Dear readers/followers,

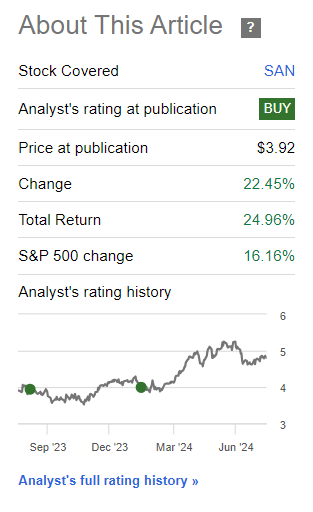

Many analysts and investors were dubious of my over 2-year endorsement and recommendation/rating of Santander (NYSE:SAN) as an investment. I say value, if invested in properly, comes to those who wait – and indeed, that is what I believe that we are seeing here. The company is now showing S&P500-beating averages and trends, and my position in this bank is now not only firmly in the green but outperforming overall. The company’s trajectory is expected to be positive, supported by improved fundamentals and earnings growth.

Despite risks from exposure to Latin America and emerging market currency, I considered Santander priced attractively and considered it a “BUY” in my last article. Even with the recent decline, the company is still outperforming, and it goes to show you that it’s all about that valuation when you invest in a stock.

Seeking Alpha Santander RoR (Seeking Alpha Santander RoR)

You can find my article on this excellent stock (my last one) here, and now I’m going to update for 1Q24 and look at what could happen for 2Q24 and the rest of the year – as well as the next few years.

Is this bank the most fundamentally safe financial play on earth? No, certainly not. That’s why this bank investment is still only about half the size of my other financial investments, and why I’m typically pretty slow adding to it. But my slow sizing, and only at good pricing, is definitely showing alpha here.

Returns for Santander – An attractively-valued bank

It makes perhaps the most sense to put Santander in the context of the other banks. We have new results for Santander in a few days, so this article will serve as an earnings preview for the bank, and where I expect the bank to go, looking forward, to 6 months since my last piece.

Santander is following its strategy to turn around its operations to better profitability, and I would argue that as of 1Q24, this is working out very well.

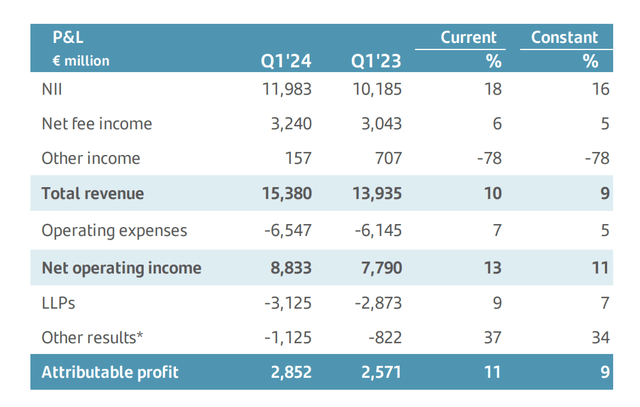

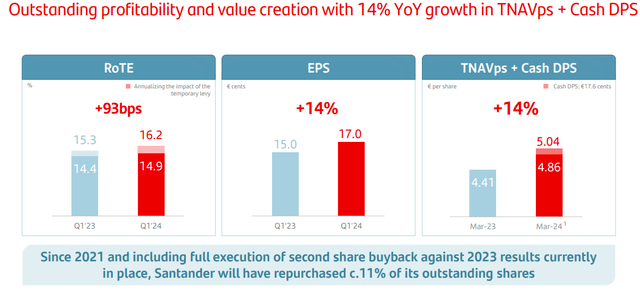

I’m talking about strong operating performance in 1Q, with operating profit showing growth, revenue showing growth, RoTE increasing, CET-1 ratio at 12.3% (Significantly below Scandinavian peers, but that’s why we size conservatively here), and a solid increase in the company’s payouts. The company has improved balance sheet quality and managed to add over 5 million new customers YoY, with good overall activity levels.

It takes time to turn around a bank that hasn’t done all that well since the GFC – and this is after all what Santander is.

Santander IR (Santander IR)

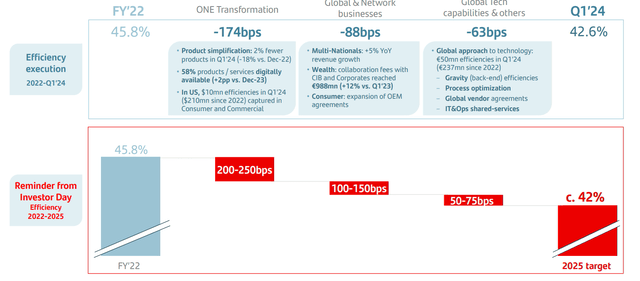

But the P&Ls for 1Q24 and other KPIs show that this turnaround and these positives are indeed now coming in. In fact, the 1Q24 results put the bank on track to meet 2024E targets, with an efficiency of sub-43% (lower is better), and a CET-1 of over 12%, which is already managed. The ROTE is also above target, once you annualized some one-off impacts.

