Overview

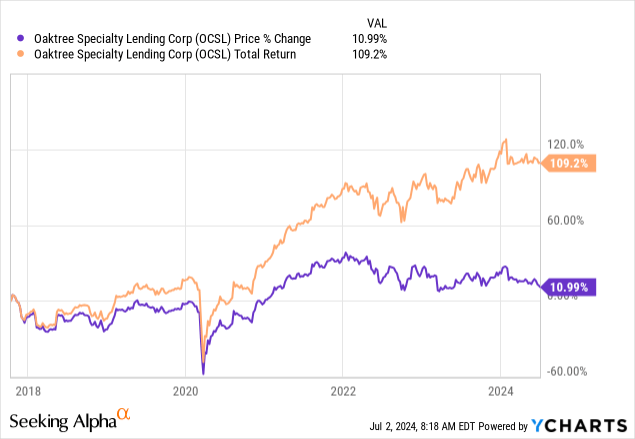

I previously covered Oaktree Specialty Lending (NASDAQ:OCSL) back in March and rated it as a hold due to its price trading at a premium to net asset value and its declining net investment income. However, I wanted to reassess this business development company and provide a more specific time range in regard to its performance. OCSL actually didn’t publicly exist until the tail end of 2017 because prior to this the portfolio was managed by Fifth Street. Therefore, I will no longer be referencing its past price performance prior to 2017. When looking at the price and total return performance starting in 2017, we can see positive price growth and a total return over 100%.

This high total return can be attributed to the consistent levels of high distributions that the BDC issues to shareholders. The dividend yield currently sits at 11.8% and this makes it a highly appealing choice for investors that are looking to add a sizeable stream of income to their portfolio. Since Oak Tree’s take-over of this fund, the distribution history remains quite solid and recent increases in the base dividend has proven that their portfolio is able to efficiently capitalize on the higher interest rate environment.

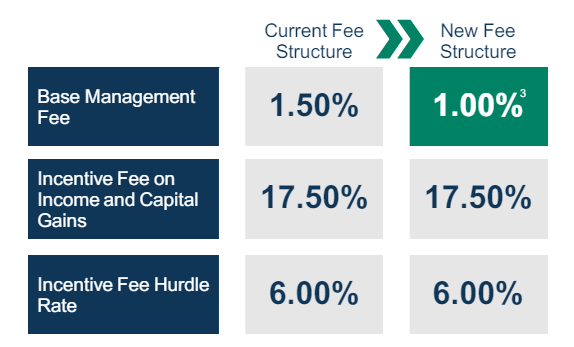

Since the last time I covered OCSL, management has made some changes that have made the fund more appealing. The biggest change was the reduction in the base management fee down to 1%. This creates a larger window of opportunity to see excess earnings that can be passed along to shareholders in the form of supplemental distributions. This fee reduction is expected to increase net investment income per share by $0.15 annually.

OCSL Q2 Presentation

Just to add a bit of context here, Oaktree Specialty Lending operates as a business development company that generates its earnings through different forms of debt investments. They tend to focus on investments within middle market companies, while remaining diverse across what industries and sectors they are exposed to. Let’s start by first reviewing their portfolio structure as well as the investing methodology used.

Strategy & Portfolio

A part of OCSL’s strategy is to remain focused on senior secured debt investments as a way to mitigate risk. Approximately 86% of their overall portfolio is comprised of senior secured debt investments, including first and second lien debt types. This is significant because senior secured first lien debt sits at the top of the capital structure, which means that it has the highest priority of repayment. In cases where portfolio companies may be underperforming and forced to liquidate assets, this ensures that OCSL doesn’t lose all of their invested capital.

Similarly, OCSL focuses on a portfolio of investments that operate on a floating rate basis. Interest rates currently sit at their decade highs, which directly translates to higher earning potential for OCSL. As interest rates increase, so does the required interest payments that borrowers have to make on the debt acquired from OCSL. As a result, OCSL has been able to thrive in this environment and reward shareholders with several base distribution increases as well as supplementals when possible.

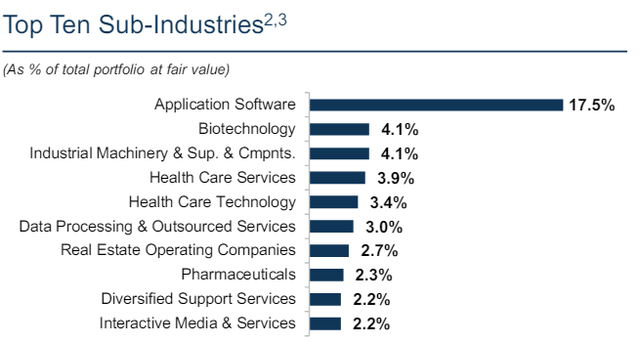

The portfolio of investments remains diverse, although I do see an emphasis on the application software industry, which accounts for 17.5% of the portfolio at fair value. Application software remains the largest industry exposure and the only one sitting in the double digits in terms of weight. This heavy weighting to this sector may present some concentration risk and may slow OCSL’s growth if this specific sector gets impacted by general market conditions. This exposure is followed by investments in biotechnology companies and industrial machinery companies, both accounting for 4.1% of the overall portfolio.

