Thesis

P3 Health Partners Inc. (NASDAQ:PIII) is operating in the healthcare space, where they are collaborating with healthcare providers in different states in five states, providing them with assistance for a compensation.

P3’s revenue has been growing steadily over the past years from $452 million to $1.5 billion, but so far, has not been profitable. Profitability in 2024 is however on the doorstep in light of the company’s guidance, and once profitable, I believe the company’s valuation should start to look entirely different. Probably for that reason, P3’s valuation grade according to all of Seeking Alpha’s metrics is A+. With an EV/Sales value of 0.31, I believe P3 is strongly undervalued.

The recent announcement of a new CEO may bring renewed attention to the stock.

As the company progresses towards its guided goal of profitability, I am rating the company as a Buy.

Company

Introduction

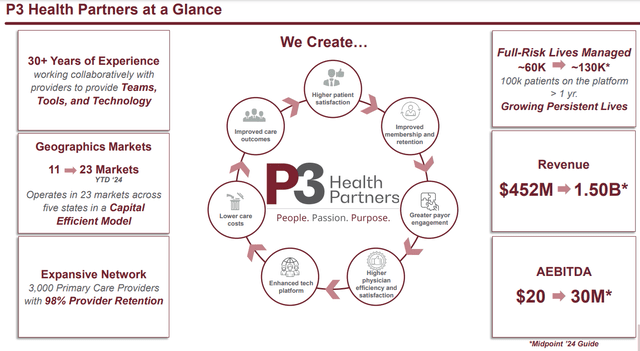

P3 operates in the healthcare service, where it works with healthcare operates as its members with the goal to create added value. P3 has a team of doctors and healthcare providers with a variety of healthcare management services, such as education to patients and doctors, patient management, proactive screening, and access to resources.

P3 at a glance slide (Recent Jefferies presentation) Growth profile (Recent Needham presentation)

P3 has a network of care providers across the country, who manage the care of thousands of patients, by providing coordination and administrative services that lead to better patient outcomes and lower costs, taking care of patient care, hospital visits and related services. P3 uses local physicians to provide these services in part. P3 charges a per member, per month fee [PMPM] and Medicare providers earn a percentage of money not spent taking care of members and an additional bonus.

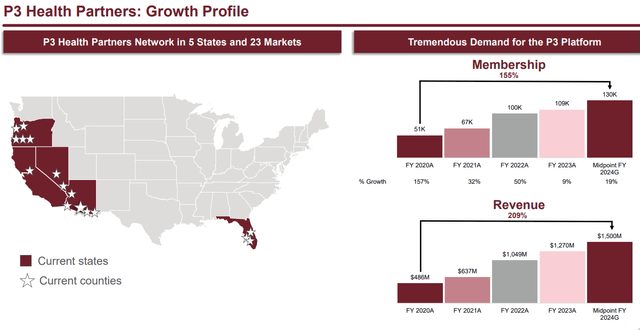

P3 is active in five states and 23 markets.

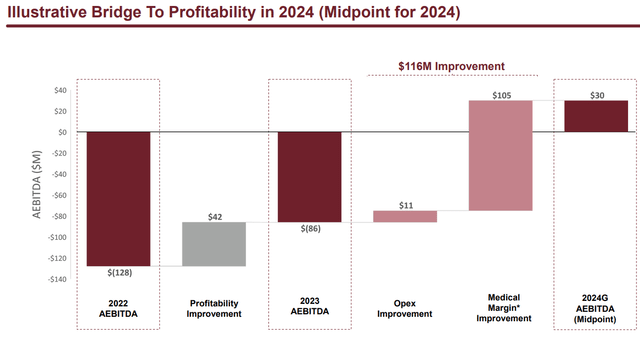

Path to profitability in 2024

P3 currently has a market capitalization of $183 million, which is in drastic disproportion to its latest quarterly revenue of $388.5 million and expected yearly revenue of between $1.45 and $1.55 billion. Moreover, that revenue keeps on growing year over year, while the share price keeps on dropping, adding to the disproportion.

