The PANW Investment Thesis Seems Expensive As Revenue Growth Decelerates

Palo Alto Networks (NASDAQ:NASDAQ:PANW) is a global cybersecurity provider of comprehensive zero trust solutions for enterprise users, networks, clouds, and endpoints markets through the use of artificial intelligence and automation.

The company operates through the usual SaaS approach, with Subscription/ Support revenues comprising 77.1% (+1.9 points YoY) of its FY2023 revenues.

It goes without saying that the SaaS business model is one that is highly profitable as well, with the Subscription/ Support segment reporting high gross margins of 71.9% (+2.5 points YoY).

Combined with the “$200B of growth opportunity in cloud security alone” as remote work remains popular, along with the intensified cloud investments attributed to the generative AI boom, it is unsurprising that PANW has reported a double beat FQ3’24 earnings call.

This is with total revenues of $1.98B (+0.5% QoQ/ +15.1% YoY), operating margins of 8.9% (+6.2 points QoQ/ +4.3 YoY), and adj EPS of $1.32 (-9.5% QoQ/ +26.9% YoY).

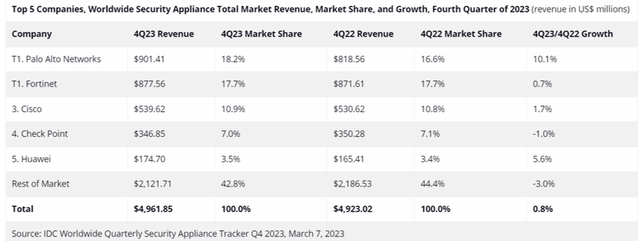

Worldwide Security Appliance Total Market Revenue

IDC

With growing multi-year Remaining Performance Obligations [RPO] of $11.3B (+4.6% QoQ/ +22.8% YoY), it is apparent that PANW’s offerings remain sticky, as observed in the expanding annualized subscription revenues of $4.16B (+1.9% QoQ/ +25.3% YoY).

And the long-term visibility into its eventual revenue recognition is why PANW seems likely to continue reporting robust market share in the Worldwide Security Appliance market in 2024, based on the 18.2% (+1.6 points YoY) of market share reported in Q4’23 by International Data Corporation.

This development also demonstrates why PANW has benefited from the sustained cloud transition since the COVID-19 pandemic, with its large platform and well-diversified offerings naturally allowing it to attract larger deals and more customers.

This also allows the management to engage on certain sales strategy in expanding adoption across three of its vertically integrated platforms: Strata (network security), Prisma (cloud security), and Cortex (security operations), while growing the customers’ lifetime value and reducing churn.

Key Risks From PANW’s Platformization Approach – Growth Appears To Be Decelerating

However, readers must also note that PANW previously introduced the new concept of “platformization” also known as “multi-platform wins” in the FQ2’24 earnings call, with the management looking to accelerate its growth opportunities in the near-term.

This is by offering “free support during a breach,” while “approaching customers well before their point product contracts expire and offering free extended rollout period prior to the end of the obligation of legacy vendors/ payment.“

As a result of the slower monetization/ revenue recognition, it is unsurprising that PANW has guided near-term top-line headwinds in the FQ2’24 earnings call, wiping out -28.4% or the equivalent $30.89B of its Market Capitalization at its worst.

Even so, we are impressed that the SaaS company continues to report robust profitability in FQ3’24, exemplifying its improved operating scale despite the near-term impact “by payment terms where more and more customers prefer annual billing plans.“

At the same time, it appears that PANW’s platformization strategy has paid off extremely well, with “65 incremental platformization sales” already completed in FQ3’24 and the management seeing “a runway to delivering approximately 2,500-plus platformization sales, up from the current 900.“

This further demonstrates its widening economic moat in an increasingly crowded cybersecurity market, where “enterprise spending is usually sticky, with significant risks and upheaval required to switch from existing vendors.”

