Introduction

Oracle (NYSE:ORCL): The global business software giant’s shares, have enjoyed a remarkable year so far, surging by approximately 47% year-to-date, culminating in a market capitalization of approximately $317 billion.

In conjunction with the burgeoning emergence of artificial intelligence (AI), Oracle has proactively positioned itself by already communicating its capacity to integrate AI into its product suite, thereby positioning AI as a shaping component of its future business endeavors. The recent ascent in the company’s stock price certainly mirrors the prevailing optimism within the market. This sentiment is further bolstered by Wall Street analysts, as underscored, for instance, by a recent “BUY” upgrade from UBS (UBS).

Nevertheless, this article aims to delve into the reasons behind my inclination towards a “HOLD” stance on Oracle’s stock for now.

Presently, the company appears to grapple with the challenge of providing a lucid numerical projection in terms of both growth and margins for its AI initiatives.

Moreover, a comprehensive discounted cash flow valuation analysis suggests that a significant portion of the current circulating optimism has already been factored into Oracle’s elevated stock price.

As such, prudence warrants a closer examination of Oracle’s ability to fulfill these high expectations and deliver substantial returns to its investors.

Wall Street’s Optimism

Oracle’s stock has experienced a significant boost in recent days, among other things, attributed to the favorable actions of UBS analysts who put out a “BUY” rating for Oracle on Tuesday. UBS argues that Oracle’s edge in GPU capacity, along with their NVIDIA (NVDA) partnership, is in fact underestimated.

These factors are identified as key drivers for attracting new clients and fostering increased Oracle Cloud Infrastructure (OCI) adoption. UBS analysts even speculate that, despite this impressive year-to-date gain, Oracle’s shares may still possess untapped potential, especially due to GPU supply constraints, which have previously driven remarkable performance for cloud infrastructure providers.

Additionally, the anticipation of converting $2 billion in AI start-up commitments into OCI usage fuels UBS’s optimistic perspective. They emphasize Oracle’s potential edge in GPU speed-to-deployment, placing it favorably alongside industry peers.

Personal Interpretation and Future Prospects

Oracle’s Strategy for Enterprise-Grade Generative AI:

Oracle has certainly devised a promising AI strategy tailored for enterprise-grade applications. This strategy hinges on addressing three fundamental aspects: infrastructure, cloud services, and application integration.

By collaborating with NVIDIA, Oracle offers a robust infrastructure for training and serving models at scale, enabled by ultra-low-latency networking. I think one more thing to note in that context is that Oracle can use its own portfolio of tons of data that it has amassed in the past.

Oracle extends its vision to provide accessible cloud services, making generative AI capabilities available to developers and scientists. Collaborations with entities like Cohere empower Oracle to potentially offer versatile generative AI services that can be easily integrated into various business functions. This is likely to facilitate the harnessing of generative AI’s potential without extensive technical expertise.

So far, the main value proposition I see behind Oracle embedding AI into its core business applications is driving efficacy and innovation across industries. Enabling organizations to automate tasks, elevate decision-making processes, enhance customer experiences, etc.

Nevertheless, while Oracle’s direction holds promise, I would rather remain cautious. Over the past decade, the company’s revenue and growth across all other key financial metrics have been somewhat lackluster, leading to questions about Oracle’s execution abilities, especially when it comes to new avenues now, such as AI.

I am in no doubt that Oracle is offering solid value to customers, but currently they lack clear capitalization guidance outlooks, especially regarding future margin expectations, etc. Presently, AI’s contribution to Oracle’s revenue remains marginal, which is prompting questions about the justification of its current valuation, which indicates strong optimism.

I am looking forward to read more about the company’s numbers in its upcoming quarterly results, as well as perhaps the outlining of a clearer roadmap in that respect, which hopefully makes the company’s growth prospects expected from AI a little more concrete.

Financials & Valuation

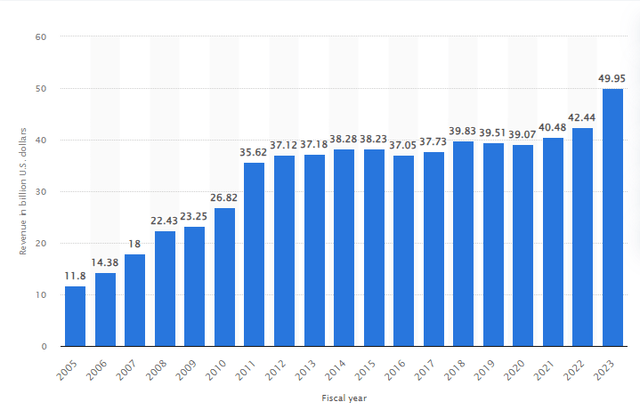

Oracle’s financial performance, including key metrics such as revenue growth, has been notably lackluster.

