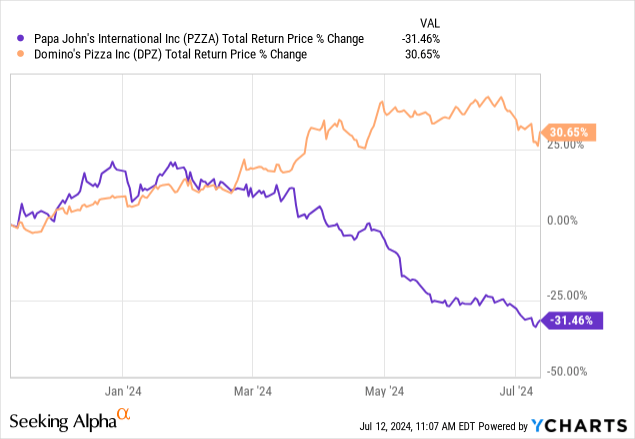

Papa John’s International, Inc. (NASDAQ:PZZA) stockholders haven’t had it easy in recent times. These shares have now lost around 65% of their value from their 2021 peak, having fallen around 30% (with dividends) since I opened on the firm last November. Covering it back then with a ‘Hold’ rating, I wasn’t thrilled with the valuation here compared to what was on offer at close peer Domino’s (DPZ), and with the latter outperforming by around 60ppt in that time, the contrast in fortunes between the two has been pretty stark.

Given the magnitude of the share price decline, it would be natural to think that something has gone badly wrong at Papa John’s. I’m not sure it has. Granted, operations are in something of a soft patch, with comps looking weak, earnings guidance downgraded, and net unit growth also trailing management’s medium-term target.

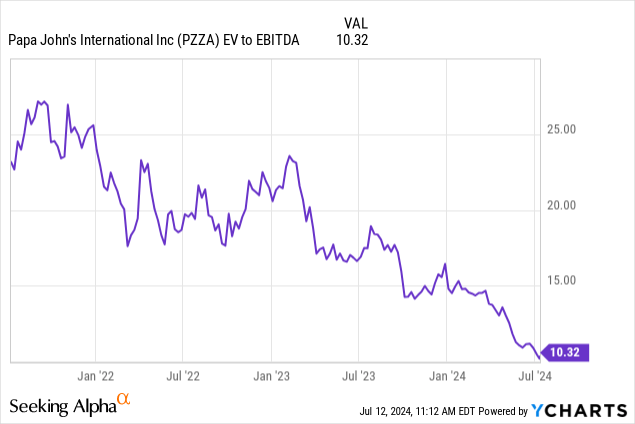

On that side, I think PZZA’s previously lofty valuation has been the larger issue here. The fact is that these shares were on a punchy EV/EBITDA of over 20x at their 2021 peak, and that was always going to require a lengthy spell of strong growth to justify.

With the stock down heavily in that time, that EV/EBITDA multiple has contracted to around the 10x mark, meaning investors only need very modest growth assumptions to make things work. While I am mindful that the business isn’t exactly firing on all cylinders right now, there is also a fairly wide margin of safety to work with here, and I upgrade my previous ‘Hold’ rating to ‘Buy’ as a result.

Hitting A Soft Patch

Papa John’s has released two quarters’ worth of fresh figures since my initial piece (N.B. Q2 2024 results aren’t due until next month), and business has definitely weakened in that time. Comparable sales growth has turned negative for one, with management basically pinning the blame on cost-conscious consumers. North American restaurants – which account for around 60% of the total estate size – saw comps fall 1.8% year-on-year in Q1, while international restaurants fared slightly worse, with comps down 2.6% in the quarter. This led to company-wide comps falling by around 2% year-on-year in Q1.

PZZA has continued to grow its store count, so the effect on total systemwide sales (i.e., the sum of all restaurant-level sales in both company-operated and franchised outlets) has been more modest, with this down just under 1% year-on-year in Q1 to $1.23 billion.

Guidance has also been lowered. Initial guidance had Papa John’s delivering North American comparable sales growth of around 2% in 2024, representing the low end of management’s 2-4% long-term target. Given the weak Q1 print, full-year domestic comps guidance has been downgraded to “flat to down low single-digits”. This has had a knock-on impact on operating profit guidance, with management now seeing full-year EBIT at $150 million at the mid-point compared to the initial 2024 midpoint guidance of $158 million.