With greater visibility into its platformization efforts and the growing customer base thus far, we can understand why PANW has moderately raised its FY2024 guidance again to total billings of $10.15B (+10.4% YoY), revenues of $8B (+16.1% YoY), and adj EPS of $5.57 (+25.4% YoY) in the FQ3’24 earnings call.

This is up from the previously lowered numbers of $10.15B (+10.4% YoY), $7.97B (+15.7% YoY), and $5.50 (+23.8% YoY) in the FQ2’24 earnings call and the original guidance of $10.95B (+19.1% YoY), $8.175B (+18.6% YoY), and $5.33 (+20% YoY) offered in the FQ4’23 earnings call.

However, it is undeniable that the massive fluctuation in PANW’s FY2024 guidance is alarming, with the management’s free trial platformization approach already shaking the shareholders’ confidence in their forward execution. This is due to the slower revenue recognition and the inherently decelerating growth trend compared to its direct peers, such as CrowdStrike (CRWD) and Zscaler (ZS).

For context, CRWD reported excellent FY2024 total revenues of $3.06B (+36.6% YoY) in March 2024 while guiding FY2025 numbers of $3.95B at the midpoint (+29% YoY), demonstrating its consistent high-growth stage.

The same high-growth trend can also be observed in ZS, with raised FY2024 revenue guidance of $2.12B (+31.6% YoY) and adj EPS of $2.75 (+53.6% YoY), implying the robust demand for cybersecurity offerings as the world enters the next super cycle of cloud computing.

And this is perhaps why PANW has had to embark on this aggressive platformization/ sales approach to avoid from losing out during this race, with the management’s low double-digit growth guidance naturally paling in comparison to its peers’ guidance.

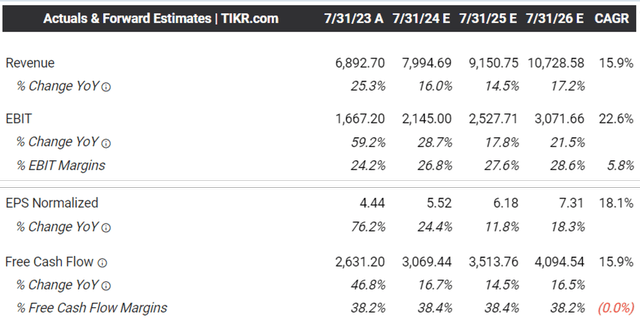

The Consensus Forward Estimates

Tikr Terminal

Thanks to PANW’s decelerating growth guidance, it is unsurprising that the consensus have already moderated their forward estimates, with PANW expected to report an underwhelming top/ bottom-line growth at a CAGR of +15.9%/ +18.1% through FY2026

This is compared to the previous estimates of +22.3%/ +24.9% and the historical growth at +25.9%/ +34.5% between FY2016 and FY2023, respectively, marking the end of its high-growth trend.

For now, with a cash/ short-term investments of $2.88B (-14.2% QoQ/ -27% YoY) and convertible senior notes of $1.16B (-36.2% QoQ/ -68.4% YoY), it appears that PANW remains more than well capitalized to weather the near-term uncertainties.

This is significantly aided by the growing Free Cash Flow generation of $3.01B over the LTM (+9.8% sequentially), with the consensus also projecting robust cash flows, implying the SaaS company’s ability to sustain its platformization/ sales approach ahead.

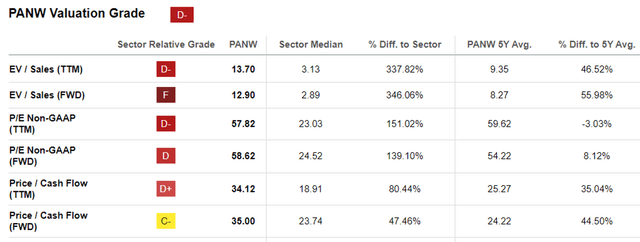

PANW Valuations

Seeking Alpha

However, this is why we believe that PANW appears to be expensive at FWD P/E valuations of 58.62x, compared to its 1Y mean of 50.54x and 3Y pre-pandemic mean of 42.24x, due to its decelerating growth trend ahead.