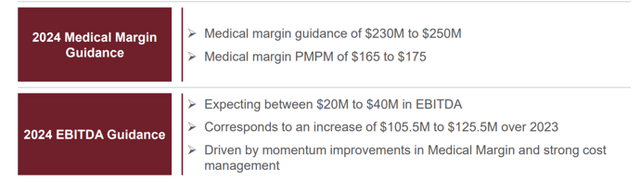

One could argue that perhaps a low valuation is in place because the company will never be able to turn profitable. That arguments fail in light of the repeated guidance of the company that the year 2024 will be profitable, with an estimated EBITDA profit margin of $20 to $40 million. While the company usually does not provide guidance as to potential profits, the fact that it does is an indicator that prospects are good. If that trend would continue, then in the course of the coming years that profit margin could quickly grow. There is ample room, as $20 to $40 million represents only a fraction of the company’s projected revenue of $1.5 billion, which is expected to keep on increasing year over year.

Medical Margin and EBITDA guidance (Recent Needham presentation)

P3 reaffirmed guidance to profitability in the Q4 2023 earnings call and did so again when issuing the Q1 2024 results.

Factors underlying the path to profitability

Several elements are playing in favor of P3’s guidance here, some of which I will mention below. Over the past five years, while memberships have increased by 155%, revenue has grown by 209%. As revenue is expected to reach between $1.45 and $1.55 billion at the end of 2024, that would correspond to approximately 14% to 19% of growth over 2023.

As annual membership enrollment numbers keep on improving, P3 also keeps on expanding to new territories. Currently, the company is working in 25 countries, two extra compared to the start of 2024.

Revenue growth is also consistent each year. In 2023, total revenue growth compared to the year before was 21%. For the first quarter of 2024, revenue growth compared to the first quarter of 2023 was 29%.

Existing members keep paying more, namely 16% compared to the year before in 2023, in spite of declines in reimbursement.

P3 has made some cost reductions and other operational efficiency enhancements, such as the reduction of its platform expense by 32% in 2023.

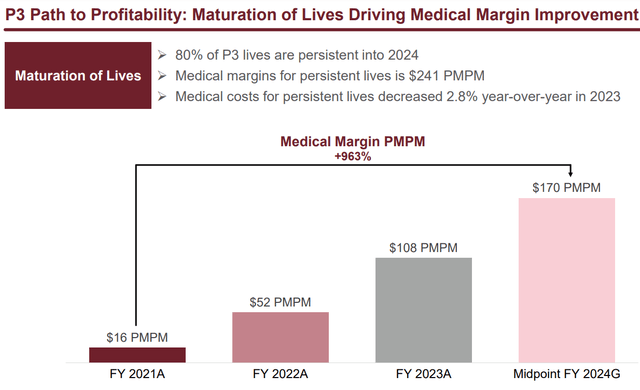

Additionally, P3 expects the maturation of lives to drive an improvement in medical margins.

Maturation of Lives slide (Recent Needham presentation)

Latest quarterly results

The first quarter of each year is generally not the big contributor to annual revenue.

However, in its latest first quarter 2024 quarterly results, P3 noted a total revenue growth of 29% year-over-year. Total revenue for the quarter was $388.5 million, an increase of 29% compared to $302.1 million in the first quarter of the prior year.

Net loss and adjusted EBITDA loss were similar year over year, but as revenue increased by 29% compared to the year before, the net and EBITDA losses are actually an improvement compared to the year before, or a relative reduction of about 30% compared to the year before.

The net loss was $49.6 million, compared to a net loss of $52.4 million in the first quarter of the prior year. Adjusted EBITDA loss was $19.8 million, compared to an adjusted EBITDA loss of $19.1 million in the first quarter of the prior year.

That relative annual decrease in losses as a function of total revenue was probably due to several reasons, such as a 26% reduction of operating expenses to $26.2 million for the first quarter of 2024, a 12% reduction in medical expenses, and a 12% reduction in corporate, general and administrative expenses. If these operational efficiencies continue, I believe the guidance of the company could turn out to be correct. Additionally, P3 expects to potentially see a significant reserve release, as the 2023 claims showed a trend to a strong improvement from what had been previously booked.

P3’s guidance for profitability in 2024 is between $20 to $40 on an adjusted EBITDA basis.

