Research Note Summary

For today’s research note I’ll be covering my first REIT stock on this portal, Park Hotels & Resorts (NYSE:PK), which I picked from the sector of hotel and resort REITs.

I gave this stock a neutral / hold rating today and here are some reasons why:

Although it has seen an uptick in room demand post-pandemic and achieved revenue growth, it is still below its sector average on revenue growth YoY and also has struggled with profitability, posting a net loss in the last reported quarter.

Its 3-year dividend growth is poor, although its dividend yield is not far from the sector average.

A major risk identified with this company is its debt load and a recent notice of loan default on one of its loans. The stock also could present an undervalued opportunity when looking at its valuation and share price right now.

Methodology Used

I will utilize my WholeScore Rating methodology which looks at this stock holistically across 6 categories including potential downside risks, and assigns a rating score.

Some of the data used comes from the most recent reported quarterly earnings results on Aug. 2nd (for FY23 Q2), while forward-looking estimates relate to upcoming Q3 earnings results due out on Nov. 1st.

Industry Outlook

When investing in the sector of hotel and resort REITs, I am essentially investing in a real estate investment trust that is also traded as a stock on a major exchange, such as the NYSE. So, the analogy I use is that it’s like owning a small piece of a large portfolio of properties you did not have to buy directly yourself, nor do you have to maintain them.

The REIT then invests in a portfolio of properties, in this case hotels and resorts that make money not from apartment rentals but from rooms booked, in addition to ancillary revenue such as from conferences and food/beverage.

Earlier this year, I got to attend the groundbreaking for a new hotel project in coastal Croatia in southern Europe, which is owned by a hotel REIT but will be managed by Hyatt (H) and have the Hyatt brand associated with it. This also occurs often with the Hilton brand (HLT) as well. In other words, Hyatt and Hilton does not actually “own” a lot of the properties with their name on them, but the property itself is owned by an investor or a REIT with many investors.

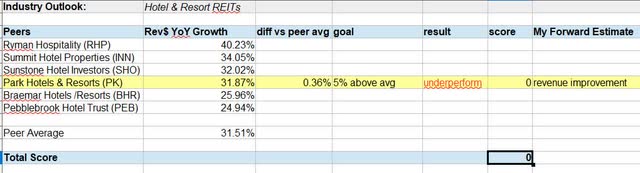

When comparing Park Hotels with its sector in terms of YoY revenue growth, we can see that it is somewhere near the peer group average on YoY revenue growth, so not great but not terrible. In fact, it is a meager 0.36% above the average.

Park Hotels – industry outlook (author analysis)

However, my target is YoY revenue growth of 5% above the peer average, so it did not quite make the cut this time. I think, though, that there will be revenue improvement going forward as most recent figures from Q2 indicate increasing YoY occupancy and demand, particularly in some urban centers.

Keep in mind about this industry that it is subject to the effects of recessions, seasonality, and as we saw in 2020 the effects of travel disruptions due to pandemics. There is still no definitive view from all economists as to whether a major recession will occur in near term or not.

The bright spot on the horizon for this company, and its sector, is that the travel sector seems to have recovered post-pandemic but we also do not know what policymakers will do in the next year, two, or five, and whether the pandemic reality will re-surface again or not.

This table below from the company’s Q2 results shows how their revenue breaks down by category. As you can see, rooms booked is a key revenue driver in this business, followed by food/beverage revenue. In both categories, Park Hotels saw YoY growth:

Park Hotels – revenue by category (company Q2 results)

For the time being, I gave this stock a score of 0 in this category, but I estimate revenue improvement going forward, driven by travel demand.

Financial Statements

Now, let’s discuss the financial statements and their relevance to my investor readers.

As you can see, most recently this firm achieved a YoY revenue growth of 2.43%, but just missed my target of a 5% growth.

However, based on revenue info I touched on in the prior section I estimate the next quarter to be positive on revenue for this company, driven by the increased travel demand and room bookings.

Park Hotels – financial statements (author analysis)

In terms of net income, unfortunately the firm achieved a net loss in the last quarter reported, which was a 200% YoY decline and definitely missed my target. My forward-looking sentiment on net income will remain negative on this stock as pressure from interest-expenses also continues. This is also an industry with high overhead, so there is the constant expense of actually maintaining the properties and in times of elevated inflation I suspect that materials generally cost more than 5 years ago.

The supporting evidence is in the following two tables which show not only a 195% drop in profitability (adjusted on YoY basis) but also the company outlook for FY23 is also expecting a net loss, whereas their prior FY23 estimate called for a profit.

Park Hotels – YoY net loss (company Q2 results) Park Hotels – FY23 outlook (company Q2 results)

In terms of free cashflow per share, it outperformed my target on a YoY basis, and I expect continued positivity there, but one area of concern is the YoY decline in positive equity.

This, I expect, will continue to be an issue due to the heavy debt load of this company that impacts the balance sheet and equity.

In this category, I gave the stock a score of 1.

Dividends

When it comes to this stock’s dividends, I was looking for it to exceed the sector average on dividend yield by 5%, but it actually came in 5% lower than average so it missed my target there.

