Investment Thesis For Okta Stock

Okta, Inc. (NASDAQ:OKTA) is a growing company in a fast-growing and potentially massive market. It has strong profit margins, very low debt for a tech company, and cheaply valued book and sales ratios. This young company has massive upside potential for a relatively low stock price.

Okta, A Company That manages Identity Solutions

Okta’s business is providing software for easier access and management to employees’ users. This includes a secure platform for one login step into Gmail, Salesforce, Slack, and others, and tools for managing the workflow.

Okta provides a platform that aims to save other companies money and time. Their platform does not require adding new infrastructure, such as servers, but instead works on top of the existing tech.

Their solutions work for the customers and the workforce, with a clear goal of being a one-stop solution for any company with a bigger than your average small business and a number of users to manage.

The business proposition is aimed at providing easy-to-use, on-the-cloud, secure, and scalable identity software, saving time and money for their users.

Two of the biggest drawbacks are that security breaches into Okta could compromise critical data. However, Okta, as a larger and more experienced player, has deep know-how in security and data protection.

The other problem with the business model is that smaller businesses might not really need such powerful solutions, thus limiting expansion. Okta should, in the future, offer a “lite” version of its platform to better reach smaller mom-and-pop businesses.

Okta: Everything starts with identity (Okta’s Website)

The Growing Market of Identity Solutions

Okta, Inc. is well-placed in an industry that is expected to compound at a rate of 16% CAGR from 2024 to 2032 as the economy grows, and more companies require a platform for customers and workers to access.

Digital identity is also a growing concern for regulators as a way to prevent fraud and increase transparency, and it is reasonable to expect solid growth in the demand for digital identities.

Okta holds a strong position in this market, with 26.91% of the market share, only behind the number one market. OneLogin, a private company from San Francisco, holds more than half of the market share in the single sign-in business. This makes Okta Inc. the largest publicly traded company in the identity and access management industry.

Okta’s Website

Okta Earnings And Income

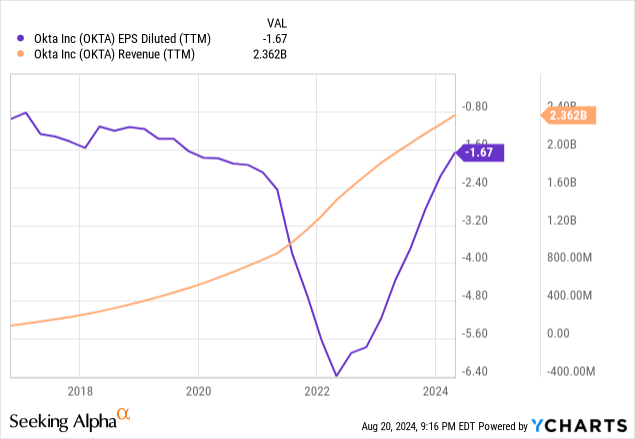

Let’s get straight into this: Okta stock earnings are negative right now. This is the result of the early buyback of debt notes for $937 million, a big hit to the bottom line that put the company into negative earnings territory.

Now that we have that out of the way, we can focus on revenue growth.

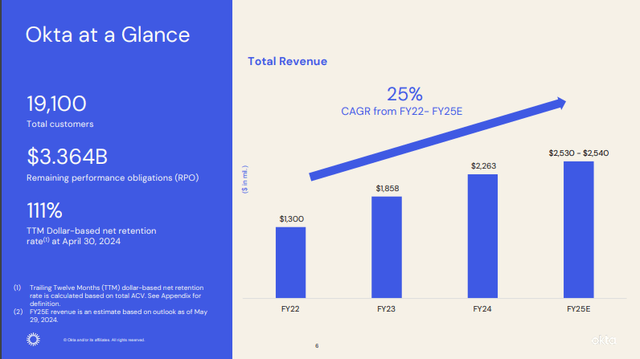

Okta has been growing its revenue for the past few years. It currently stands at $2.362 billion and has a projected 25% CAGR until 2025.

Okta’s Investor Presentation 2024

This is a welcome sight for any bullish thesis and provides a solid foundation for long-term growth.

Their main source of income is subscriptions, a business model that provides a stable and predictable source of income. If Okta can continue its current trend until Q1, 2025, it will have nine straight quarters of growing subscriptions, another positive sign for a bullish outlook.

