Introduction and Earnings

As many of you are aware Palantir (NYSE:PLTR) is a serious battleground stock with both bulls and bears making solid points regarding the valuation of PLTR stock. Palantir’s earnings were in-line with expectations, while market makers initially expected a volatile swing in the stock price.

Due to the recent explosive stock price rise, with Palantir being up over 137% since May, many people were of the opinion that PLTR had to report extraordinary earnings to not make the stock fall by over 10%. That said, the stock is now up 3% after hours after earnings came in line of expectations, but with the company raising full-year guidance.

Furthermore, the company is on pace for S&P inclusion in Q3, with PLTR now being one quarter away from GAAP profitability. In addition, management has guided that they fully expect to be eligible for inclusion by EOY. To be completely honest, I don’t know what to think about the $1B authorized buyback.

Apparently, some people do not completely understand what this means. This means that the company can do $1B in buybacks whenever they see fit. This doesn’t mean that they have to do it right now, if the stock would drop significantly, that’s probably when they will decide to start being back shares.

In addition, share buybacks are loved by Wall Street and this makes investors believe that the stock is cheap at the current level, due to the company indicating that they are willing to buy in case the shares drop. Given the significant SBC dilution PLTR is notorious for, it is good to see that they will be able to somewhat offset this with the authorized buyback.

Nonetheless, PLTR might have been better off using this money elsewhere to grow its business. As PLTR is still considered a growth company, it is quite odd that they decide to buy back shares. This could indicate that they don’t see any opportunities to deploy capital in operations or new business. This could be seen as very bullish, as this could indicate that the company believes it is currently undervalued. But, why did they not do this earlier? As such, it is likely a move to please investors and Wall Street.

Alex Karp, the CEO of Palantir, is very good at talking to investors and is obviously a huge part of why the company is at the place it is today. Some interesting quotes from the earnings call of today were the following. “The scale of the opportunity that lies ahead has increased significantly in recent months. And we intend to capture it.” This could be one of the reasons why they initiated the authorized buyback as they see tremendous opportunity in the next few months.

In addition, Karp mentioned that “The demand for AIP is unlike anything we have seen in the past twenty years.” This would obviously be very bullish for investors as well, if PLTR is able to generate substantial free cash flow of this down the line.

Palantir And Its Billionaire Founder

Palantir Technologies was established in 2003 by Peter Thiel, who named the company after the seeing stones (Palantiri) from Lord of the Rings. The Palantiri was used in the movies for communication and intelligence gathering throughout Middle Earth amid continuous war. It is easy to see the parallels between the fictional Palantiri and the real-world Palantir, which can be an effective tool in warfare just like its fictional counterpart.

PLTR gained immense popularity after going public but crashed more than 85% from its all-time high in January 2021 to its all-time low in December 2022. PLTR’s saving grace might’ve been the popularity of ChatGPT, which showed the world the power of AI which PLTR’s products are built upon. In this article, we will explore how the recent revolution within the world of AI has given PLTR a breath of fresh air, how PLTR can function in the new age of warfare, and their financials.

AI Has Given PLTR Its Relevancy Back

PLTR’s quest for contentment amid global instability in the US tech sector draws attention. As AI emerges, PLTR stands out with its negative comments about potential crises. The idea that AI could lead to a dystopian future, just like Robert Oppenheimer’s moment with the atomic bomb, is a talking point that gained much traction with the reveal of ChatGPT.

Although the exact potential of generative AI remains unclear, discussions about its immense power have boosted the value of certain companies. For instance, AI chipmaker Nvidia’s market capitalization briefly surpassed a trillion dollars. Despite declining funding elsewhere, AI startups continue to raise money, and PLTR’s share price has more than tripled in months.

PLTR recently unveiled its new AI platform, capable of generating conversational responses using large language models (LLMs) like those powering chatbots such as ChatGPT. The AIP platform aims to avoid the pitfalls of false responses that plague other chatbots. The tool’s application includes battlefield scenarios, assisting in enemy tank identification, and offering suggestions for targeting.

