In my past write-ups of Palo Alto Networks (NASDAQ:PANW) I noted that while XSIAM and AI were certainly creating some renewed excitement and that company had done a nice job diversifying away from its traditional firewall business that I thought the stock looked fairly valued. The stock is up over 25% from my original April write-up, but down nearly -10% since my early July follow-up.

Company Profile

As a refresher, PANW is a cybersecurity firm that offer solutions for network security, secure access service edge, cloud security, and end point security. The company sells both products and subscription services.

On the product side, the company is known for its firewall appliances & software. On the subscription side, meanwhile, PANW offers a variety of cloud-delivered security services solutions. These include things such as Threat Prevention, Advanced Threat Prevention, WildFire, Advanced URL Filtering, DNS Security, and other solutions that are often sold as add-ons to its firewall appliances and software.

It also provides cloud security, secure access service edge, and security operations solutions that are sold on a per-user, per-endpoint, or capacity-based basis.

Fiscal Q4 Results

For its most-recent quarter, PANW grew its revenue 26% to $1.95 billion. Analysts were looking for revenue of $1.96 billion. Adjusted EPS rose 80% to $1.44, beating the consensus by 15 cents.

Subscription revenue climbed nearly 27% to $1.45 billion, while product revenge jumped 24% to $507.4 million.

Fiscal Q4 billings rose 18% to $3.2 billion, while its remaining performance obligations (RPOs) climbed 30% to $10.6 billion.

Looking ahead, PANW forecast fiscal Q1 revenue to come in between $1.82-1.85 billion, good for growth of between 16-18%. It expects adjusted EPS to grow 39-41% to $1.15-1.17. Billings are projected to rise 17-19% to $2.05-2.08 billion.

For the full year, the company guided for revenue of between $8.15-8.20 billion, representing growth of between 18-19%. It expects adjusted EPS to grow 19-22% to $5.27-5.40. Billings are expected to increase by 19-20% to $10.9-11.0 billion.

On its FQ4 earnings call, CFO Dipak Golechha said:

“We have proven over the last 5 years that we target the largest and most attractive parts of the market. We’ve been able to capitalize on an expanding opportunity, taking share from within existing markets and positioning ourselves in new markets to drive further growth potential. Our share today stands at just 7% of our addressable market, which is lower than the share of leaders in many other markets outside of the cybersecurity industry. As we plot the course to the larger town that Nikesh outlined over the next 5 years, we continue to see the opportunity to gain share in our existing markets and continue to fuel above-market growth for Palo Alto Networks. … We’re targeting growth of 17% to 19% in revenue and billings over the next 3 years, which is ahead of the cybersecurity market growth rate. We see hardware as a percentage of our total revenue decreasing to approximately 10%, with NGS ARR exiting fiscal year ’26, above 55% of our fiscal year ’26 revenue. RPO remains an important metric as it captures the full value of our customer contracts independent of payment terms, and we expect growth of 25% annually through fiscal year ’26. Additionally, we see about 2/3 of our revenue in fiscal year ’26 driven by current RPO entering the year, highlighting the increase in predictability of our revenue profile.”

In an unusual move, PANW’s fiscal Q4 earnings call was held on a Friday after the bell. That usually isn’t a good sign, but there wasn’t any surprising bad news and the stock rallied strongly the following Monday session, up 16%.

Overall, the quarter was solid, although not spectacular, with the company growing the top-line nicely, but basically coming in line with expectations. The company continues to see nice operating leverage, which is showing up its it earnings.

The fiscal Q1 revenue guidance was a bit light of analyst expectations, as was its full-year sales forecast. It’s medium-term outlook, meanwhile, sees a company growing solidly, but also seeing growth decelerate as well. The overall guidance is likely conservative, but I don’t see the company blowing it out of the water given its size and the current economic backdrop.

