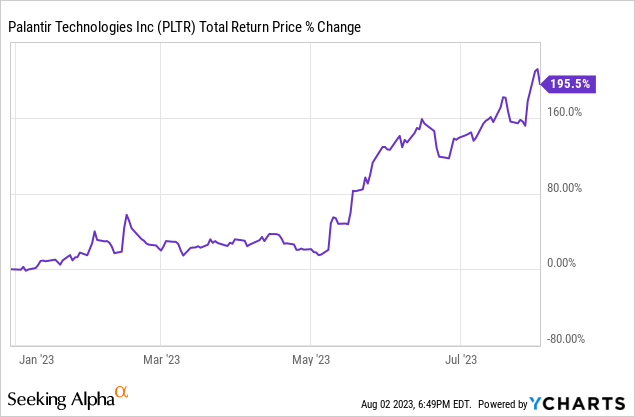

Palantir Technologies stock (NYSE:PLTR) has been on a phenomenal run this year, boosted by the company’s pivot towards sustainable GAAP profitability and the market mania surrounding artificial intelligence.

This run-up has taken us by surprise, given that the stock has continued to soar higher since we last covered the stock. In that article, we rated PLTR a Sell, because – while we believe that the AI wave will contribute to PLTR’s growth – it is unlikely to justify its current valuation. Therefore, it is an extremely speculative buy for investors with only the most optimistic expectations for AI-driven growth for PLTR.

While sentiment seems to be exceptionally strong surrounding PLTR stock and many other artificial intelligence stocks right now, we think that investors would be prudent to lock in gains ahead of next week’s earnings report. We believe that it is important to point out that this upcoming earnings report could very possibly be a negative catalyst for the stock as management will likely need to deliver robust growth results or at least offer more concrete guidance numbers on how artificial intelligence will drive significant growth acceleration for PLTR moving forward. We think this will be very difficult for them to do for the following reasons:

- The growth of the Foundry (commercial) platform will face headwinds from companies that are facing growing pressures to cut costs in the face of a tight labor market, persistent core inflation, and a slowing economy

- The growth of the Gotham (government) platform will be difficult to forecast over a short time frame as management has previously stated that government spending on PLTR’s products is very lumpy with unpredictable timing due to the budget-setting and contract awarding process in government agencies.

With this potential upcoming negative catalyst in mind, here are three reasons why we think this earnings report will be disappointing:

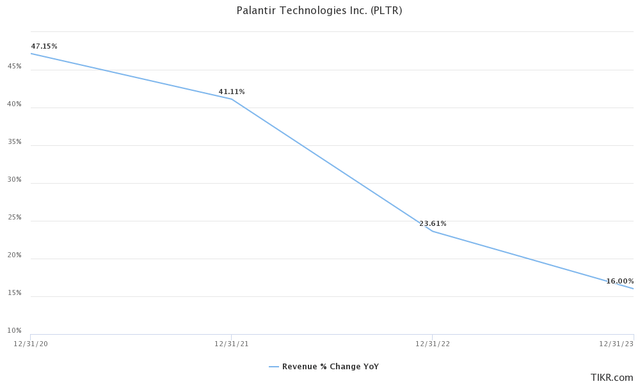

#1. PLTR’s Growth Rate Has Been Decelerating

The biggest reason to be pessimistic of PLTR going into Q2 earnings is that – while the stock price and the hype surrounding the company’s artificial intelligence capabilities seems to be pointing towards rapid growth moving forward – revenues have actually been decelerating. This point is largely reflective of the point we just made about management likely being unable to give the market clear guidance on how artificial intelligence will re-accelerate their revenue growth in the near future.

As the chart below illustrates, since the company went public, its revenue growth rate has declined every single year, with particularly precipitous declines felt in 2022:

PLTR Revenue Growth Rates (TIKR.com)

This dramatic deceleration of growth has prompted management to drop all talk of its original guidance for $4 billion plus in 2025 revenue. Instead, Wall Street analyst consensus is forecasting less than $3.2 billion in 2025 revenue despite still predicting that revenue growth will reaccelerate in 2024 and 2025.

While management is certainly making every effort to hype up its artificial intelligence credentials and capabilities, it is yet to be determined just how much of a boost this will provide to growth. Yes, management has provided anecdotes about a spike in artificial intelligence related growth, stating in a recent interview:

Our customer base is large and – usually we have to go to find people – now we have customers, especially the U.S., just calling us everyday…we have been getting the number of inbound calls that we usually get in a year, in like a month. Then when we are at a conference, there are customers showing potential customers how to use our products.

However, it has yet to quantify what this growth looks like on the cash flow statement. If artificial intelligence was truly such a powerful growth tailwind, why hasn’t management provided any updates on its short to medium term revenue growth outlook? Perhaps this will come out on the Q2 earnings call, but until they release this outlook, buying PLTR stock at lofty prices based on the assumption that as-of-yet unquantified growth will come pouring in is a highly speculative investment.

On top of that, PLTR has even admitted that its international business is struggling mightily:

We have America, which is growing around 28%, it is now 64% of our business. Four years ago it was 37% of our business. We are absolutely disrupting in the U.S. of A. International is growing around 10% and that is becoming obviously a smaller part of our business.