With the platform’s announcement came a video on its YouTube page showcasing its capabilities. While it is difficult to pinpoint the exact applications of the platform in real-world scenarios, Ukrainian forces have already started using some of its features. The platform has several other uses than data analysis in warfare, and the commercial sector will also reap the benefits from this new platform.

PLTR faces competition from software companies like IBM, which recently announced its AI platform, Watsonx, which focuses more on businesses than government sectors such as the military. In addition, many other big tech companies, such as Microsoft (MSFT) and Alphabet (GOOGL), have released their own AI platform in some capacity. However, no big players have the same military uses as PLTR’s platform, giving PLTR a sizeable edge, for now.

So, where does PLTR stand? Initially, the company was founded to build software for intelligence agencies to combat terrorism, but it has now expanded to serve government departments and businesses.

The company may shift its focus heavily toward government contracts, specifically the defense sector, as they are seeing unprecedented demand for its military AI. The surge of interest in AI has breathed new life into PLTR’s appeal, amplified by its newfound profitability. The prevailing zeitgeist, which aligns with PLTR’s perspective on AI’s potential to steer us toward an uncertain future, only adds to its allure. If AI indeed unfolds in ways that may have profound consequences, PLTR won’t be caught off guard.

The 21st-Century Arms Race Is AI

Since Russia invaded Ukraine, a significant debate has emerged about the nature of the conflict. This surge of interest in AI has also sparked discussions about its potential impact on warfare.

Prominent figures, such as Kai-Fu Lee, CEO of Sinovation Ventures, called AI weapon systems the “third revolution in warfare” in 2021. While the Ukraine conflict has not undergone a complete transformation, it serves as a crucial testing ground for the following form of warfare, which PLTR has been a big part of. Ukraine has become an opportunity to fine-tune and improve AI-enabled systems for immediate deployment. The ongoing efforts in refining AI capabilities pave the way for the future of AI warfare.

More specifically, AI-enhanced autonomous capabilities in drones and loitering munitions have become widespread. AI is crucial in target recognition, geospatial intelligence, and strategic analysis using satellite imagery and open-source data – this is what PLTR’s AIP is capable of. In addition, PLTR has also assisted Ukraine with its systems, providing intelligence and positional advantages.

Despite not fully manifesting the AI-driven revolution, the potential of a truly networked battlefield, where data moves at the speed of light to coordinate military actions, remains a significant consideration. As technological developments progress and concerns about adversaries’ capabilities grow, the idea of AI-driven warfare becomes more real.

PLTR has already shown us the capabilities of its software on its YouTube page, and it seems they are very much ahead of their competition. With that being said, will we see a Cold War-esque type of arms race? Likely not – unlike the nuclear arms race, governments across the globe are already looking into ways to govern this new technology. Still, with PLTR’s expertise in the field, it is difficult to see how they will not be able to benefit from this new type of warfare.

PLTR Has A MOAT Customer Base

According to Statista, PLTR has approximately 367 customers across all its products as of Q4 2022. Some of these names include BP (BP), Hertz (HTZ), Merck (MRK), and many more companies on the commercial side; however, PLTR’s more interesting contracts are with the US government in particular. In our opinion, this is where PLTR will have to focus further in the future.

Palantir.com

Government business serves as a significant and formidable advantage for PLTR. In 2022, PLTR made over $1B from their government contracts, which included analytics and integration solutions. Traditional government and defense contractors like RTX Corporation (RTX), BAE Systems (OTCPK:BAESF), and Booz Allen (BAH) need more technological expertise and scale to compete in this area efficiently, expertise PLTR already possesses.

In addition, PLTR has expanded its services to various government agencies, including the Centers for Disease Control and Prevention (CDC), The Department of Homeland Security (DHS), and The Navy. While new data integrators and analytics players like Snowflake (SNOW), Datadog (DDOG), whom we’ve covered before, and Splunk (SPLK) possess the technology and scale, they are not focused on this specific space and follow a platform-based product/licensing approach, limiting their ability to offer customized solutions.

