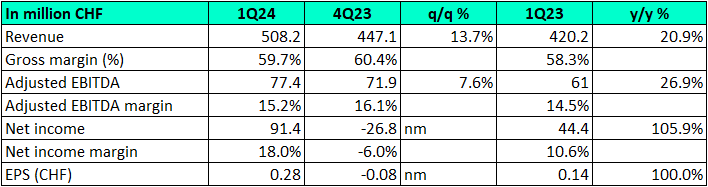

On Holding AG (NYSE:ONON) has reported another stellar quarter, reporting record sales and net income. On a constant currency basis, sales increased 29.2% (or 20.2% in reported currency) and margins expanded thanks to a greater contribution from the Direct to Consumer (DTC) segment. Gross profit margin expanded from 58.3% to 59.7%, Adjusted EBITDA margin expanded from 14.5% to 15.2%, while net margin expanded from 10.6% to 18.0%.

The gross margin is encouraging, because this is well on its way towards the 2024 and medium term target of 60%. On’s Adjusted EBITDA target for 2024 is 16.0%-16.5%, so there is still some work to do. On will likely hit this target if DTC continues its momentum and the currency improves. The substantial improvement in net margin was the result of a massive “foreign exchange result”, which was a CHF 76.8m benefit to the financials.

ONON Company Filings

I mentioned in my previous coverage of ONON that foreign exchange was an “unfortunate yet unpredictable” headwind. In the first quarter, the CHF weakened, after having strengthened in the prior quarter, which gave the results of the company a large boost. This line item is shown on the income statement after the operating results but included in IFRS net income.

It is important to understand the mechanics of this line item. This is not the translation of income and/or expenses across currencies. This is the movement of balance sheet items held in USD that were revalued through the period, resulting in an unrealized gain.

As a result, and given the relatively minor impact of interest received and paid, I think the operating income to be the best measure of the company’s progress from quarter to quarter. On focuses on Adjusted EBITDA, which excludes the impact of stock based compensation, but in On’s case, since SBC is a fairly small as a percentage of revenue (compared to other companies that pay staff in stock and options) I think Adjusted EBITDA is fine to use as well.

1Q24 Result highlights

Management stated on the conference call that adoption of Cloudmonster, Cloudsurfer, and Cloudrunner all were key reasons for the strong performance. The success of these franchises saw market share gains to over 10% in some key cities in Europe, the US, and Asia. The Cloudmonster 2 was released through the period and was very well received by the running community. The second generation of the Cloudrunner was released this week, and the next version of Cloud surfer will be released in late summer.

On Running website

The company is very focused on growing the company through the community as much as from brand marketing. In this vein, local run clubs organized from On stores are helping with growth and brand awareness, and the company also opened new flagship stores in Berlin and Portland, which takes them to 50 stores, 34 of which are operated by On directly. The company flagged that Paris, Milan and Texas will be next.

The Direct to Consumer (DTC) segment did a lot of the heavy lifting, which speaks volumes to the momentum the brand is gaining in the running community. DTC grew sales 39% in Q1 2024 (or 48.7% in constant currency), contributing 37.5% to overall sales, up from 32.6% Q1 2023. The DTC channel comprises both the website and the company-owned stores and as brand awareness grows, I expect this channel to continue to outpace the wholesale channel.

Wholesale grew by 12.2% over the year ago period, and this may not seem like much, but as the brand grows, I think it likely that the brand’s DTC channel will cannibalize some wholesale sales. All this means is that the headline growth number is far more important than the channel growth numbers.

The shift towards DTC is a key measure that will drive On’s gross margin higher over time as there is no retailer in the middle taking their cut. The launch of the company’s first app occurred this quarter, which is expected to be a key communication channel with customers, and to also drive membership growth, which has itself tripled in both of the last 2 years. This is no doubt coming off a small base but a quality product combined with a loyalty program is very likely to be good for sales.

Asia Pacific, while still small, continues to show excellent momentum, growing 68.6% (or 90.7% in constant currency), and made up over 10% of Group sales for the first time. Sales in Brazil also doubled.

Apparel is still a small component of revenue, but a segment that management seems very optimistic on. The category grew 16.7% for the quarter over the year ago period, taking it to CHF 19.7m in sales. On the surface, this looks to be a low rate of growth for what is a category that is still on a small base. However the company noted that they took back some apparel inventory from retailers after they corrected some sizing of their products to better align with consumer expectations regarding fit. This had a negative impact on revenue, making it look lower than the underlying demand was in reality. On expects growth to accelerate aggressively for the remainder of the year and indeed, they quantified this, saying wholesale prebooks for the second half of the year are up 100% on the prior corresponding period.

Short Term Outlook

On has all eyes focused on the upcoming Paris Olympics, seeing it as a key brand building moment with more than two dozen of their sponsored athletes expected to compete at the Games. The highest expectations are no doubt on the shoulders of On Athletics Club member Hellen Obiri, who recently won the Boston Marathon in On gear for the second year in a row. The new Paris store, located on the Champs-Elysees and the second in the city, will be important because it, and the existing store located in the Galeries Lafayette Paris Haussmann mall, will act as a hub for runners at the Games.

On has good visibility of forward wholesale orders and its order book gives it the confidence to reiterate guidance of 30% constant currency revenue growth, which implies CHF 2.29 billion in sales for the year.