This is where the company’s so-called “one transformation” comes in.

Santander IR (Santander IR)

What encourages me here is the consistent execution of targets for the past 2-3 years. It’s in this manner you can follow a company turnaround, and make sure it’s going according to plan. If that plan can be considered attractive, there is little reason why valuation, if the valuation was low, shouldn’t improve.

And it has.

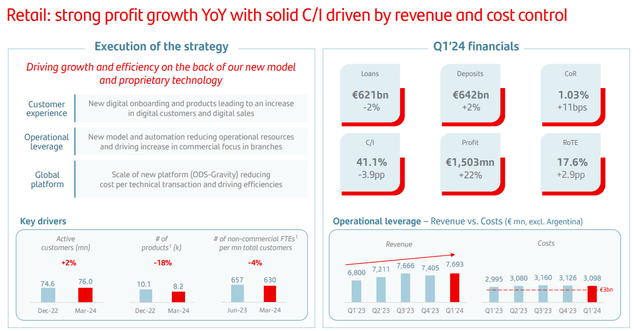

Santander is one of the appealingly-mixed exposure banks towards SA and Southern Europe in all of Europe. Its various segments, including Retail, Consumer, CIB, Wealth, and Payments, mean that it offers full-service coverage and the 52% revenue contribution from Retail is an attractive thing. It also has some very profitable segments (Wealth for One, ROTE of 80.4%), which are set to grow further.

But retail is the first one we want to make sure is working well to ensure solid continuation – and it is.

Santander IR (Santander IR)

The company wealth segment is seeing double-digit growth across its businesses, with very good commercial activity. It was named the best private bank in all of LATAM, and saw 13% YoY growth in the customer base, with a net new money rate of €5.5B for the quarter, and sales of €3.8B. AUM is growing double digits, and fees are growing double digits as well – everything is growing double digits here, which leads me to believe that Wealth and private banking for Santander is only in its inception at this time.

Santander, for 1Q24, simply outperformed.

Santander IR (Santander IR)

And as you can see, the company will have bought back over 1/10th of its shares outstanding by the time current share buybacks are finished. Stable high interest rates also mean stable and high net interest incomes, and a Net interest margin improvement of over 30 bps, which for a bank this size in the billions, is very significant.

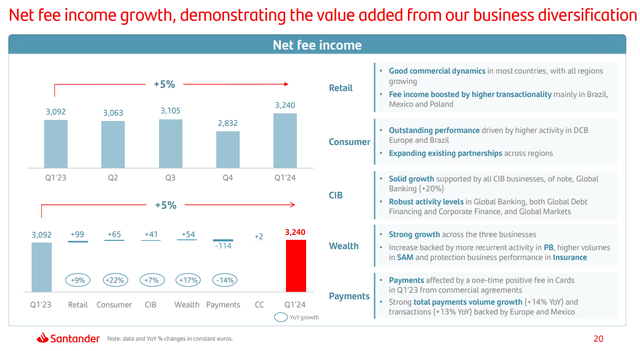

The fact that fee income is growing on a net basis as well shows us that the company is adding value here.

Santander IR (Santander IR)

The company is now A+ rated, but unfortunately also remains one of the lowest-yielding banks in the European space, but also one with a market cap of almost €70B, and a TEV of over €500B. However, due to the yield and the history, I remain only partially invested in Santander at this time.

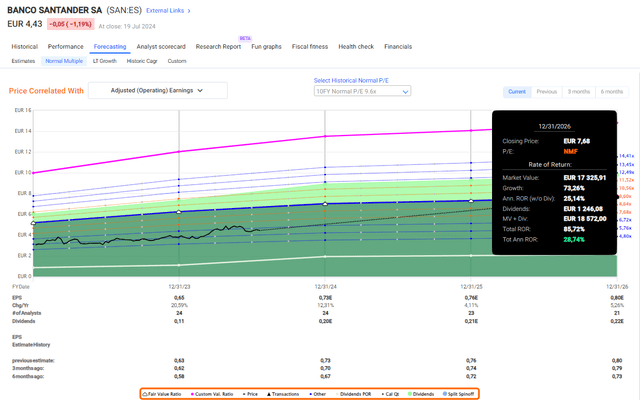

Still, for the past few years, I have clearly stated and supported the company as a “BUY”-worthy bank, with significant upside – and this has now in part materialized. Going forward, we should look at the valuation and upside potential, if we assume that 2Q24 continues on the trajectory of double-digit growth. This is the current estimate by analysts, which gives the company the estimate of growing by 12% this year (Paywalled F.A.S.T Graphs Link)

In terms of the earnings preview, I do not see the bank slowing down here – and I believe that in 2Q24, given current economic trends and growth in the company’s geographies, Santander will continue to grow.