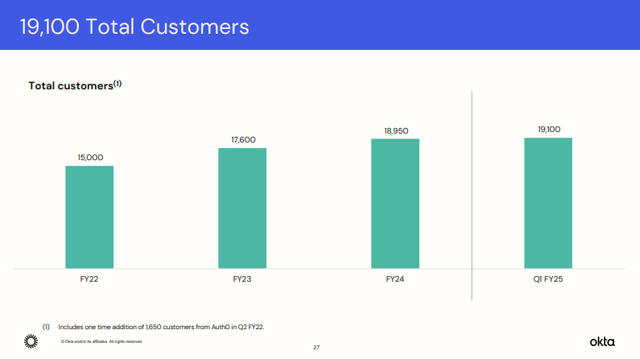

Customers have been steadily increasing for the past few years, with a projected 19,100 for Q1 FY25. I consider this one of the key things to watch; as the industry grows, Okta’s customer base should grow at a rate closer to the industry’s average; if a slowdown occurs, it might be an early warning indicator that the company is losing market share and its position. It should be especially considered as the business model is based on subscriptions, so losing clients means an ongoing loss of revenue versus the one-time loss of sales profits in traditional business models.

As such, I think this is a critical thing that would impact any thesis for Okta.

Okta’s Investor Presentation 2024

Debt And Debt Notes

I believe Okta took a calculated risk buying their debt notes early, per their 10-K

During fiscal 2024, the Company repurchased $508 million principal amount of the 2025 Notes for $462 million in cash and $542 million principal amount of the 2026 Notes for $475 million in cash, resulting in an aggregate gain on early extinguishment of debt of $106 million.

No shareholder wants to wake up and see their stock with a negative P/E ratio, but Okta stock had to endure this for the year ending April 2024.

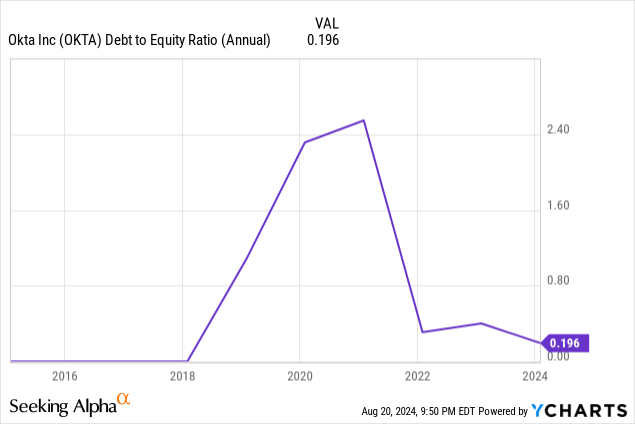

This debt repayment put the debt-to-equity ratio at 0.196, meaning that for every dollar of equity, Okta has $0.196 of debt. This makes it a very financially robust company.

With possible Fed rate cuts on the horizon, Okta could even get more debt at a lower rate besides already getting a $106 million discount off their previous debt.

Even better is the possibility that in the next year or two, of a scaling up of the company and further investments made from a position of financial stability and at lower rates, thus bringing a synergy to the table that would put the Okta stock price into a strong uptrend.

I think this possibility should be considered, as we are talking about a relatively new company in a growing industry where opportunities for increased business abound.

Profitability And Margins

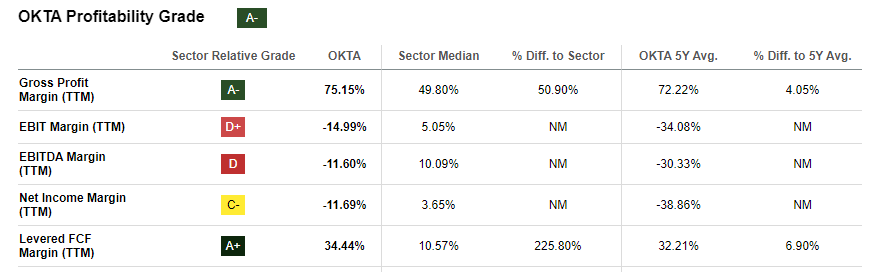

Okta, Inc. has strong gross margins at 75.15%, which shows a strong top line for the company, yet both EBIT and EBITDA are hurt by the previously mentioned early debt buyback.

A strong top line is vital for any business, and for the bottom line, we can actually see that the levered FCF margin is superior to the sector median. This is key for any possible dividends in the future and shows that Okta can handle its financial obligations and still have plenty of hard cash left. With the debt buyback, this ratio only stands to improve.

