Nomad Foods (NYSE:NOMD) is a leading company in the European frozen food market, holding a 16% market share, with well-known brands as seen in the image below. With solid financial health, a management team focused on creating value through effective capital allocation, and expansion opportunities, the market is undervaluing an excellent business.

Due to all the points, I will explain below, I believe the stock is undervalued by the market, and my recommendation is a buy.

Source: Nomad Foods cagny 2024

Company overview

Nomad Foods is a company with very stable growth that produces and distributes frozen products, primarily to supermarket chains. Its main market is Europe, with the UK, Germany, Italy, and France accounting for 60% of its revenue. Its flagship product is fish, which represents 40% of the company’s total operations.

The company’s growth strategy is both organic and inorganic. The former is primarily driven by an increase in volume or prices, while the latter is achieved through the acquisition of new companies to establish itself as a market leader. For instance, “Iglo,” a leading brand, was acquired by the company, enabling its entry into the German market. Another example is “Findus,” a brand through which the company expanded into Italy, France, Spain, Sweden, Switzerland, and Norway.

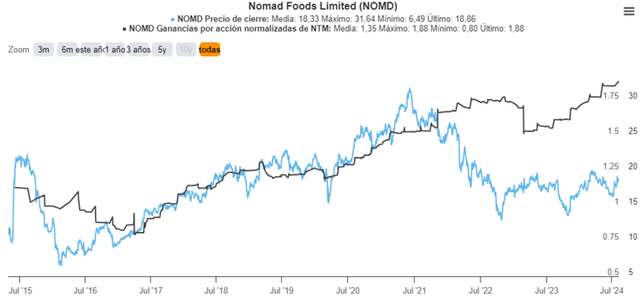

The stock price has declined from $21 to $18.8 over the past five years—a situation that, in my view, is not justified given that sales have grown at an annual rate of 7%, and the company has maintained stable margins.

Source: Koyfin Source: Author’s representation

Market outlook and company guidance

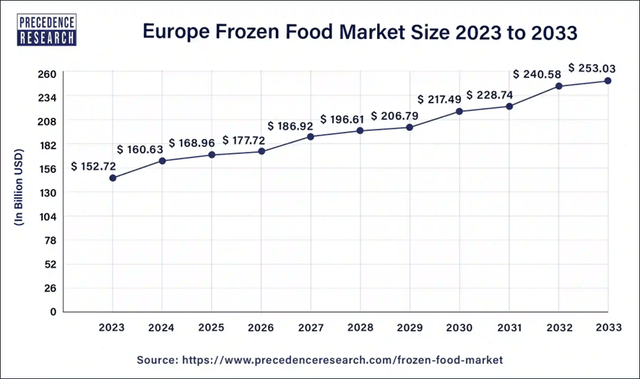

The current total market for frozen products in Europe, where Nomad Foods focuses its business, is valued at $152 billion and is expected to grow to $253 billion by 2033, representing a CAGR of 5% over the next 10 years.

Source: precedenceresearch

In the latest earnings presentation (Q2 2024), Nomad Foods exceeded analysts’ expectations for EPS, reporting $0.44 per share (vs. $0.42 expected), but fell short on sales, posting $753 million (vs. $760 million expected). Despite this, the company reaffirmed its organic growth guidance of 3-4% for 2024.

In my view, the mid-single-digit sales growth guidance is sustainable given market expectations and could be increased to a mid-to-high single-digit range with the help of acquisitions.

Capital allocation: A positive catalyst

Personally, capital allocation is a point I highly value in the companies I invest in. Nomad Foods is a clear example of this.

Firstly, in 2024, the company began paying a quarterly dividend of $0.15 per share, which equates to a 3.2% dividend yield with only a 30% payout ratio. This is the lowest payout in the sector compared to competitors like Unilever, which has a 64% payout, or Kellanova, with an 85% payout. This low payout leaves room for future dividend increases.