Bridge to profitability slide (Needham presentation)

In my eyes, neither the company’s expected revenue of $1.5 billion nor its projected trajectory warrants a market capitalization below $200 million.

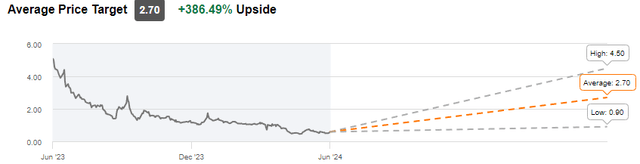

The average Wall Street analyst price target is 386% higher than the current valuation.

Wall Street analyst average target (Seeking Alpha)

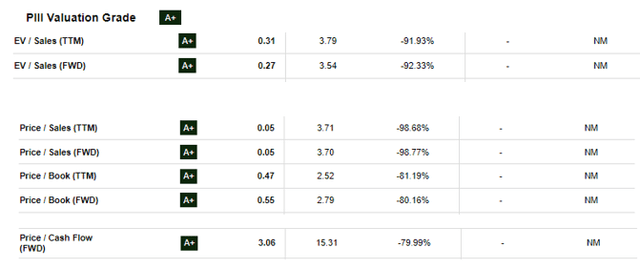

Seeking Alpha’s valuation grade on PIII is A+. In fact, all available metrics are A+.

Valuation Grade metrics (Seeking Alpha)

Lacking profitability, I would primarily look at this company from an EV/sales ratio. For PIII, that value is around 0.3, whereas companies generally trade around EV/sales ratios of 1 to 3. The company appears drastically undervalued from that perspective, certainly in light of its guidance.

New CEO on board

In May 2024, P3 announced that Aric Hoffmann would join P3 as the new CEO, while the former CEO would stay on as an adviser and member of the Board of Directors. Mr. Hoffmann knows the team of P3 well, as he has worked for the company in the past, prior to transitioning to serve as the CEO of the Everett Clinic and Northwest Physicians Network.

His return to a company and people he already knows, with greater experience as a CEO, may bring added value and a new wind to the company. This may also be good news for investors, allowing the company to turn a page.

Finances

According to P3’s latest quarterly results, the company had approximately $32 million in cash and received approximately $15 million in regular cash-capitated premiums and an additional $15 million of capital at the start of the second quarter.

The company has recently also picked up approximately $42 million from a private placement at $0.62 cents. In total, that should lead to about $100 million in cash, which may be sufficient if the company indeed turns profitable.

The recent financing, at a price higher than the current price, reduces the risk of further financing.

Moreover, last year’s financing was also a private placement at a price of $1.12, so I assume investors of that financing will be reluctant to sell at the current prices.

Finally, the short interest in PIII is about 7% with about 18 days to cover at the current volume.

Risks

Investing in a company that does not generate revenue yet is risky. The company may need further financing, thereby diluting the current shareholders and increasing market capitalization. I believe that risk, for now, is limited in light of the recent financing.

The thesis of profitability as projected by the company may be impacted by regulatory or macroeconomic factors, may simply appear erroneous, or the company may take longer to reach that pivotal point. A positive market reaction in case of profitability is not guaranteed.

P3’s price is below the dollar at the moment, meaning it is not in compliance with Nasdaq requirements. If this situation continues, P3 may eventually have to take measures to ensure compliance, such as a reverse stock split.

Finally, though its revenue is high, PIII’s valuation is low, making it qualify as a microcap. Investing in microcap stocks is always risky.

Conclusion

P3 is a player in the healthcare business with a growing business on its way to profitability.

With recent financing closed, I believe now may be an appropriate time to look at potentially investing in P3 Health Partners. P3’s revenues have kept on growing over the past years, and the guidance is that revenue will end up between $1.45 and $1.55 billion this year. That revenue is in stark contrast with the market cap of the company, which is below $200 million. It is also in contrast with the EV/sales ratio of about 0.3, which is in contrast with EV/sales ratios which are typically between 1 and 3. The average Wall Street analyst price target shows a 386% upside.

PIII’s cost structure has recently been made more lenient over the past quarter.

For the above reasons and because the company believes 2024 to be transformational, I believe now is a good time to cover PIII with a Buy rating.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here