Still, we can look at some risks and upsides that influence the company’s “ups and downs” here.

Ups and downs to Santander – Plenty to consider

There’s no doubt to me that at some point, Santander is going to slow down its growth. The bank won’t be able to keep growing at 5mn customers on a quarterly basis.

But the downsides are more “macro” than this. Santander’s exposure to LATAM is massive. The bank makes 45% of its earnings from Latam, the European operations are actually still somewhat substandard next to the other European banks and other financial majors. LATAM is what drives Santander here. And the key to unlocking even further value and multiples lies in improving US and EU, in my opinion.

Leading the charge in Brazil, Mexico, and Chile, the company has clear exposure to what I would consider being relatively “volatile” overall geographies. Other negative arguments are of course the associated exposure to massive FX – with 70% being non-euro income. Declines here would impact Santander. This brings me to a tendential trend that I can see in the company’s streamlining processes – namely that management seems very reluctant to cut and carve with as sharp a butcher’s knife as they might need to. In other words, they seem attached to some of the businesses. This is currently being obscured by excellent performance, but I’d like to see more focus on the underperforming parts of the portfolio and attacking them more sharply.

But really, anyone asking risks about of Santander can be answered with “South America/Latin America”.

Upsides are just as clear – because they are the same. LATAM and SA are regions of significant growth potential compared to Europe. That’s why I am not only investing in LATAM and SA but in Africa and parts of Asia. This is where I currently see massive growth potential. The company’s focus on retail and diversification of geography gives, even in this risky region, greater visibility and stability to earnings and trends. Unless something major happened across the entire region, Santander would be able to absorb it.

Also, if streamlined properly, it’s my view that Santander should trade at least at twice at what it’s currently trading at.

That’s the case I make for the company, and putting my earnings preview into context for 2Q24.

Let’s look at valuation.

Santander Valuation – Still an upside, but far smaller than before.

Santander now trades at a multiple of 6.4x to P/E. This is still below its 5-year average, as well as the 20-year and 10-year averages – because the 20-year average goes to almost 11x. So when I say it could double, that’s not just “hot air” – because we’ve been there before in terms of multiples.

From a peer perspective, the company still is one of the cheapest banks available in this context. P/S, P/B and other multiples still show discounts to comps, which include companies like HSBC and Banco Bilbao (BBVA). Granted, all of these are better in terms of yield – but Santander has a yield upside. It’s expected to grow to €0.2/share for the next year, which implies almost 5% for the native here, which is much more palatable when you also take the capital appreciation upside into consideration. I consider a 10-year average to be valid for Santander, which puts my upside potential as follows.

F.A.S.T graphs Santander Upside (F.A.S.T graphs Santander Upside)

As usual, I invest native wherever possible, including here. In my last article, I gave a $4.2/share for the ADR – I’m now upping this for the materialization of the company’s ONE program, and upside to at least $5.5/share – but more is possible. Conservatively speaking, I still see a double-digit upside, but it’s now very close to no longer being at 15% – currently at 15.2% per year until 2026E.

That means, that fairly soon, once the bank hits above $5/share, you need to consider a higher premium or different P/E average as opposed to the 5-year average of 7.18 – which is where I have made most of my money from this company, by estimating against a very “low bar”.

Profit drivers for this bank would be the bank’s tangible book value and its development. Depending on how you expect this to evolve, and what multiple you would assign (I say 1x), the company could be anywhere from $5-$7 for the ADR.

I would also say that we’re seeing a slowdown of profit growth in 2025-2026E, and it might start as early as 2024E, but which will be offset by the company’s planned share buybacks.

For now, I continue to say that Santander is a “BUY” – but with a much slimmer upside than before, because there are many attractive banks out there.

The following thesis is relevant here.

Thesis

- Santander is one of the better banks found in the Southern European area and geography. It has significant emerging market exposure, which gives it a heightened risk profile in context to other banks – but it’s also immensely qualitative, as evidenced by how it has survived previous downturns.

- I consider Santander a “Buy” at cheap valuations, and I believe this bank can deliver significant upside over time – and now is one of those times.

- I believe the company’s thesis and potential have improved since my last article, and I continue to add shares, albeit at a lower rate than some other banks.

- I remain for Santander at a PT of $4.2/share, a share price upgrade, and give it a “Buy”.

- This thesis has been updated for 2024, and I remain positive here.

Remember, I’m all about:

-

Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansions/reversions.

Despite a 7% RoR since my last article, I consider the company fulfilling all of my criteria except being cheap – it’s still attractive here.

Read the full article here