Seeking Alpha Premium

The strong points here are the high gross margin, with a 49.80% superiority over its peers, and the high levered FCF margin, 225.80% better than the sector median. These are the two advantages Okta has over the rest; with a robust topline and sound financial standing after paying financial obligations respectively, Okta should continue to be a company in a formidable fiscal position, but in my opinion, investors should monitor these. The rest of the margins, as this position, is a crucial ingredient in any fundamental analysis of the company and should be even more closely watched than other ratios.

Competition In The Identity Management Sector

The cloud-based identity and access management industry is relatively new. Okta Inc. (with 26.91% of the market) and its biggest competitor, OneLogin (with 50.56% of the market), both were founded in 2009.

The two companies are also in the same fields, providing customer and workforce identity and access management; they even share the same hometown of San Francisco.

One common issue with companies that manage massive amounts of critical data is security breaches, and these two companies are no exception.

A negative point for Okta: Its security breaches are more recent than those of its competitor, in 2023 and 2022, while OneLogin had its own security breaches in 2016 and 2017.

This is a serious thing to consider, as managing data requires a lot of trust from those who are using the service, and further breaches might hurt Okta’s credibility and those make it lose potential and actual customers, with the loss of ongoing revenue.

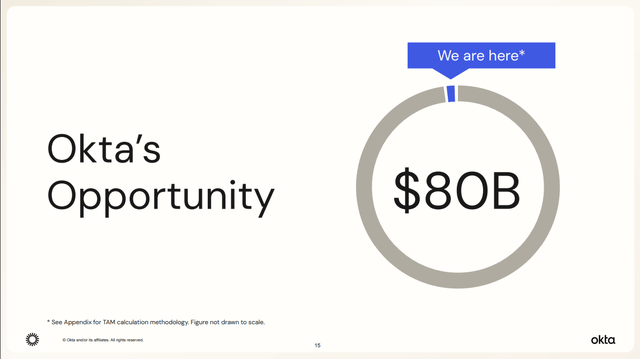

Another danger for this highly competitive environment is the intrusion of bigger players such as Microsoft or even Amazon. With a possible market of $80 billion, by Okta’s own calculation, it is a possibility that in the future another bigger company would tap into its vast resources to offer a version with many improvements over the rest.

Still, Okta is in second place, has strong margins, and very little debt. If it manages to continue growing and improving its business model, it could very well hold its own against the rest.

Okta Investor Presentation 2024

Okta Stock Valuation

The valuation methodology I decided to use is the comparable company analysis, using other publicly traded companies in the industry and similar industries.

I have used gold for those ratios where Okta Inc. is the best and silver for second best.

Analyst own calculations using Seeking Alpha for data and Google Spreadsheets for the table

The valuation methodology I decided to use is the comparable company analysis, using other publicly traded companies in the industry and similar industries. I used gold for those ratios where Okta Inc. is the best, and Silver is the second best.

Revenue growth is 20.45%, which is above the average of 18.49%. EBITDA Growth is quite high at 217.05%. The EPS FWD Long-Term Growth sits at a CAGR of 27% and is well in line with the growth in other income ratios.

Operating Cash Flow Growth also has a strong 100.37% and would have been worrisome if it had been lower, considering the strong top-line metrics like gross margin, which would have shown a weak capacity for turning revenue into cash. Still, fortunately for the bullish thesis, this is not the case.

On more valuation-oriented metrics, Price To Sales is the second best of the group, at $6.40, which is pretty good considering we are evaluating a tech industry company where overpriced sales are common.

Price to book is also a very good metric, being the best of the group at $2.63. Yet, I do not consider such a good metric as the others because tech companies have not been historically capital intensive, but this trend could change with AI, something that also needs to be considered.

Okta and AI

AI is probably one of the most disruptive technologies of this century (and probably much, much more), and any company that can leverage it will have an edge over the competition. Okta has its own spin, with Okta AI focused on security and productivity and using the years of data collected by the company.

As a tech company, AI is a must just to survive the competitive environment. It is too early to say if Okta AI will bring the necessary edge to beat the competition, but it is good to see it in the works.

Okta’s website

Conclusion – Is Okta A Buy?

In my opinion, and after considering the numbers and story, I think the Okta share price is low for the strong metrics, low debt and growing revenues this company has. As the largest publicly traded company in a growing sector, I believe Okta is a good buy and a great long-term investment.

Read the full article here