PLTR’s unique advantage lies in its high-cost Forward Deployed Engineers (FDEs) and representatives, allowing them to provide embedded engineers to existing customers’ software platforms to solve complex challenges. PLTR aspires to serve as the operating system for its clients and has the expertise and resources to excel in this business.

This MOAT will not disappear suddenly, providing PLTR with a significant advantage over its competitors. It should be mentioned that PLTR has said several times that they refuse to do business with countries hostile to US global interests, which somewhat limits their customer base. However, with the sheer size of the US military, contracts should be readily available for PLTR.

Financials

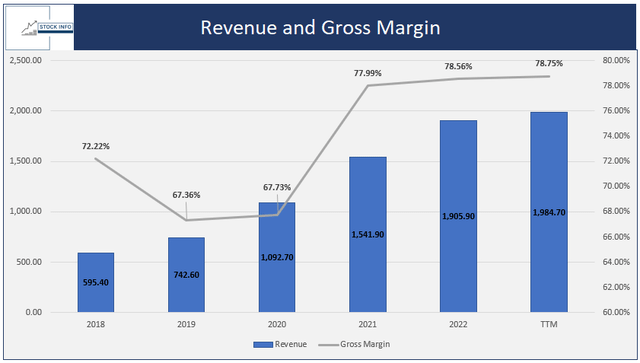

As PLTR has grown its customer base throughout the years, so have its revenues and gross margins. PLTR has experienced remarkable growth and profitability over the past five years. Its revenue has consistently increased from $595.40 million in 2018 to $1,905.90 million in 2022, with TTM revenue reaching $1,984.70 million. The company’s gross profit rose steadily, reaching $1,497.30 million in 2022, and TTM’s gross profit at $1,562.90 million.

Their impressive gross margins, starting at 72.22% in 2018, improved to 78.56% in 2022, with the TTM gross margin at 78.75%. Thus, PLTR has always been able to generate profits from its business, and its consistent growth trajectory indicates they have a strong market presence.

Stock Info with Seeking Alpha Stock Info with Seeking Alpha

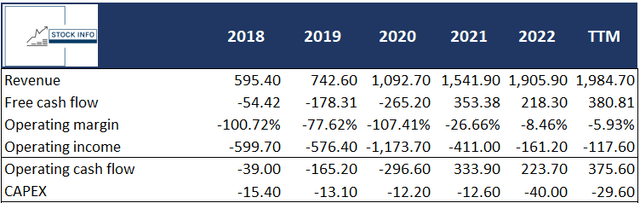

Looking further into their financials, the free cash flow was negative in 2018 and 2019 but turned around in 2021. It came in at $353.38M and improved to $380.81M in TTM. Similarly, the operating margin and operating income were negative from 2018 to 2020, with marked improvements in 2021 and 2022, signaling better cost management and reduced losses.

The operating margin improved to -8.46% in 2022. However, it is still some way from a satisfactory percentage. The operating income was reduced to -$161.20 million, and the operating cash flow improved dramatically in 2021, turning positive at $333.90 million and reaching $375.60 million in the TTM.

The company’s CAPEX remained relatively stable until 2020, but a significant increase in 2022, reaching -$40.00 million, indicated substantial investments for expansion or modernization projects. These changes reflect PLTR’s efforts to enhance its financial health and improve operational efficiency, and hopefully, this will result in a better bottom line shortly.

