Investment thesis

Otis Worldwide Corporation (NYSE:OTIS) is in the elevator and escalator business. It manufactures, installs and services lifts. The company’s operations are organized into 2 segments: 1) new equipment and 2) service. OTIS was spun off from United Technologies in 2020 and is now a pure-play on elevators and escalators. For the deal, UTX shareholders received 0.5 shares of Otis for every UTX share owned.

The New Equipment segment focuses on manufacturing + installing a broad range of elevators (passenger + freight), escalators, and moving walkways. The service business provides maintenance and repair services for its products once installed under contract, creating a tail of revenues on the “installed base” [classic razor/razor blade model – new equipments are the razor, service revenues are the razor blade]. The business operates in >200 countries and territories, with deep customer networks consisting of real estate developers, builders + general contractors and governments.

I am indecisive on OTIS for all of the reasons raised in this report. It is drowning in cash, but has no major means to reallocate these funds back into the business outside of growing working capital. As such, all of the freely available cash it throws off each period is typically returned to shareholders via dividends + buybacks. This both sheds capital for OTIS and keeps ROICs high.

There is no issue with this at all, but our preferences are towards companies who produce such exceptional economics as OTIS but with the reinvestment runway ahead of themselves to re-utilize the cash it produces on operating capital. These are true long-term compounders. This is the only factor keeping me on the sidelines with OTIS today, and this must be stressed heavily in the debate.

Figure 1.

TradingView

High-quality business franchise

OTIS has several quality economic characteristics that suggest it is a great business. One of the facts that caught my attention is its relative strength in China. It’s no secret the macro pressures there, with companies in our coverage universe incurring a drag on performance with their China exposures. OTIS is different. Whilst sales are weaker there vs. history (and were down in Q2), the service business was up double-digits in Q2 FY24. It has long-term contracts with Shanghai Metro (inc. 475 units made up of 311 escalators and the remainder elevators]. Management views -10% decline in China sales in FY’24, but it is positive on the segment nonetheless, per the Q2 call:

“[Modernization] MOD orders are up high-single-digit. MOD sales are up double-digit. And we’re really pleased with the pivot we’ve made.

Almost a third of our revenue now in China is in Service, and that’s twice what it was when we spun. Our portfolio has more than doubled and is up again this quarter, as I said, high-teens.

So our service strategy is coming up nicely, and we’re seeing the acceleration of MOD in China and anticipate that to continue to move double-digit as we look out into the medium term for China.”

Q2 earnings insights:

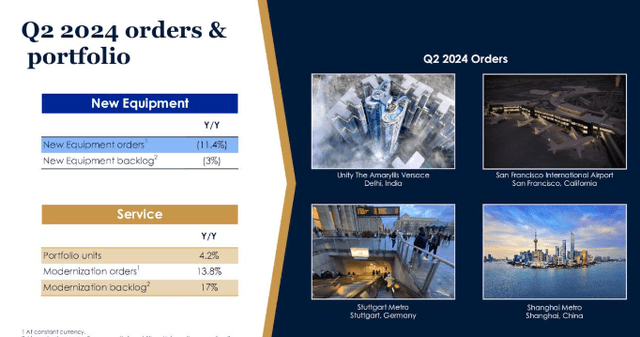

- I’d first comment on backlog coming out of Q2 – it was +17% YoY in Q2 with 420bps growth in maintenance and +14% upside in modernization orders. It has a pipeline of 12 SkyRise in Delhi and is tendering the expansion of Terminal 3 West at San Francisco International Airport. It has 8 escalators in works for the City of Stuttgart [replacing escalators], notwithstanding the China runway mentioned earlier.

- Q2 sales were $3.6Bn on -100bps organic growth and ~$15mm FX headwind. New equipment orders were down 11% YoY, but service revenues were +300bps. This is a testament to the razor/razor blade model – the razor was down YoY, but the blades build a tail of recurring revenues to offset downsides.

Figure 2.

OTIS Q2 investor presentation

-

- Payoffs from its “UpLift” restructuring are working into the P&L – operating margins decompressed by ~110bps driving earnings growth of +15% [the 4th consecutive quarter +10% growth]. Management calls for FY’24 sales of $14.3–$14.5Bn, and eyes $135–$175mm operating earnings on this.

