Investment thesis

My bullish thesis about Opera Limited (NASDAQ:OPRA) which I shared less than a month ago, aged well – the company delivered a 24% rally over the short term. Today I would like to explain why I believe the stock is still undervalued via analysis of recent developments and valuation analysis updates. My valuation analysis suggests that there is still about 20% upside potential for the stock.

Recent developments

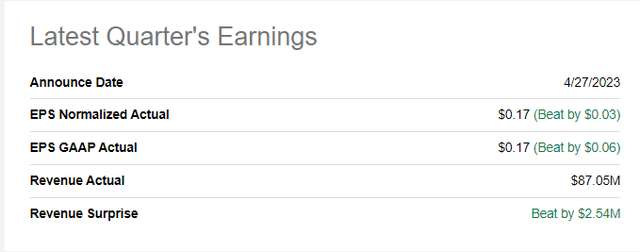

The company released its Q1 2023 financials on April 27, beating consensus estimates regarding the topline and EPS.

Seeking Alpha

Quarterly revenue of slightly above $87 million demonstrated about 22% YoY growth, though sales declined by almost 10% sequentially. I consider sequential decline to be temporary due to increased seasonality. Last year, we have also seen a sequential revenue drop in Q1 of 2022.

Seeking Alpha

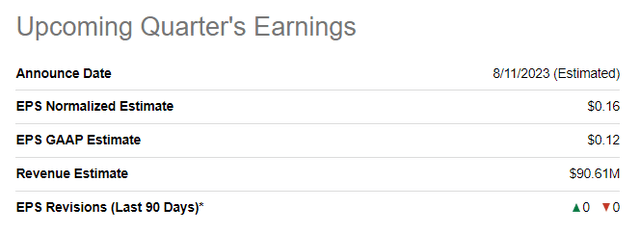

I also believe that sequential drop is also not a problem because management raised FY 2023 guidance to $373-$393 million range up from $370-$390 range declared previously. Another reason why I am positive about the company’s financials is the upcoming earnings consensus estimate for revenue at above $90 million meaning about 16% YoY growth and about 4% sequential growth.

Seeking Alpha

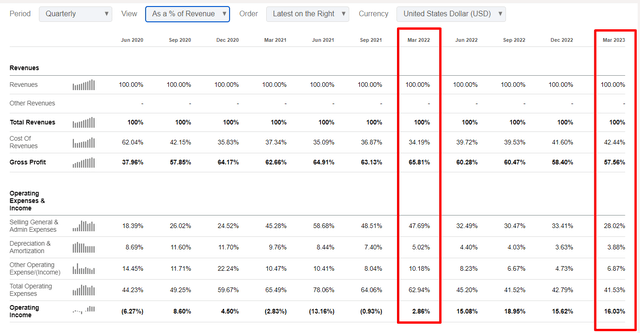

What also looks very positive for me is the operating margin which expanded significantly YoY thanks to substantially lower SG&A to revenue percentage. Improved operating margin enabled the company to almost double cash from operations.

Seeking Alpha

Financial performance over the quarter indicates strong momentum for the company’s operations. One of the company’s most important performance indicators, Average Revenue Per User [ARPU] also supports this idea given a 30% YoY growth.

What I also like since I believe it will give the company secular benefits, is that management reiterated its commitment to AI adoptions. Apart from collaboration with Open AI, during the latest earnings call management announced that users should expect new AI features to be released in the nearest future, according to Song Lin, the company’s co-CEO:

Moving forward, we plan to introduce the new native AI services designed to augment web browsing for our users and further differentiate our products to drive engagement. Earlier this week, we opened up for early access Opera One completely redesigned the browser tailored for AI GC services where AI tools are enabled by default.

Another positive sign for me is the fact that the company has a $30 million remaining share buyback commitment and a $0.80 per share special dividend paid in Q1, which was the first in the company’s history.

Overall, I believe that the company is highly likely to keep the healthy momentum it has been benefiting from in recent quarters. The management looks confident by raising dividends and buying back shares and I also like the commitment to embedding new AI features into its products.

Valuation update

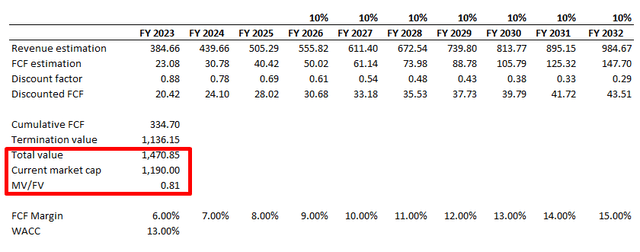

Given the strong latest quarterly earnings and the management’s positive guidance, consensus earnings estimates were also reprojected. The stock also rallied significantly recently, so my previous valuation looks outdated, and I need to reperform it.

I use the same discounted cash flow [DCF] approach as last time. My WACC and FCF margin assumptions were conservative at 13% and 6% for FY 2023, respectively. Therefore, I keep them unchanged, but I would slightly increase long-term revenue estimates given the company’s strong latest quarter performance.

Author’s calculations

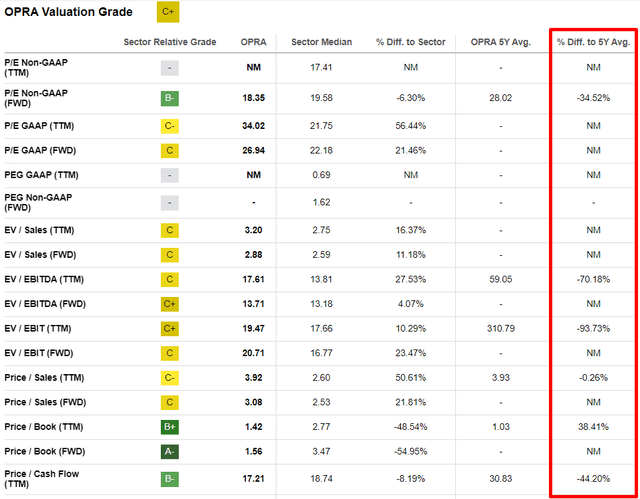

To gain more confidence and cross-check my DCF, I would also like to look at valuation multiples. According to Seeking Alpha Quant valuation tab, the current valuation ratios of OPRA are mostly substantially lower than the company’s 5-year averages. For me, this is also a sign of the undervaluation of the stock.

Seeking Alpha

Overall, I believe that the intrinsic value of OPRA stock is substantially higher than the current market price despite the recent strong rally.

Bottom line

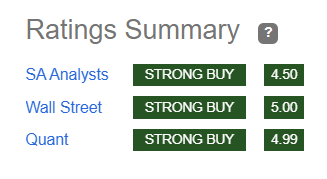

Overall, my updated analysis suggests that OPRA is still a strong buy given its healthy momentum and commitment to keep up with the AI race. The latest earnings have been really strong and near-term guidance also looks bright. Moreover, my valuation analysis suggests the stock is still very attractively valued. So, I absolutely agree with the stellar Seeking Alpha Quant grade of OPRA.

Seeking Alpha

I believe that the risks landscape of OPRA has not changed much in recent weeks so you can check my opinion on significant risks in the previous article available here.

Read the full article here