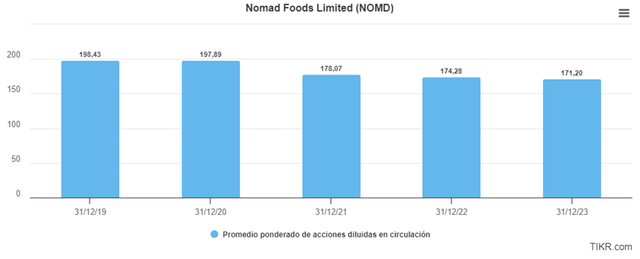

Secondly, share buybacks. In the following image, it can be seen how the management has consistently repurchased shares following the stock’s decline, a move I find appropriate. Additionally, the expected free cash flow for 2024, according to my estimates, is $173 million. If 30% is allocated to dividends, the company would have $122 million available for share buybacks. Being conservative, the company could buy back 3% of its outstanding shares in 2024 at current values if it uses only 75% of that amount. This would further boost EPS growth.

Source: Author’s representation Source: Koyfin

Over the past 5 years, the company has reduced its outstanding shares by 16% due to the low valuation the market places on a stable business with respectable organic growth.

Source: TIKR

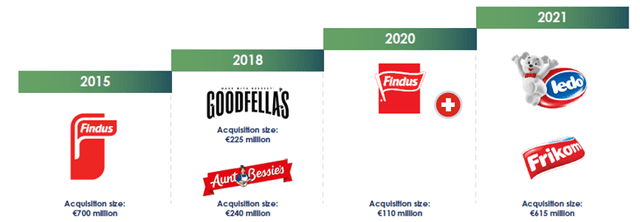

Lastly, the acquisition history. The company’s acquisitions are based on companies with sales greater than $1 billion and paying an EV/EBITDA multiple of less than 10x.

Throughout its history, acquisitions have provided moderate growth, leading the company to reach $3 billion in sales in 2023.

Source: Nomad Foods cagny 2024

Financial overview

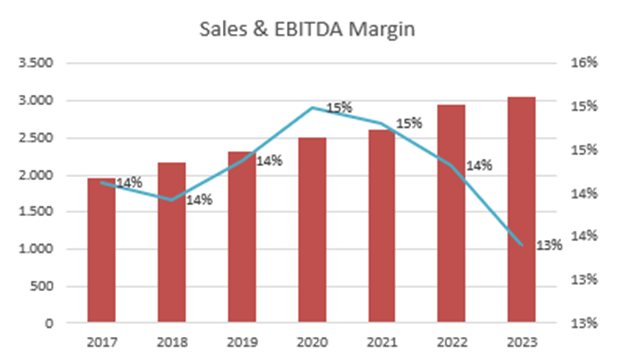

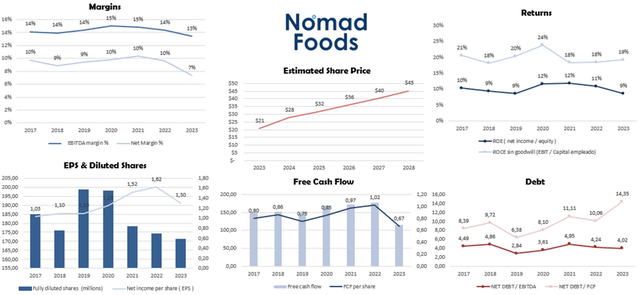

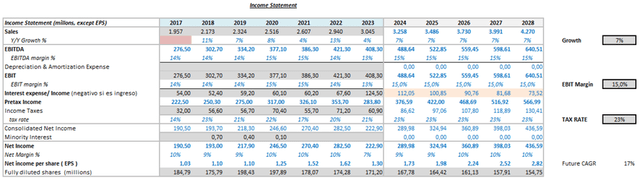

This image displays the company’s financials and their evolution over the past seven years. All metrics have shown growth significantly exceeding the UE GDP, which typically grows around 2%-3% under normal conditions.