Goldman Conference

Earlier this month, CEO Nikesh Arora was at the Goldman Sachs Communacopia + Technology conference. Security operations center (SOC), with the term broadening its XSIAM strategy, was a big topic at the conference. The CEO noted that the company launched its SOC product just 9 months ago and that it already has $200 million in bookings. He said most SOC is being protected by 15-year old tech and that what is happened to endpoint protection is now happening in SOC.

At the conference, Arora said:

“The traditional approach to security is there is this thing called SOCs. You try to protect an enterprise by buying a whole bunch of security software and every piece of security software, either block something bad or sends an alert saying, hey, here’s a problem, go figure it out yourself to your customer because you have 40 different security vendors, and I don’t know what do with that. And this thing went into a thing called SOC. And you had a bunch of analysts who would figure out what happened. … The mean time to fixing a SOC is still 6 days because this is a problem that is not going to fix itself. The only way to fix the problem is stop collecting data and analyzing it later is to start analyzing it as you collect the data. So we’ve spent 5 years building that tech. … Our first 10 customers, we’ve taken them down from 6 to 7 days to an average of 5 hours of fixing security. Our aspiration is to get them to under 1 minute, which is where we are. So eventually, security has to become real time. We are running 1,300 machine learning models in our product, which is what I like to call precision AI. So this is not ChatGPT or OpenAI. This is precision AI, 1,300 machine learning models, the models you’d want to drive your car. You don’t want ChatGPT driving your car. If it hesitates, it’s a bad idea.”

Polaris Market Research

SOC looks like it could be the next big growth drive for PANW, as it leverages its machine learning and AI capabilities to not only detect security issues but also fix them. This is projected to be a nice growing market, and PANW looks well positioned to take share and displace current legacy players in the space.

Valuation

SaaS companies are generally valued based on a sales multiple given their high gross margins and the companies wanting to pump money back into sales and marketing to grow. PANW currently gets about 80% of its revenue from recurring subscriptions and support.

PANW is projected to generate $8.2 billion in revenue in fiscal 2024 (ending July) and $9.7 billion in fiscal 2025. 80% of those numbers are $6.6 billion and $7.8 billion, respectively. Thus, based on subscription revenue it trades at an EV/sub revenue multiple of 10.2x and 8.6x, respectively.

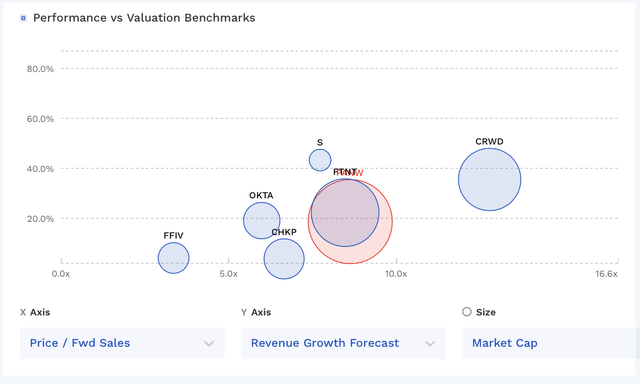

From a pure P/S multiple, PANW is among the higher valued cyber security firms, trailing only CrowdStrike (CRWD). Its growth is better than many of the companies in the space, but there are some better values it appears, such as Okta (OKTA), although it is offering a much different type of solution and isn’t some of the hottest areas of cybersecurity, such as PANW.

PANW Valuation Vs Peers (FinBox)

Conclusion

PANW continues to expand the breadth of its solution to be more comprehensive, with the talk of XSIAM now being an entire SOC transformation. It thinks it can do to SOC what CRWD did endpoint security market. This is a huge market and takes PANW from being a legacy firewall player that is being hunted to becoming the hunter. Its $200 million in bookings in this area in a short time is a good start.

Valuation comes into play and at 10x sub revenue, the stock is pretty fairly valued. However, there is still product revenue in there that carries good margins (73.5% last year). Valuing the subscription business at 10x revenue and products at 5x, gets you to a $290 stock based on FY 2025 forecasts.

That’s about 15% upside, which keeps me at “Hold” looking for a little better entry point. I’d prefer to be a buyer around $215.

Read the full article here