Oracle Stock’s Bearish Thesis Less Justified Now

I must admit that my previous bearish thesis on Oracle Corporation (NYSE:ORCL) failed to pan out, as the leading cloud computing and database management company has continued to outperform expectations. Even though Oracle’s “monstrous” cloud infrastructure growth rate has decelerated, its robust backlog has remained highly resilient. Analysts have also revised their adjusted EPS estimates upward, underscoring its operating leverage improvement as it scales OCI further. Therefore, my bearish thesis hasn’t been validated, as the AI growth momentum has proved more sustainable than anticipated.

Moreover, the robust Q1 performance in the leading hyperscaler results suggests a reacceleration in growth as enterprise and commercial customers broaden their generative AI adoption on the cloud. Oracle’s expanded partnership with Microsoft (MSFT) and other cloud computing providers should improve the expansion and reach of Oracle’s leading database management services. Given its less significant scale compared to Microsoft Azure, Amazon Web Services (AMZN), and Google Cloud (GOOGL) (GOOG), Oracle must rely on increased adoption of multi-cloud opportunities to assure investors of its premium valuation (relative to its long-term averages).

Oracle’s fiscal third-quarter earnings release led to an initial post-earnings surge to a new all-time high in ORCL stock. As a result, I have assessed ORCL as still having an uptrend bias, although ORCL suffered a nearly 15% correction toward its April 2024 lows. However, dip-buyers returned with conviction, likely assessing that Oracle is well-positioned to capitalize on increased opportunities from enterprise cloud migration. In addition, Oracle management emphasizes the increased growth cadence in sovereign AI as another growth vector. Management indicated in Oracle’s FQ3 earnings call that it anticipates increased potential in Japan. Consequently, the announcement of Oracle’s $8B long-term cloud investment in Japan underscores the significance of its market potential.

Oracle’s Increased Cloud Investment Is Bullish

As a result, Oracle management’s CapEx guidance corroborates the demand for increased access to Oracle Cloud, as the company guided to an FY2024 CapEx guidance of between $7B and $7.5B. Oracle emphasized that it has experienced “increasing demand for national security and EU sovereign regions.” Oracle’s robust 24% growth in cloud revenue (including Cerner) in FQ3 accounted for the 49% surge in IaaS. While Oracle’s IaaS is in growth mode now, it has a highly profitable legacy platform to underpin its profitability. As a result, it allowed the company to price its Cloud offerings more competitively. Accordingly, Oracle highlighted that “customers are attracted to OCI due to its ability to deliver more while costing less.” Coupled with the company’s proven ability and experience in “running mission-critical workloads at enterprise scale with robust security and support,” I have assessed Oracle’s growth momentum to remain robust.

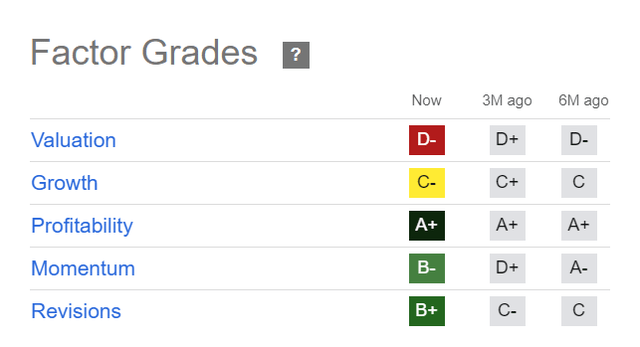

ORCL Quant Grades (Seeking Alpha)

ORCL’s premium valuation (“D-” valuation grade) underscores Oracle’s optimism about its ability to grow faster than its hyperscaler peers. However, over-extended investor expectations could find more significant challenges, as Oracle’s slower-growth legacy business could hinder a more robust growth rating (“C-” growth grade). Although Oracle is a fundamentally strong company (“A+” profitability grade), there is little doubt that its valuation has likely reflected its growth cadence in OCI.

Oracle management highlighted that it expects to expand its penetration in the healthcare space as it integrates Cerner into its cloud platform. Oracle’s recent decision to relocate its headquarters to Nashville could bridge the proximity with healthcare customers. Therefore, penetrating the healthcare vertical more successfully could open up another robust growth vertical that is not captured in the current dynamics. Notwithstanding my optimism, Oracle’s execution on Cerner has been assessed to be worse than anticipated, highlighting the integration risks. As a result, investors will likely remain cautious over Oracle’s cloud opportunities in healthcare until they observe better execution moving ahead.

Is ORCL Stock A Buy, Sell, Or Hold?

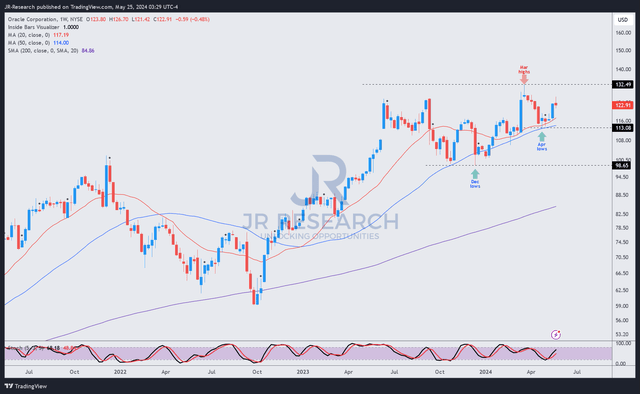

ORCL price chart (weekly, medium-term, adjusted for dividends) (TradingView)

While ORCL stock faced resistance at the $130 level, its buying momentum has remained resilient. As a result, the correction through ORCL’s April lows was stoutly defended by robust dip-buying, helping ORCL recover close to the $125 level last week.

However, ORCL’s buying momentum has struggled to gain traction above the $130 level over the past year, suggesting the market has turned more cautious. As a result, while I view ORCL’s bearish thesis as less justifiable given the more robust AI growth momentum, I have not assessed a buying opportunity yet. Unless ORCL suffers a steeper pullback toward the low-$100 levels to improve its risk/reward, investors might do better staying on the sidelines for now.

Rating: Upgrade to Hold.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here