Sales have increased from $1.927 billion in 2016 to $3.044 billion in 2023, representing a CAGR of 7%. However, EPS has grown substantially more, at a rate of 33%, primarily due to the share buybacks I previously mentioned as a positive catalyst. The company’s ROE has remained consistent over the years, reflecting its stability. While the ROE is below the market average (15%), the ROE excluding goodwill is well above the market average. Considering the company’s strategy of capital allocation through acquisitions, with the most recent being Fortenova in 2021, I believe it’s appropriate to consider this latter ratio.

Source: Author’s representation

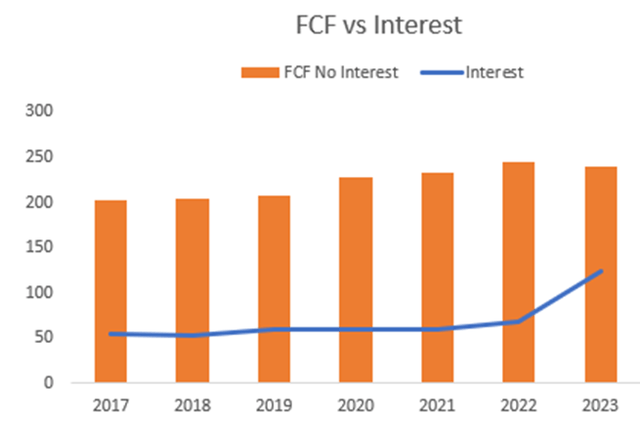

The most important aspect of the company’s financials that I want to highlight is its debt, which typically operates between 3x to 4x Net Debt/EBITDA. Although this is common in a stable sector where most companies operate with leverage, Nomad Foods is among those with the highest ratios, which negatively impacts FCF when interest rates are high, as they are now. This is evidenced by a 40% increase in interest expenses over four years, from $58 million in 2020 to $82 million in 2023.

Source: Author’s representation

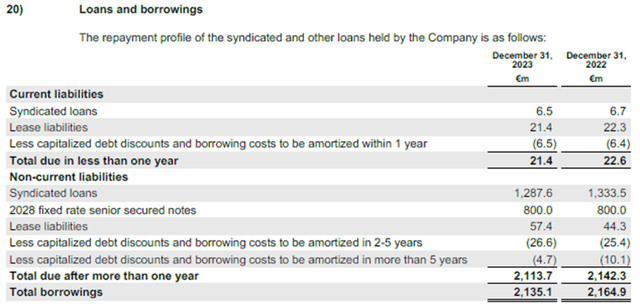

The expansion of the interest/FCF ratio has been largely driven by the fact that of the $2.135 billion the company holds in debt, $1.253 billion is subject to the EURIBOR rate, which is variable and has experienced a significant increase since 2022, rising from negative rates (-0.5%) to 3.5% in 2024.

Source: Balance Sheet 2023

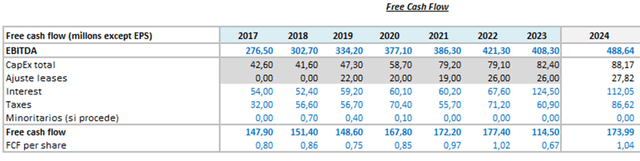

Additionally, I would like to include a chart I designed using information from the company’s financial statements, showing the evolution of its metrics over the last seven years.

Source: Author’s representation

In this image, we can see how metrics such as FCF and EPS were significantly affected by the rise in interest rates from 2022 to 2023.

One final point I want to emphasize is that although companies operating with debt often struggle during crises, Nomad Foods, as a producer and distributor of essential goods like food, typically navigates crises well, maintaining sales, margins, and performance ratios, as was the case in 2020 during the pandemic.

Risks

In my view, there are three risks that can significantly affect the FCF if they are consistent over time.