However, while management claims that the international business – which still occupies a substantial 36% of the business – is growing at around 10%, in Q1 the international commercial business shrank by 7% sequentially and the international government business saw its revenue decline by a whopping 13% sequentially. With over one third of the business struggling to grow, the headline revenue growth rate decelerating for several years running now, management apparently abandoning previous 2025 revenue guidance, and no quantifiable data being provided on what sort of growth tailwind will come from PLTR’s artificial intelligence platform, PLTR looks like its valuation is standing on very shaky ground heading into Q2 earnings.

This likely disconnect between management hype/market sentiment and the disappointing reality of the fundamentals was highlighted in a recent investor note by Monness, Crespi, Hardt’s analyst Brian White, who stated:

We believe the near-term fundamental realities by those promulgating the AI dream will fail to satisfy the market’s voracious appetite.

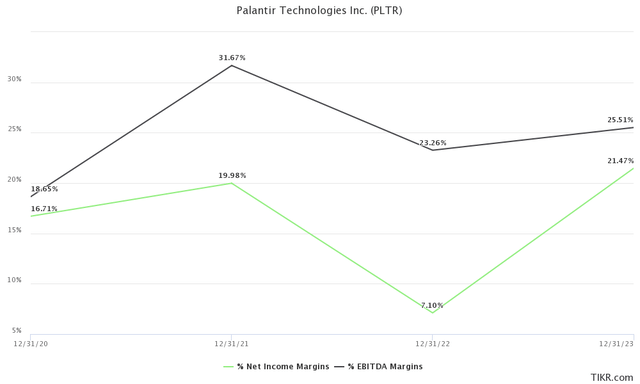

#2. PLTR Has Yet To Develop Significant Economies Of Scale

Another reason to remain highly skeptical of PLTR’s long-term value proposition at its current valuation is that it has struggled to develop significant economies of scale over time. We do not expect Q2 to change this narrative given that their business model has not fundamentally changed and likely will not for some time, if ever.

As the chart below illustrates, PLTR has had pretty choppy EBITDA and net income margins since going public in 2020 despite its revenue more than doubling over that period and the company placing an increased emphasis on profitability:

PLTR Profit Margins (TIKR.com)

What that tells me is that PLTR is struggling to unlock meaningful economies of scale. If PLTR were a true software company, it would be seeing its profit margins expand rapidly with scale as once the software is developed, the business becomes extremely capital light and cash generative.

This has led many to question whether or not PLTR is truly a software company and instead view it as more of a hybrid software-consulting firm. While PLTR sells software licenses to generate its revenue, it has considerable consulting services embedded in that license agreement. Given the labor-intensive nature of these consulting services, profit margins remain pretty fixed even as the company scales. The reason these consulting services are so needed is because PLTR’s platforms need to be custom-tailored to fit client needs, requiring considerable expertise and effort from PLTR’s engineers.

Until PLTR can figure out how to make its model less labor-intensive and can begin to increase its profit margins more meaningfully as it grows, PLTR’s intrinsic value growth will be fairly limited.

#3. PLTR Stock Is Way Overvalued

Last, but not least, PLTR’s valuation multiples are incredibly rich right now. On a forward basis, it trades at a P/E ratio of 82.66x, its EV/EBITDA multiple is an incredibly high 66.92x, and its EV/Revenues is 17.23x. If PLTR was enjoying strong economies of scale and seeing its profit margins rapidly expanding with growing revenue, these multiples would make more sense. However, it is simply not doing this. Analysts expect revenue to grow at a 23.7% CAGR through 2027 and they expect normalized earnings per share to grow at a virtually identical 23.6% CAGR through 2027.

Even if PLTR can achieve analyst consensus estimates of $0.50 in earnings per share in 2027, it would still be priced at 38x 2027 earnings if its share price remained constant with where it is today. Keep in mind that earnings per share is expected to be growing at ~20% at that point, making this look like a pretty reasonable assumption of a fair value multiple at that point. That means that there is a very real possibility that PLTR will not generate any total returns over the next three and a half years. The risk-reward profile does not look attractive at all at these prices, with a lot needing to go right for PLTR to generate even close to decently attractive total returns moving forward.

Investor Takeaway

PLTR has been one of the market’s biggest winners this year and appears to have incredible stock price momentum to soar ever higher. However, when taking our eyes off of the scoreboard and looking at the playing field, the long-term outlook looks far less exciting. Yes, PLTR is growing at a solid clip. However, its topline revenue growth has been decelerating since it went public in 2020, its economies of scale are very weak, its international business actually shrunk last quarter and is experiencing anemic growth overall, management has yet to provide quantifiable guidance for how artificial intelligence is going to reaccelerate their revenue growth and seems to have abandoned their original 2025 revenue guidance, and the stock’s valuation multiples appear to be way too high compared to analyst consensus estimates and the business’ recent growth rates.

PLTR is definitely an innovative company with strength in a hot, fast-growing industry and could therefore certainly see an explosion of growth moving forward. However, at the current valuation and given its recent performance track record, the risks seem to greatly outweigh the potential rewards heading into Q2 earnings. As a result, we rate it a Sell.

Read the full article here