It’s Not All Bad

While negative revisions aren’t good, I would point out that it’s not all bad here. Restaurant-level economics have shown improvement for one, with domestic company-owned outlets seeing around 220bps of margin improvement in Q1 as inflationary pressures have eased.

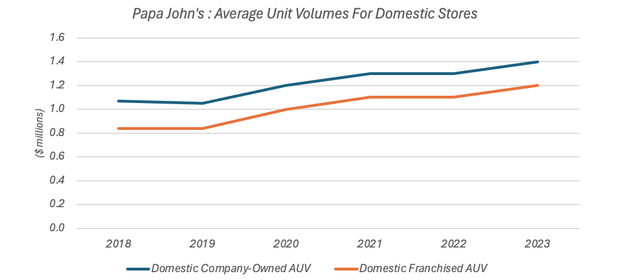

These company-owned outlets delivered a circa 21% EBITDA margin in Q1. Franchised-store margins will be lower, as royalty fees to the head company swallow around 5% of franchised-store sales. Furthermore, average unit volumes in franchised outlets are typically lower (they were around $1.2 million last year versus $1.4 million for domestic company-operated ones), so franchised-store margins are likely to be structurally lower due to the inherent fixed cost leverage in running a restaurant.

Data Source: Papa John’s International Forms 10-K

Having said that, unit economics would be solid even if we were to conservatively assume 10% EBITDA margins for franchised outlets. As I mentioned last time, a new store only required cash investment costs of around $345,000 back in 2018 as per that year’s 10-K. With inflation, that has likely risen to around $450,000 today, pointing to a circa 25% return on investment given the implied franchised-store EBITDA of $120k. Franchisees are incentivized to open up more stores if underlying returns on investment are attractive, so that figure would give me some confidence with respect to future unit growth potential.

With that, management’s longer-term target is 5-7% annual net unit count growth. Growth is trailing that presently, with the company reporting around 3.3% year-on-year net unit growth in Q1, but I would be inclined to accept that this is largely due to cyclical weakness on account of current macro conditions. The key is that unit economics still look solid here – and that should ultimately be a significant driver of future earnings growth.

Valuation

The good news for prospective investors is that you don’t need aggressive assumptions to make things work here. Helpfully, management has also disclosed 2024 guidance on D&A (~$72.5 million), CapEx (~$80 million), and the effective tax rate (23-26%) alongside the previously-mentioned figure for EBIT (~$150 million). Those numbers get me to around $105 million in estimated 2024 free cash flow to the firm (“FCFF”). With PZZA’s current enterprise value at ~$2.2 billion and its WACC at circa 7.8%, investors only really require around 3% annualized long-term growth to make the current share price work.

That is a very low bar to clear. Franchised stores are incredibly high margin and capital-light as they attract little by way of additional operating expenses and CapEx. In addition, I mentioned last time out that management also plans to increase the margin on its domestic commissary business from 4% (in 2023) to 8% by 2027. Excluding unallocated corporate expenses, this business accounted for around 18% of company-wide EBIT last year. Management plans to stagger this increase in annual increments of 100bps, and this should similarly provide profit growth at little to no extra increase in investments or expenses.

As such, I expect Papa John’s to display meaningful leverage over operating expenses and CapEx, and this should fuel strong growth in medium-term free cash flow. Indeed, current sell-side consensus implies around $128 million in FCFF by 2026, with implied FCFF margins expanding by around 20% to 6% of sales. Incorporating that into a simple DCF model would get me to a fair value of approximately $65 per share, with that based on a five-year forecast period and a terminal ROIC-driven EV/EBITDA of around 12x. With the stock currently at $43.56, there is a reasonably large margin of safety on offer should the company fall short at the business level.

Summing It Up

This has been a rough few years for Papa John’s shareholders, with an investment at the 2021 peak ultimately losing around 65% of its value with dividends included. While business is definitely soft right now, I do think the stock’s previously rich valuation has been the bigger driver of underperformance here, while sound unit economics mean that the ingredients for reasonable future growth are still present. Most importantly, with these shares now trading for just 10x the estimated 2024 EBITDA, prospective investors have quite a bit of leeway should the firm ultimately fall short on the growth front.

Read the full article here