Even when we compare against its cybersecurity SaaS peers, such as CRWD at FWD P/E valuations of 89.06x, Fortinet (FTNT) at 35.19x, ZS at 65.39x, and Okta (OKTA) at 45.41x, it is apparent that PANW is not cheap here.

This is especially when comparing PANW’s consensus forward estimates through FY2026 against CRWD at +27.4%/ +27.8%, FTNT at +12.2%/ +12.5%, Z at +26.9%/ +31.1%, and OKTA at +13.1%/ +28.5%, respectively, with the former’s inflated stock valuations offering interested investors with a minimal margin of safety despite the recent pullback.

With PANW no longer being a high-growth stock, we believe that the premium embedded in its stock valuations are unjustified for now.

Readers may want to monitor its execution in the intermediate term, until its billings growth accelerates nearer to its better performing peers and its robust RPOs are monetized as revenues.

So, Is PANW Stock A Buy, Sell, or Hold?

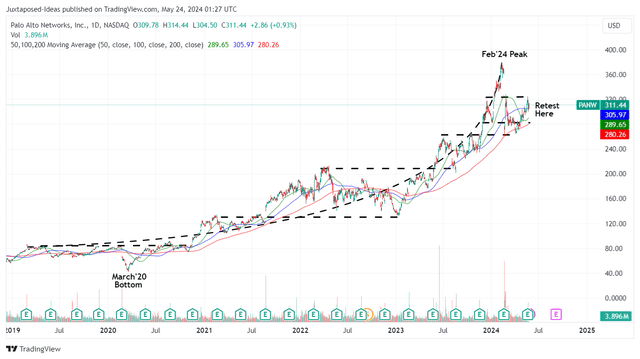

PANW 4Y Stock Price

Trading View

For now, PANW has already pulled back by -3.8% since the recent earnings call, if not by -14.9% since the painful FQ3’24 earnings call when the management drastically cut their FY2024 guidance.

Despite so, it is apparent that the stock is trading at a notable premium of +28.4% to our fair value estimates of $236.50, based on the LTM adj EPS of $5.60 and the 3Y pre-pandemic P/E mean of 42.24x (nearer to its lower growth peers, attributed to PANW’s slower monetization trend).

Based on the consensus FY2026 adj EPS estimates of $7.31, there appears to be a minimal margin of safety to our long-term price target of $308.70 as well.

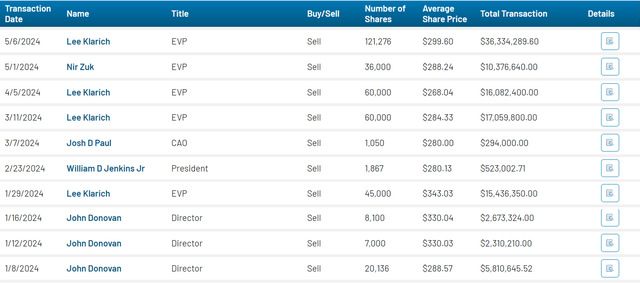

PANW Insider Selling

Market Beat

At the same time, readers must note that PANW insiders have been incrementally cashing out at these peak levels as well, worsening its investment thesis, as shareholders continue to be diluted with $1.06B in LTM stock-based compensation (+2.9% sequentially) and bloated share count of 354.6M (+9.9 sequentially/ +71.1M since FY2019).

As a result of the uncertain risk/ reward ratio, we are initiating a Hold (Neutral) rating for the stock here, with it likely to continue trading sideways until it grows into its premium valuations.

Meanwhile, traders may consider doing a momentum trade and coming back in after a deep pullback.

Read the full article here