Stock Info with Seeking Alpha

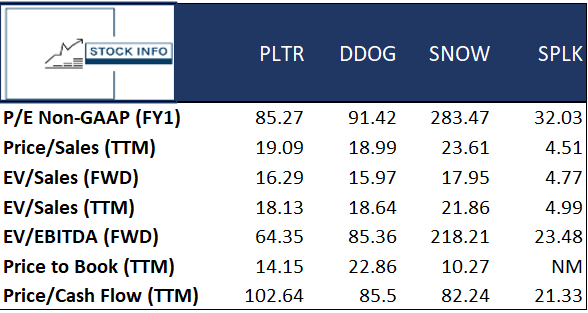

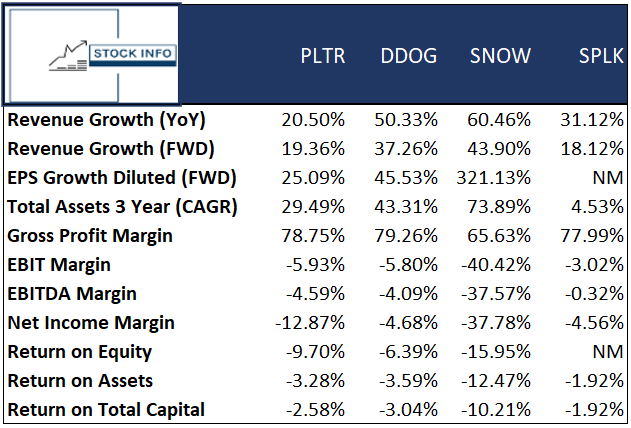

Let’s move on to the valuation metrics between PLTR and its closest competitors. SNOW and DDOG have higher P/E ratios, with SNOW’s P/E ratio being more than three times higher than PLTR’s. In addition, SNOW has a higher valuation when considering EV/sales. Regarding EV/EBITDA ratios, SNOW has a very high ratio again, while PLTR, DDOG, and SPLK show more attractive valuations based on EBITDA.

DDOG exhibits the highest P/B-valuation, with SNOW having the lowest. PLTR has the highest price-to-cash flow ratio. PLTR and DDOG seem moderately valued, while SPLK is a clear outlier with much lower ratios than the rest. While SPLK may seem more attractive based on these ratios, it is essential to remember that PLTR has a competitive advantage.

Stock Info with Seeking Alpha

Among the four companies, SNOW exhibits impressive revenue growth, with the highest YoY growth at 60.46% and a projected FWD growth of 43.90%. DDOG also shows strong revenue growth, with YoY and FWD growth at 50.33% and 37.26%, respectively.

On the other hand, PLTR reports steady revenue growth with YoY and FWD growth at 20.50% and 19.36%, respectively, and a reasonable FWD EPS growth of 25.09%. SPLK demonstrates a balanced performance with solid revenue growth and FWD EPS growth at 31.12% and 18.12%, respectively, and the highest gross profit margin among the group at 78.75%. All companies have negative RoE, RoA, and RoTC; however, they have slightly favorable returns compared to DDOG and SNOW. SPLK’s profitability metrics are relatively better compared to the rest.

Bear Case For Palantir

While the company is going at a steady pace, one could argue that growth isn’t as significant as it should be to justify the pretty steep valuation.

The company has a big vision and if they are able to execute this could multiply the market cap by a lot in the next decade. Nonetheless, with the data that we have now, the company is quite expensive.

Important to mention is that most of the bear arguments are regarding the valuation of the company. While companies that seem expensive are often considered dangerous to invest in, one has to remember that many of the giants today were called “overvalued” 10-20 years ago. Afterward, they rallied 10-20x, could Palantir do the same? Sure, but they will need to execute flawlessly to justify the current price.

A lot of the investment thesis for PLTR relies on the fact that the management will be able to execute and while I believe they might be able to, I wouldn’t invest in it at the current price due to the steep valuation.

As such, it is important for PLTR to accelerate their growth and AI could help them do so. As the stock price has definitely risen due to the AI hype train and the CEO isn’t afraid of mentioning AI quite often during the earnings call. Up to the management to now deliver and execute.

Technical Analysis

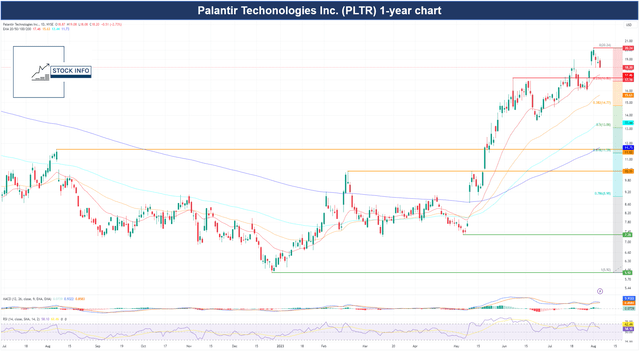

As seen in the chart below, PLTR has been on the rise since the beginning of the year, but especially since May, as the market has opened its eyes to the capabilities of AI technology. The stock recently touched the $20 level after bouncing back to the $ 18 handle. This is also partially due to the recent news of the downgrade. It will be interesting to see whether the stock can regain the $20-handle and continue its uptrend.

