Note: All amounts referenced are in Canadian Dollars.

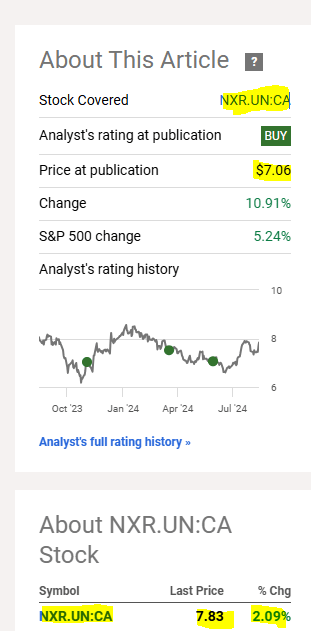

On our last coverage of Nexus Industrial REIT (TSX:NXR.UN:CA) we stamped a third consecutive buy for it, despite a challenging payout ratio.

That said, there is a reason we sold this REIT near $12 in 2021 (it traded at 1.2X NAV) and did not issue a buy rating until it was under $7.50. You need a big margin of safety when the payout ratio is high and the REIT is relatively small. At present, we have it. We did not see anything from Nexus Industrial REIT this quarter to change our view on the bullish front. We maintain our “buy under $7.50.”

Source: 9% Yielder’s Payout Ratio Goes To 120%

The REIT has delivered and is now trading above our “buy under” price.

Seeking Alpha

We looked at the Q2-2024 results to see if we needed to move that “buy under” price a tad higher.

Q2-2024

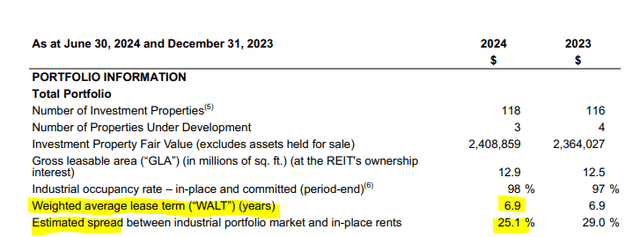

At a high level, the portfolio is doing exceptionally well, with a strong weighted average lease term or WALT and extremely high occupancy levels on industrial properties.

Nexus Q2-2024

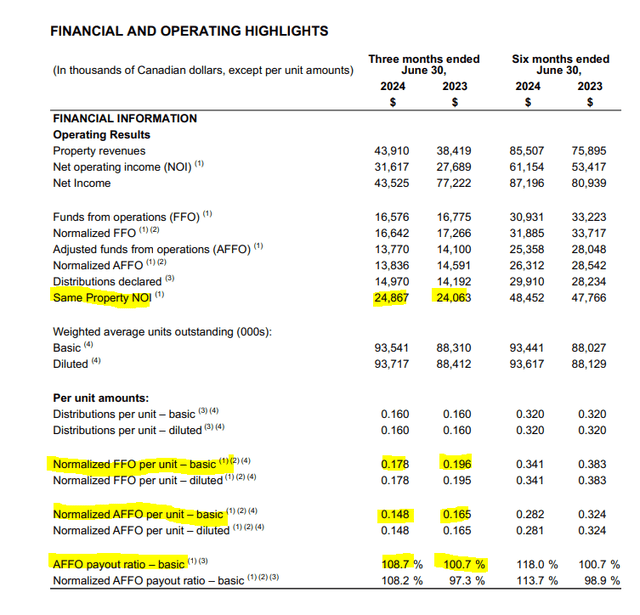

Same property net operating income (NOI) was also up nicely year over year to $24.86 million, a gain of 3.3%. Unfortunately, funds from operations (FFO) and adjusted FFO (AFFO) were both down, pushing the payout ratio once again past 100%.

Nexus Q2-2024

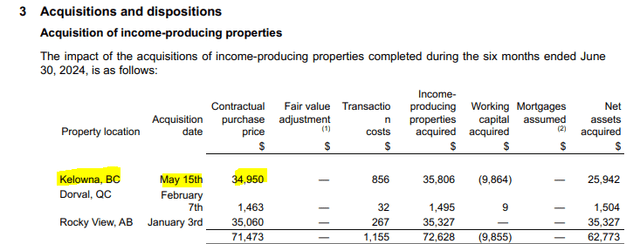

During the quarter a big property was acquired for $34.95 million with the REIT issuing units with a cost basis of $10.00 for the transaction. So far this year, Nexus spent $71.5 million on acquisitions.

