million in IDRs to offset that sale. We can see below that NEP has around $1.8 billion of convertible equity financing that needs to be paid off over the next few years.

2023 Q1 Presentation

In total, there is around $4.6 billion of CEPF that needs to be addressed over the coming years.

2023 10-K

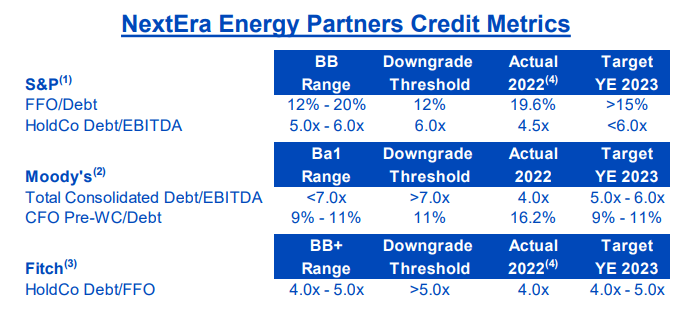

The sale of the natural gas pipelines is expected to address around $1.5-$1.8 billion of that if they are able to sell the pipelines at a 10x multiple. Even if we assume that they are able to execute on such a transaction (which is no guarantee given that the stocks of publicly traded pipeline companies are trading around that 10x EBITDA multiple), they still have around $3 billion remaining to deal with. I am doubtful that NEP could issue additional unsecured debt to raise financing, given that the company is already approaching downgrade thresholds.

2023 Q2 Presentation

Moreover, issuing debt would likely need to come at a 7% to 8% interest rate if not higher, which would heavily impact cash available for distributions. 8% interest on $3 billion in debt would amount to $240 million – compare that against $820 million in projected 2023 consolidated CAFD.

Is NEP Stock A Buy, Sell, Or Hold?

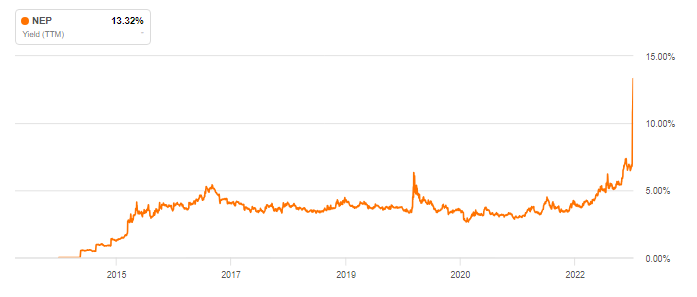

Still, though, many readers may be thinking that the price is right here, with the stock trading at its highest distribution yield ever.

Seeking Alpha

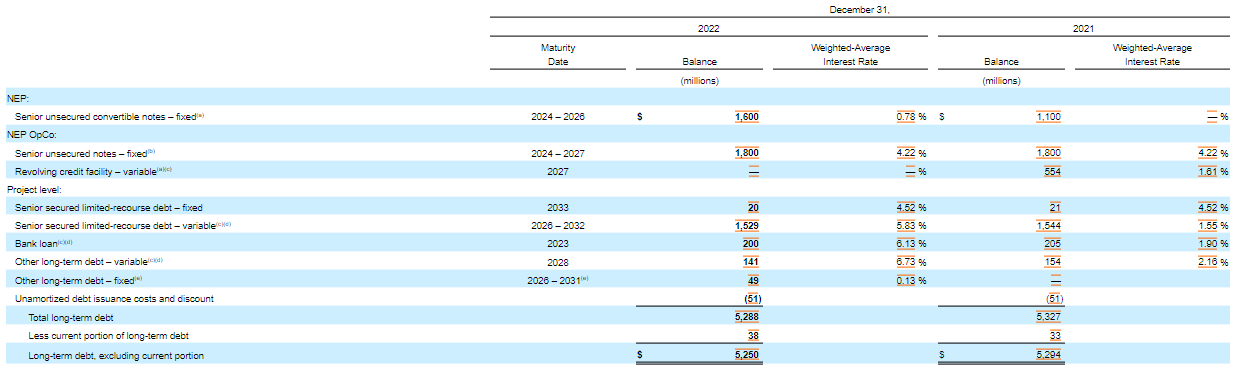

Again, it isn’t so simple. We should first calculate the valuation. There are 190 million shares outstanding (inclusive of NEE shares), yielding a $4.3 billion market cap. As of the latest quarter, there was $5.9 billion of long-term debt, $573 million of near-term debt, and $587 million in cash. I have included a breakdown of the debt from the annual report to show the low interest rates of maturing debt.