Additional economic characteristics:

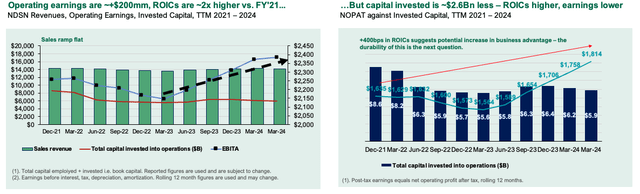

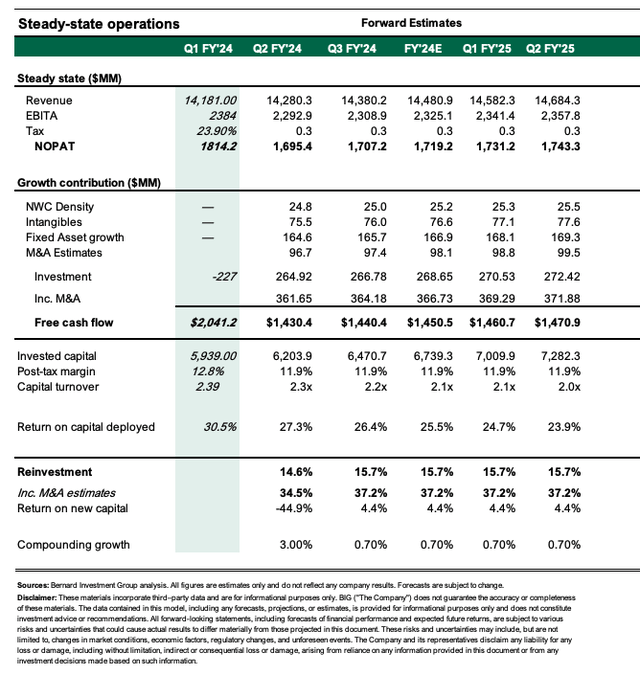

- OTIS is drowning in cash as 1) ROICs are tremendously high, 2) reinvestment requirements to maintain its competitive position or grow are low, and 3) it throws of ~$2Bn in freely available cash every rolling 12mo. ROICs are >30% and up from 19% in FY’21 [I’ve made some adjustments to capitalize expensed intangibles + non-operating assets to arrive at this figure]. But the high + expanding ROICs are from shedding capital via 1) divestitures, 2) working capital work-thrus, and 3) dividends + buybacks. It’s not a mitigating factor, but it has to be explained to illustrate it’s not such an anomaly. The business is strong, but not that strong.

Figure 3.

Company filings

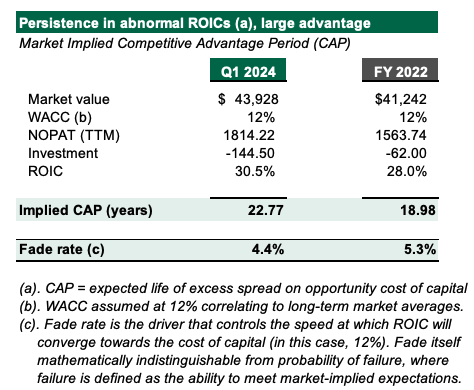

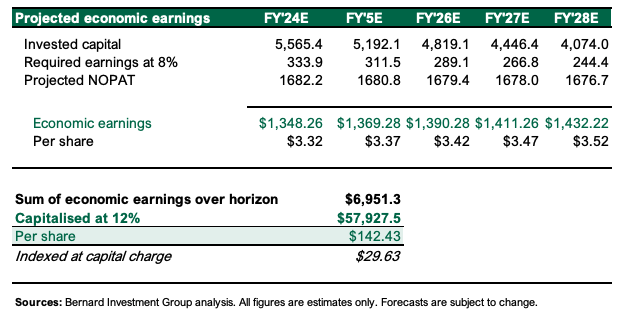

- Nevertheless the implied competitive advantage period is extensive – at 22 years based on my estimates (Figure 4). This is the expected life of excess business returns above our 12% hurdle rate, which represents the appropriate opportunity cost of not holding the benchmark indices. My view is OTIS’ market position, its asset-light operating model (most capital is tied up in NWC), and propensity to methodically rotate earnings into FCF [i.e., produce cash] mean its high ROICs will fade ~4% to our hurdle rate. These are a statistical anomaly to base rates of fade usually seen in the industrial sector [usually fades of up to 60% are observed]. I can’t stress how much of a competitive advantage this is for OTIS. But it squares off with the economics of the business. It is by and large the largest lift + escalator company in the world. Its market share is enormous, and it enjoys both consumer advantages [due to its brand, customer networks, reputation etc] thus enjoys high margins, but also enjoys pricing advantages due to economics of scale and economies of scope in elevators/escalators as a segment.

Figure 4.