OCSL Q2 Presentation

There are about 151 individual portfolio companies within, with 24 of them belonging to the application software industry. Their investments currently have a weighted average yield of 12.2% and a median debt portfolio company EBITDA of $134M. The top ten investments only account for 20% of their portfolio, so despite the sector breakdown and focus on software, OCSL remains highly diversified. The software slice of their portfolio has a fair value of $579M, compared to the total portfolio value of $3B.

Financials & Risk Profile

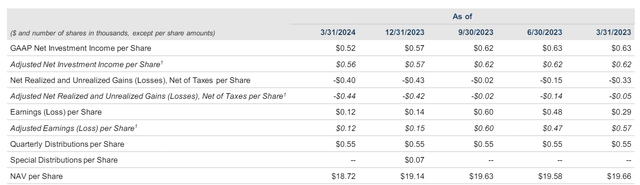

The latest financials that we can reference are from the Q2 earnings reported at the end of April. Net investment income per share landed at $0.56 per share, which was a slight decrease from the $0.57 NII per share reported in the prior quarter, and this was driven by lower adjusted total investment income. I do stay cautious at OCSL’s ability to continue growing NAV over time. Net investment income has been on a steady decline, and it looks like this has directly impacted the fund’s ability to grow the value of their net assets.

NAV per share landed at $18.72 for the quarter, which is a decrease over the prior quarter’s amount of $19.14 per share. We can see that this was due to the combination of a lower net investment income and higher net realized losses within their portfolio. My thoughts are that a big contributing factor to this underperformance is the rise of lower quality borrowers. Interest rates have certainly allowed OCSL to pull in higher levels of income over the last two years, but this also presents a set of challenges. As interest rates remain elevated, this can put additional strain on portfolio companies as their profit margins shrink due to the higher debt maintenance.

OCSL Q2 Presentation

As a result, OCSL’s current non-accrual rate sits at 2.4% of portfolio at fair value and 4.3% at cost. While this does represent a slight improvement from the last time I covered this BDC, I still remain cautious about the underwriting abilities here going forward. As interest rates remain higher, there is likely a lower volume of potential borrowers and investments to choose from. As a result, this could be effecting OCSL’s numbers if investments are forced out of the obligation to continue growing their portfolio. Just as a point of reference, here are the non-accrual rates of peer BDCs.

- Fidus Investment (FDUS): 1% non-accrual rate at fair value.

- Ares Capital (ARCC): 1.7% non-accrual rate at cost.

- Prospect Capital (PSEC): 0.4% non-accrual rate at fair value.

- Main Street Capital (MAIN): 0.5% non-accrual rate at fair value.

On the plus side of things, it’s nice to see OCSL still actively trying to grow their portfolio despite the challenging conditions around interest rates. They have new investment commitments totaling $395M for the quarter, which was allocated towards 20 new portfolio companies and 15 existing portfolio companies. I think when interest rates start to come down, it may present a higher volume of potential borrowers that can better fuel OCSL’s portfolio growth. Until then, liquidity remains strong for OCSL with cash and equivalents totaling $125M.

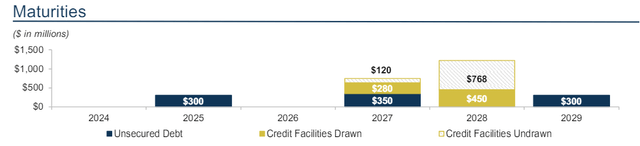

OCSL Q2 Presentation

The debt maturity schedule looks pretty solid, with most of the maturities happening in 2027 and beyond. For now, the cash on hand in combination with the additional credit facilities totaling over $800M that’s accessible, brings their total liquidity up to $1B. Therefore, I see no current threats to their liquidity and there are no concerns to the overall health of the BDC from a balance sheet perspective.