Nexus Q2-2024

Dispositions have been focused on office and retail, and the REIT expects to sell a lot more in the back half of this year.

On June 21, 2024, the REIT sold an office property (previously classified as an asset held for sale) located in Blainville, Quebec for a selling price of $5.1 million. Net of selling costs of $0.3 million (reflected as a loss on disposal in the REIT’s statement of income and comprehensive income), the REIT received cash proceeds of $4.8 million. At the time of the disposal, the REIT repaid a mortgage against the property of $3.6 million. As part of its capital-recycling program, the REIT intends to sell 26 investment properties with a carrying value of $121.1 million as at June 30, 2024. These properties are being marketed for sale.

Source: Nexus Q2-2024 Financials

One point to note here is that, the stated amount of sales are slightly different than what was said at the end of Q1-2024 (even adjusting for the office property that was disposed off).

In the short term, we no longer expect to sell our portfolio Western Canada truck terminals. We therefore are now targeting non-core asset sales of approximately $110 million in the second half of 2024. We will use the proceeds from the sales to reduce our debt.

Source: Nexus Q2-2024 Conference Call Transcript

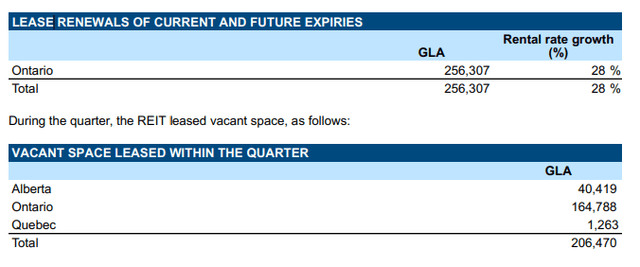

During the quarter, Nexus once again moved opportunistically to hedge its interest rate exposure. They entered into a series of five-year interest rate swaps for a notional $100 million. This fixed the variable rate credit facility at 3.44% (plus required spread). This reduces their borrowing rate substantially on this portion (about 1.5%). Lease renewals were strong as expected, and even some previously vacant space was leased up.

Nexus Q2-2024

The REIT mentioned that it was past a key inflection point for its development properties and expressed confidence in the AFFO payout ratio moving lower over time.

Outlook

Nexus is very cheap when you weigh on a price to AFFO level. The stock still trades close to 11X AFFO on 2025 numbers. The consensus NAV is about $9.66 per share, so it is well below that as well.

TIKR

There is a wide divergence between what the REIT believes its properties are worth and what the analysts believe about the same. IFRS NAV is over $13.00 per unit, and on a different planet than these $9.66 projections. Generally, we have found that we tend to take the more conservative view and come in under the consensus as far as NAV is concerned. Here, we are about a bit optimistic than analyst estimates and think $10.00-$10.50 is fairly reasonable. The small risk here remains that we have a brutal recession and then Nexus will find itself a tad more leveraged than what it will like. Even here, a lot has to go wrong for this to happen. Their debt maturity and lease maturity schedule are fairly long, and the CEO/CFO seem to really know how to hedge interest rate exposure. We have seen a few people do this, and this group has its act together and is probably the best in our view. They have also been fairly creative in acquiring properties by making vendor takebacks in Nexus units above the current price. Down the line, if the stock price improves enough, they can grow in a more conventional manner.

And there’s a huge difference between your trading price and what you’re asking them to take the stock at. So hopefully we can drive. We’ve been building relationships for that. And if the markets open up, I’d like to see us grow substantially again and continue to grow and grow in our nose. We can continue to grow in Southwestern Ontario, like to grow more in the GTA, Montreal. We probably will grow a little bit out West. We do have opportunities out there.

Maybe in the Vancouver, Richmond node, opportunities keep popping up, Kelowna. So at the end of the day, it will be a little bit market dependent. Our hands are tied right now. We’re not about to raise equity anywhere near these levels. So it’s really about straightening out the portfolio, driving down the payout ratio, getting our debt down and then taking it from there.

Source: Nexus Q2-2024 Conference Call Transcript

The odds are high that we will see the dividend maintained and if Nexus does this and gets the payout ratio under 90% by the end of 2025, well, you would expect this to rerate to at least consensus NAV numbers. We did accumulate a nice position as the stock fell. We have no desire to sell our long positions, but we simply won’t be adding anymore. Shockingly though, at a 22% discount to our own NAV estimates, Nexus is not the cheapest REIT we can find. There are better alternatives for us and that is where we expect to focus fresh buys. We are moving this to a “hold”. Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here