On the one hand, the dependence of the company on third parties for the supply of raw materials and indirect tasks such as logistics or packaging. For example, a global increase in the price of salmon will have a direct impact on the cost of the product, and there is a certain difficulty in raising the final product price with the same pace.

Another drawback is the seasonality of certain raw materials, especially vegetables. There are raw materials that are produced at specific season, so the company must accumulate stock to meet demand. An error in estimating the required quantity could lead to a loss of raw materials if demand is lower than expected or a loss of potential sales if demand exceeds expectations.

Finally, high interest rates that strongly affect FCF. So far, the company has shown strong financial resilience to mitigate this impact, but if these interest rate levels persist over the next three years, the situation could significantly worsen.

Valuation

The current valuation suggests that the company is undervalued. As we’ve seen in the financial analysis, Nomad Foods has achieved mid-single-digit CAGR across all metrics, but with timely share buybacks, EPS has grown by 33%. Based on Francois Rochon’s idea, which posits a direct relationship between EPS and stock price over the long term, I observe a gap that serves as an initial indication supporting my buy recommendation.

Source: TIKR

In my view, the fair value for NOMD, considering its expected growth, future share buybacks, the stage of the business cycle the company is in, and comparisons with its competitors, would be 15-17 times the P/E multiple at most. Based on my 2025 EPS forecast of $1.98, this would give a fair value range of approximately $31.62 – $33.6.

Source: Author’s representation

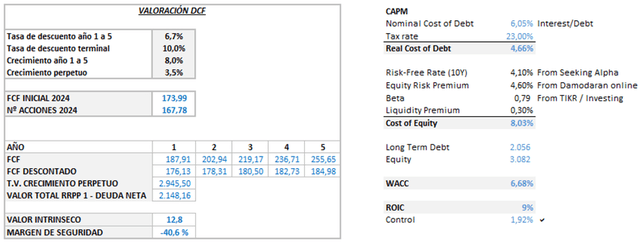

Since I believe that the P/E ratio may not be the best profitability metric, I will also proceed with a DCF valuation.

Considering the following assumptions: WACC of 6.68%, TGR of 3.5%, TDR of 10%, and expected FCF growth of 8% (driven by 4% revenue growth, benefiting from share buybacks as a common company policy, and potentially lower interest rates), I derive a fair value of $12.8 per share. The main difference between this method and the previous one is that in a DCF model, debt is taken into account, so leveraged companies like NOMD are more adversely affected.

Source: Author’s representation

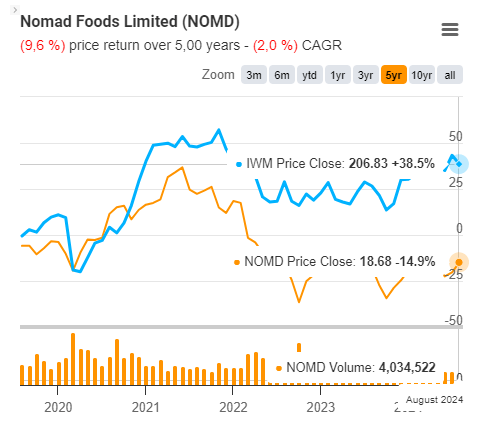

Another chart:

When comparing the performance of Nomad Foods to the Russell 2000, since our company is a small cap, the index has returned 38% to investors, compared to -14.9% for Nomad Foods. This is another indication that it represents a great opportunity, given the cumulative return, as EPS has grown by 33% annually.

Source: TIKR

Conclusion

Nomad Foods is a company with very stable financial health, featuring 4% organic sales growth, stable margins, ROIC without goodwill above the market average, and sound capital allocation that has driven EPS growth by 33%, which has not been reflected in the stock price. I believe that the market is afraid of the current high interest rates and how the company can deal with this situation, but at the moment it is doing very well.

On this basis, I believe that the company is undervalued, and at current prices, it could potentially offer a return of 18% to 20% over the next five years. A stock that has been in my portfolio since December 2023 and I expect it will remain there for many years to come.

Read the full article here