Company filings, author

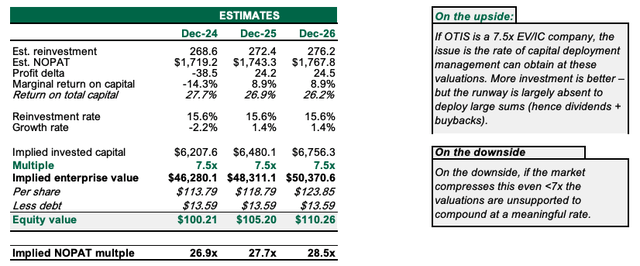

Mixed view on valuation

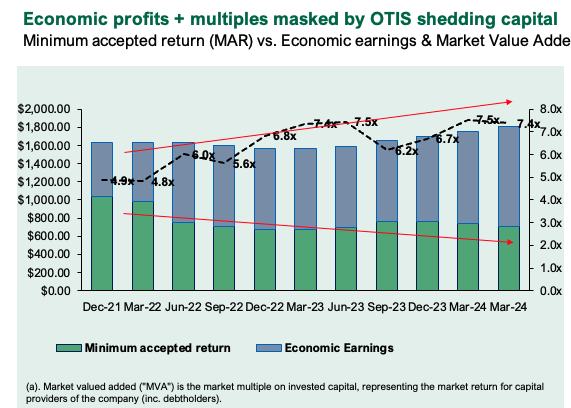

The business valuation is highly sensitive to changes in economic earnings (all those above a hurdle rate). As OTIS has shed ~$2.6Bn in capital to grow earnings by ~$200mm since FY’21, investors have lifted the valuation to ~7.x EV/IC as I write. I can’t say this is unfair – any business producing >2x our hurdle rate should be valued at high multiples on capital. The market expects ~$38Bn in economic profit from OTIS’ enterprise at current valuations, but my estimates suggest it can produce this. My dilemma is how to value the cash flows. If they are to be returned to us (which they will be) then they are less valuable if retained + reinvested by OTIS at its mouth-watering rates of return in my view. We incur a tax burden and opportunity cost in this scenario.

Figure 5.

Company filings, author

Valuation insights

- If OTIS is a 7.5x EV/IC company, the issue is the rate of capital deployment management can obtain at these valuations. More investment is better – but the runway is largely absent to deploy large sums (hence dividends + buybacks). Again, this isn’t a mitigating factor, but you have to be honest with yourself why you’d own this name – it is drowning in cash, but that cash will likely be returned to you to reinvest at appropriate rates, also creating a tax burden to the investor.

- Recall the major benefit of equity markets is the ability to build earnings power through management’s retaining + reinvesting of earnings. Companies retaining earnings and reinvesting these at high rates of return to compound the capital base (to then produce more earnings) is the marvel of the market. These earnings aren’t realized on our income statements; rather, they are fed into our net worth as they make their way onto our balance sheets (via the capitalized earnings / discounted cash flows of our company’s stock prices).

- Theory aside, OTIS is a tremendously high-quality franchise – but to use Boston Consulting Group’s nomenclature it is a “cash cow” (high ROIC, high FCF company with little growth), and not a “star” (high ROIC, high FCF company with substantial reinvestment runway to compound capital + earnings power).

- On the downside, if the market compresses this even <7x the valuations are unsupported to compound at a meaningful rate.

Figure 6.

Author

- The discounted value of cash that can be stripped out of OTIS on my FY’24–’26E estimates is tremendously valuable in my opinion [see: Appendix 1]. The caveat most of it will be returned to shareholders in dividends + buybacks. There’s no issue with this at all. But it must be therefore adjusted for tax, and, I want my businesses to retain cash flows on my behalf and plough them back into their operations to grow the intrinsic worth of the business. Alas, if ROICs are $0.30 on the dollar, likely none of this will be put back to work in the business (in Q2 for instance, it produced $350mm FCF and paid $300mm to shareholders). How can the business expand its corporate valuation this way?

- Hence whilst OTIS is drowning in cash my view is the multiple on this cash isn’t worth >$1 in the market if it’s not reinvested at OTIS’ mouth-watering business returns, and instead subject to a tax burden and opportunity cost in the investor’s hands. Alas, I’m torn on this one and torn isn’t a conviction, so I am trigger-ready on this name from the sidelines with a hold rating.

Figure 7.

Author estimates

Risks to thesis

The major upside risk to the thesis is that investors continue expanding the multiple on invested capital >7.5x. Alas, if OTIS does start reinvesting surplus cash flows heavily, my view is this will see the valuation trade well north of $120/share. There is no evidence of this occurrence just yet, though.

On the downside, the risk is in the contraction of multiples to long-term range. This reduces the investment return sharply. I assign a weak probability of ~25% to this given the strength of the business unit underneath the current valuation.

In short

There are plenty of companies that trade on exceptionally high multiples on capital with similarly attractive economics as OTIS. They are, like OTIS, highly valuable franchises given the amount of free cash they throw off each period. This is absolutely terrific for selective income-based strategies. But for long-term compounding, the business has to be able to throw those cash flows back into the business and grow the enterprise to produce more earnings power. As such, OTIS is a hold in my opinion as I view more selective opportunities to compound their capital elsewhere. I don’t want to have to reinvest a business’s cash flows myself if they are this high. I will stress that I am torn on this decision, adding to the rating of a hold. Looking forward to further coverage.

Appendix 1.

Author

Read the full article here