Longer Term Outlook

On’s vision is to become “the most premium global sports brand”, and they are doing this by offering high quality footwear and apparel that is backed by innovation and R&D, but they are also doing it by positioning as a premium brand. The recent collaboration with luxury outfit Loewe demonstrates this, which offered an exclusive design of the Cloudtilt show for Loewe at $750, more than 4 times the price of the regular Cloudtilt. This shows On are not just aiming to be a premium sportswear brand, they want to make inroads into premium athletic fashion as well, bordering on luxury. The Loewe collab was a roaring success with the team regretting they did not make more because they would have sold more.

Similarly, On have recently engaged FKA Twigs, a British artist, singer, and dancer, to be On’s creative partner for the Train category. FKA Twigs is not an athlete in traditional, sporting sense, but as a creative dancer will not only showcase the versatility of On’s training category, but as a celebrity, will also show how the brand can be fashionable beyond being worn when active. Further, it would also be expected that she will also extend the brand to her audience, who may be less familiar with the On brand. This could be a brilliant move that combines On’s apparel as functional and fashionable.

Valuation Update

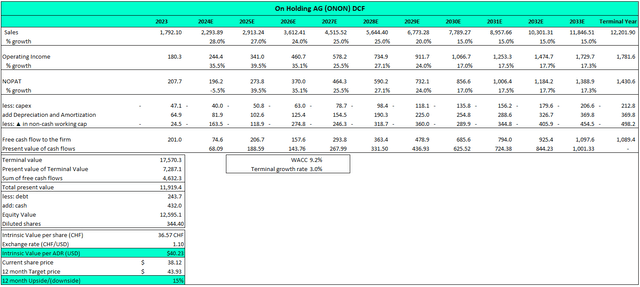

I update my DCF valuation for ONON, rolling it forward from the prior year, and arrive at a current valuation of $40.23. My assumptions are for 20.8% compounded sales growth over 10 years with margin expansion. I think gross margins will level off around the current expectation at 60%, as this is already industry-leading. But operating margins will expand thanks to growing scale and operating leverage, particularly as it pertains to marketing spend as a percentage of sales.

My expectation is that ONON can move towards Lululemon (LULU)-like operating margins, which are consistently above 20%. On’s operating margin is currently 10%, which is about in line with Nike (NKE) and Skechers (SKX). However, Lululemon positions itself in the premium athleisure bracket (Nike and Skechers do not), which I believe garners higher margins. Further, Lululemon is predominantly apparel, not footwear, so as On expands its apparel range and grows it is logical to expect margins to approach this level. I am only modelling for this expansion to bring operating margins to reach 14.6%, which is about half way between NKE and LULU margins, owing to the mix of footwear and apparel.

I am using a WACC of 9.2%, which is based on a peer-derived levered beta of 0.98, a risk free rate of 4.0% and market risk premium of 5.3%. I also use a terminal growth rate of 3%, which is the upper limit I will use in valuations. The modeling is all done in ONON’s reporting currency of Swiss francs, and I converted the valuation to USD at today’s exchange rate of about For simplicity.

Author analysis using FactSet data

Finally, I calculate a target price applying the company’s cost of capital to its valuation, since the cost of capital is the expected annual return assumed by the investor. This provides a target price of $43.93, or 15% upside from the current share price of $38.12. This is more than acceptable for me to call ONON a buy.

Risks

No investment is without risks and they don’t tend to change a lot over time, so anyone who has read my articles before will be familiar with what I view as the risks. That said, it is worth repeating. Firstly, athletic footwear and apparel is a strong competitive environment with many quality and well-funded brands. Walk into any running shoe store and you will be overwhelmed with choice. On has positioned themselves primarily in the maximalist highly cushioned shoe sub-category, which itself is becoming increasingly competitive with incumbents such as Nike’s Vaporfly and challengers like Saucony’s Endorphin Speed or Hoka’s Bondi lines also offering similar technology and results. This is why On is investing so much in the brand. There may or may not be large differences in the technology developed, but athletes will gravitate to a shoe they like as much as a brand they align with.

The other risk is to do with On’s status as a long duration growth company. What I mean by this is there is a long runway for growth, which means that a lot of the value of the company is coming from cash flows that are further in the future compared to a more steady company that is not growing as much. This means the valuation that a long term discounted cash flow produces puts the stock on a high multiple today (currently 37x according to FactSet, but average since listing is 58x).

A high multiple doesn’t necessarily mean the stock is expensive, but it does mean that changes in earnings assumptions will have an outsized effect on the stock price. Changes in interest rates or sudden changes in short term outlook (that is subsequently extrapolated into the long term cash flows) can have very dramatic impacts on the share price. This is not a risk of business failure, but investors need to be able to put up with big swings in share price if they are going to be invested in ONON. Indeed, in the last 12 months the stock has been down 35% peak to trough and is up 60% since that trough.

Seeking Alpha

Conclusion

I like ONON. I have been covering the stock for almost a year now and believe there is immense opportunity in the business. The company is well enough established that there is clear momentum and profitability, but it is early enough that there is plenty of growth in front it if they execute well. That puts it in a sweet spot for me, and the fact that the valuation remains quite reasonable makes this a core position for me. ONON is a buy.

Read the full article here