ORCL – Revenue (Statista )

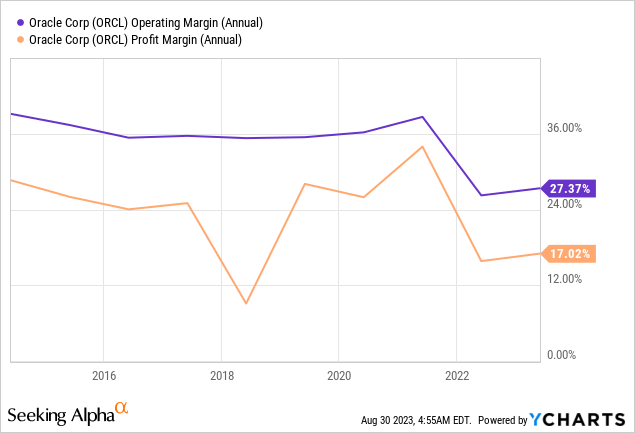

While operational margins have remained relatively stable, except for a significant decline this year, net margins have already experienced gradual deterioration over recent years, contributing to a stagnant net income and free cash flow trajectory.

A Discounted Cash Flow analysis provides deeper insights and gives a view of what must be achieved to justify the current valuation.

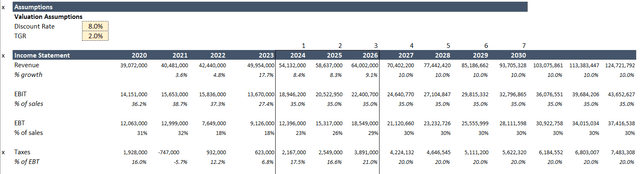

My DCF analysis begins by assuming a turnaround in Oracle’s revenue growth trajectory. Following a recent jump in revenue reported at the end of June for Oracle’s FY23, an assumption is made that the company’s AI initiatives will break the cycle of stagnating growth. A growth estimate of 10% until FY2033 is used. For FY24 to FY26, revenue growth assumptions are based on analyst estimates provided by Market Screener.

ORACLE – DCF – Income Statement (Author)

The analysis also factors in improvements in operating income margins, reflecting an optimistic reversion to the 35% EBIT margin era seen in previous years, starting from FY24. The optimistic assumption is that Oracle’s AI efforts will significantly improve overall margins and sustain them.

Ultimately, I derive Unlevered FCF by adding back depreciation and amortization to EBIAT (earnings before interest after taxes), subtracting capital expenditures (expected to increase), and accounting for changes in net working capital. D&A, CapEx as well as Changes in NWC until FY23 is used from Seeking Alpha.

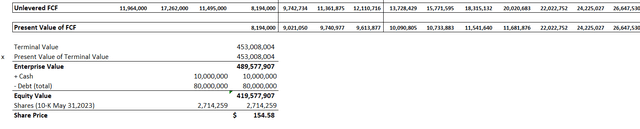

ORACLE – DCF – FCF Items (Author )

A discount rate of 8% and a terminal growth rate of 2% beyond FY33 are applied.

Considering the company’s $10 billion in cash and $80 billion in debt, these optimistic assumptions imply an Equity Value per Share of approximately $150, implying a potential upside of around 30% compared to the current share price of $130.

Oracle – DCF – Equity Value (Author)

While the DCF analysis is constructed with optimistic assumptions, it’s important to acknowledge the inherent uncertainty in predicting future performance. For instance, Oracle’s history of failing to achieve consistent 10% top-line growth casts doubt on the feasibility of such projections in the future. My point is that this evaluation suggests that the current share price might already encompass a considerable degree of optimism without leaving much more reasonable upside.

Final Remarks

Great optimism often guides market sentiment. Oracle’s YTD surge in stock price is a clear testament to that. The current overall momentum for almost anything that contains the letter A, and I add further to this sentiment in Oracle’s stock.

The assumptions I used for my valuation imply that the valuation has already priced in a lot of optimism.

Ultimately, Mr. Market is right, but overoptimism also holds the risk of bringing disappointment, resulting in a valuation adjustment.

Hence, I currently maintain a “HOLD” stance, recognizing that more clarity will emerge with Oracle’s upcoming earnings reports. The impending information will provide a crucial vantage point to reassess the company’s trajectory and its alignment with the market’s optimistic outlook. In the interim, maintaining a vigilant watch will allow for a more informed decision after gaining deeper insights into Oracle’s performance and future prospects.

Read the full article here