The 1-year chart shows that the stock trades above all the included EMA’s on the daily timeframe, indicating an overall bullish sentiment. It is also very noticeable how the 20 EMA provides comfortable support for the stock during its uptrend.

At this point, bulls aim to defend the $17.50 area, where the 20 EMA is currently. This also means the stock has some room to move down toward support. We will likely see a similar pullback scenario to the 20 EMA before the stock moves further up; in this case, we would like to see the stock break $20 – This would clear the path for a potential move toward $30, as we can see on the 3-year chart.

Stock Info with TradingView

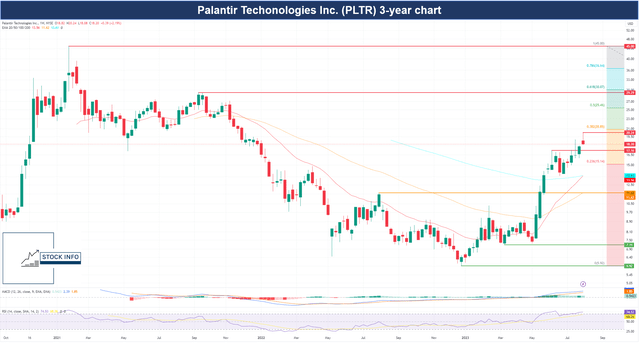

Looking at the weekly chart over a 3-year timeframe, we see the downtrend PLTR was on before finding a bottom at around $6, whereafter the stock found immense momentum.

Currently, the stock is up more than 200% from its lows in late December 2022, and as we mentioned, on its way toward the $30-handle. It should also be noted that the stock trades above all included EMA’s on the weekly chart, which only confirms the overall bullish sentiment.

In addition, the 20 EMA is just about to cross the 200 EMA, which could signal momentum investors to step in and buy. Thus, it is essential to monitor the following few day’s price action for this stock to gain confirmation about the direction this stock is going.

Stock Info with TradingView

Conclusion

PLTR has emerged as a significant player in the AI industry since its establishment in 2003. Despite facing challenges and a drastic stock price crash, PLTR’s popularity resurfaced with the success of ChatGPT, showcasing the power of AI on which its products are built.

The ongoing revolution in AI has revitalized PLTR’s appeal, particularly in the defense sector, where it unveiled its AI platform with applications in intelligence gathering and battlefield scenarios. PLTR’s unique advantage lies in its government contracts and AI expertise, positioning it favorably in the market.

Looking at PLTR’s financials, the company has experienced remarkable growth and profitability over the past five years, demonstrating steady revenue growth and improved gross margins. Although profitability metrics have shown improvement, PLTR continues to work on cost management and operational efficiency to strengthen its financial health further.

Despite competition in the AI market, PLTR’s strong market presence and government contracts make it a compelling player in the AI-driven future of warfare. As the AI revolution continues, PLTR’s position as a leading AI company will undoubtedly play a vital role in shaping the world’s technological landscape.

Nonetheless, the valuation right now seems quite steep and there aren’t many mistakes allowed to justify the current multiples and price. As such, we currently rate the company as a hold. If the shares were trading in the $10-$12 zone right now, I could justify a buy rating. I currently don’t hold any shares as I sold my position, which was a combination of LEAPS and a small share position in July, due to valuation reasons.

Nonetheless, if you believe in the thesis and are willing to hold shares for the long term this could be an enticing opportunity. Nonetheless, I believe there are better opportunities elsewhere at this moment in time.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Best AI Ideas investment competition, which runs through August 15. With cash prizes, this competition — open to all contributors — is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

Read the full article here