2023 10-K

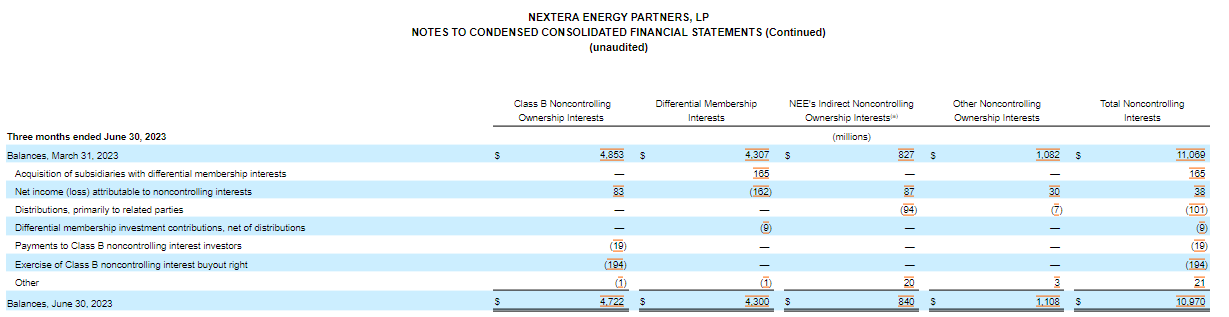

I have seen some peers use the above numbers to conclude that NEP is trading at around 4x EBITDA (using guidance for $2.1 billion in adjusted EBITDA). But the problem is that this ignores the aforementioned CEPF, as well as the differential membership interests. NEP noted having $10.97 billion noncontrolling interests as of the latest quarter, but the bulk of that is not related to NEE’s stake in the company.

2023 10-K

Adding $10.1 billion to the enterprise value yields $20.3 billion in total enterprise value – leading to a valuation of around 10x EBITDA (in line with that reported by Seeking Alpha). This is a good moment to stop and point out that 10x EBITDA is not that cheap, at least not as cheap as the 15% distribution yield might imply. At this point, hopefully, it is at least clear that there is no reason to “back up the truck.”

But the final and most concerning risk is related to how NEP might address the CEPF buyouts. When the stock was soaring and soaring, these buyouts were not so concerning, given that NEP could simply issue stock to fund the buyouts. But now that the stock has plunged, issuing stock is highly dilutive – addressing $4.5 billion in CEPF would potentially dilute unitholders by as much as 50% (and more if NEP continues falling). That puts NEP between a rock and a hard place. Issuing debt is difficult (due to leverage already being high) and expensive (due to high interest rates). Issuing stock is dilutive. So what is NEP to do? Fellow analyst Trapping Value wrote an excellent piece which, among other things, explains the take-under risk. A “take-under” refers to the event in which the company is acquired (often by the parent company) at a price near lows, or at least lower than where many investors purchased their units. At this point, an acquisition of NEP by NEE looks likely as it looks like the easiest way to handle the CEPF buyouts. NEE is incentivized to maintain the value of its ownership in NEP and likely does not want to dilute NEP unitholders (including itself). Acquiring NEP would be a drop in the bucket for NEE, given that NEE is a $100 billion company. NEE would likely have little issue raising even the full $4.5 billion in funds for the CEPF buyouts. As Trapping Value pointed out, there is now the risk that NEP decides to cut its distribution, which may lead to further selling in the units. NEE may sweep in at the lower prices to acquire the company and effectively save it from its liquidity crisis – but unitholders as of current prices might not feel so thankful.

Conclusion

Unless interest rates plunge imminently or for any other reason NEP is able to soar (and raise equity through its ATM program), the CEPF buyouts look like a pressing liquidity risk. Either issuing debt or units look prohibitively expensive, making the company’s target for 6% distribution growth look too aggressive. I expect a distribution cut to occur over the coming quarters, if not sooner, followed by an acquisition of the company by parent NEE at lower prices. I rate NEP a sell as higher interest rates have ruined the party here.

Read the full article here