Dividend Threat

As of the latest declared quarterly dividend of $0.55 per share, the current dividend yield sits at 11.8%. I previously mentioned how NII per share for the quarter amounted to $0.56. This means that the dividend is barely being covered by the net investment income, with a coverage rate of 101.82% at the moment. This doesn’t provide a hefty enough coverage for me to feel comfortable with initiating a position. One of the main reasons why investors pile cash into business development companies is because of the reliable, high-yielding dividend income that can be collected. With a very light coverage rate such as this, I feel that the dividend can be reduced at any moment if net investment income per share gets reduced.

A reduction in net investment income is a high possibility when interest rates start to get cut. As interest rates come down, so does the level of interest income that can be generated from their borrowers on a floating rate investment basis. The base management fee reduction was a smart move and will ultimately help offset the losses in NII per share. However, the cut feels a bit disingenuous as it comes off as more of a requirement at this point as opposed to a strategic move to make the BDC more appealing. Just as a point of reference, there are other BDCs out there currently offering a much larger gap in distribution coverage and would make for a better and less risky income investment.

- FS KKR Capital (FSK): Base dividend coverage of 114%.

- Prospect Capital (PSEC): Base dividend coverage of 128%.

- Morgan Stanley Direct Lending (MSDL): Base dividend coverage of 126%.

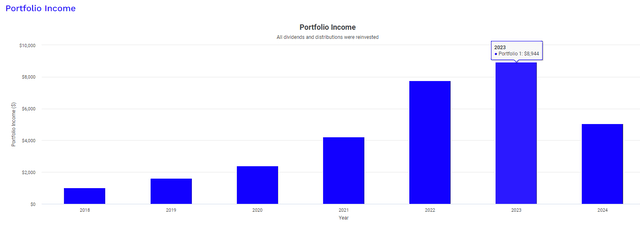

To OCSL’s credit, however, the dividend growth up to this point before the headwinds has been strong. For example, OCSL has managed to increase the dividend at a CAGR (compound annual growth rate) of 14.05% over the last five-year period. This level of growth has made OCSL a great dividend compounder for long-term holders. As a way to display this growth, we can see how an original investment of $10,000 at the start of 2018 would have grown your income using Portfolio Visualizer.

Portfolio Visualizer

This graph also assumes a monthly contribution of $500 throughout the entire holding period, as well as dividends being reinvested back into OCSL. In 2018, your dividend income would have amounted to $1,028 annually. Fast forward to the full year of 2023 and your dividend income would have now grown to $8,944 annually. Something to note, however, is that the distributions received from OCSL are classified as ordinary dividends. Therefore, the distributions here may receive less favorable tax treatment compared to the qualified dividends you’d get from a traditional dividend growth stock.

Valuation

In terms of valuation, the price has trended downward for the year as a result of the lack of meaningful NAV growth. However, the price does trade at a very slight premium to NAV of about 0.5%. This is a slightly more attractive premium than when I initially covered OCSL and the premium sat above 1%. However, these differences are quite trivial and there are plenty of BDCs that regularly trade at massive premiums or massive discounts. A lot of the pricing depends on the fund’s performance around growth of the portfolio, management’s capabilities, and how much excess earnings can be generated from their portfolio of investments.

For a BDC that has failed to show growth in NAV over the last year, I believe we may eventually see the price dip into the discount territory if net investment income doesn’t start to improve and contribute to more growth. However, I would like to revisit over the next few quarters to see how non-accruals have improved and at what rate new investment commitments are being made. I would not recommend entering here simply because of the lack of a large enough distribution coverage. I believe that any signs of weakness in NII per share could cause a distribution cut. If a cut happens, we may see the price come down as investors exit their positions and choose another peer BDC that may be a better performer.

CEF Data

In terms of price movement, Wall St. seems to believe this is a buy at the current price level. Although I disagree, Wall St. has an average price target of $19.94 per share, which represents a potential price upside of over 7% from the current level. The highest price target sits at $21 per share and the lowest sits at $18.50 per share, but I feel that these are overly optimistic. I would like to first see how future net investment income performance is and how heavily impacted OCSL may be when interest rates begin to get cut. Therefore, I am remaining on the sidelines for now and maintaining my Hold rating.

Takeaway

In conclusion, I remain cautious on initiating a position in OCSL at this time. Although the portfolio of investments remains diverse, the emphasis on software companies seems a bit too concentrated for my liking. While OCSL has continued to grow investment commitments, I stay hesitant because of the lack of NII per share and NAV growth. The distribution of $0.55 per share was barely covered by the NII per share of $0.56, which means that with continued underperformance, we may see a distribution cut happen. I would ideally like to see a larger coverage rate to consider OCSL as part of my dividend income portfolio. The lowering of the base management fee was more reactive than proactive, and seemed to be done out of necessity to make up for the underperformance of their debt investments. As a result, I am remaining on the sidelines and continuing to observe for now.

Read the full article here