Park Hotels – dividends (author analysis)

When comparing the dividend amount from Q2 2023 with the one 3 years earlier from Q2 2020, the growth was actually negative, at -67%. Therefore, it underperformed my target of a 5% dividend growth over 3 years. I estimate the same in the next quarter as they did not yet announce a dividend hike.

It should be mentioned that this company, like many in the travel/hospitality space, faced the 2020/2021 global pandemic and ensuing effects on its industry, so it is not surprising that they did not grow dividends but attempted to preserve capital wherever possible.

My goal of earning at least $100 in annual dividend income from holding 100 shares of this stock is achievable as their dividend is $0.15, and I am looking for serious companies with a dividend of at least $0.10 per share on a quarterly basis. I bring this up because I like to think of investing not in a stock but into an existing stream of cashflow opportunities.

I believe the yield will be close to or in line with the sector average which is hovering around 5.3%, as I don’t expect the share price to drop drastically or rise drastically, which could affect the dividend yield.

In this category, I gave the stock a score of 1.

Share Price

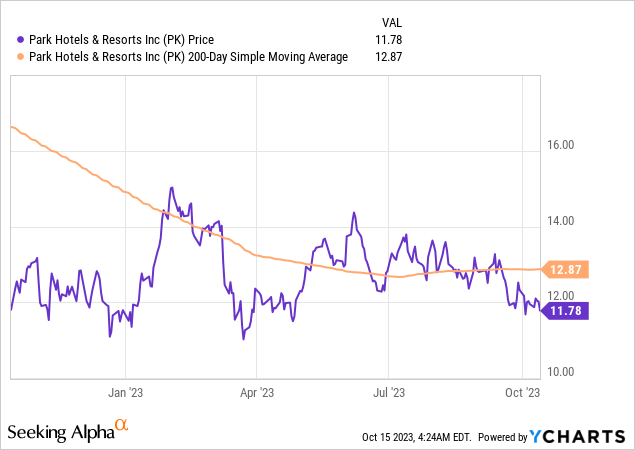

In terms of the share price, I think it is looking like a value opportunity based on the chart below, showing a crossover below the moving average occurred a few months ago and the stock still trading below the average.

In the following table I created, my target is that the share price be no more than 5% above the 200 day average, and in this case it is actually 8.4% below the average.

Park Hotels – share price (author analysis)

My 1 year price estimate is $14.16, or 10% above the current average. If this were to materialize, that is a price gain of $2.38 per share. On 100 shares, a capital gain of $238.

The reason I think it has potential to go 10% above average is the tailwind this industry has gotten after the uptick in travel demand, which can be seen in the revenue growth, and in a year’s time that could improve even more which would make this sector more attractive to the bulls.

However, there is downside potential as well, particularly if another pandemic wave resurfaces and travel is shut down again, which we do not know right now and that is a big question mark. So, another reason I don’t want to pay too much above the moving average for this stock.

In this category, I gave the stock a score of 1.

Performance vs S&P500

Next, I want to briefly mention the market momentum on this stock in relation to the S&P500 index.

As you can see from the table I made, Park Hotels had a 1 year price return that was negative, and also was 103% below the S&P500 index which saw nearly an 18% price return in the last year. So, this stock came under my target goal of outperforming the index by 5%.

Park Hotels – performance vs S&P500 (author analysis)

My forward-looking estimate has a negative sentiment, because I don’t think the market is super bullish just yet on this sector overall.

The S&P500 index also is made up of many big name tech giants, which saw lots of bullish momentum this spring after investors fled bank stocks en masse it seemed and fled to big tech. So, I don’t think travel & hospitality is quite at a point that it will outperform a tech-heavy index like this, especially since the pandemic was tech-friendly and not so friendly to the travel sector, which has recovered but not quite 100% just yet I don’t think, since now it has to deal with elevated inflation and high interest rates on credit too.

In this category, I gave this stock a score of 0.

Valuation

Ahh, one of the most complex topics I get asked to talk about: valuation!

To simplify and shorten this topic, I chose two metrics, the forward price-to-earnings and price-to-book ratios.

As you can see, both of which are undervalued by quite a bit.

Park Hotels – valuation (author analysis)

In my opinion, the driver for these seems to be poor bottom-line YoY earnings performance, despite strength in top-line revenue and an uptick in demand.

Further, net interest expense continues to hover around $50MM to $60MM per quarter, due to the company’s high debt load and current rate environment.

I think the undervaluation is driven by the market’s reaction to poor earnings and high debt costs, not to mention a recent loan default, while the top-line revenue opportunity and uptick in room demand presents a value-buying opportunity right now, at these low valuations.

In this category, I gave the stock a score of 2, and am expecting similarly low valuations going into the next quarter.

Forward-Looking Risks

I put together this table below to determine a total risk score for this stock, and I gave it a score of -1.

The key risk, which is a downside risk, is the debt load of this company and related to that the recent notice of default on one of its property loans.

I would consider a loan default a high business impact, and high probability since it already happened.

Park Hotels – risk score (author analysis)

The supporting evidence is from the company’s Q2 results commentary, which highlighted the issued of a notice of default on a $725MM loan. I think that most investors and analysts will show at least moderate concern over this stock after taking this into account, and it shows in the downward price pressure on this stock.

Park Hotels – notice of default (company q2 results)

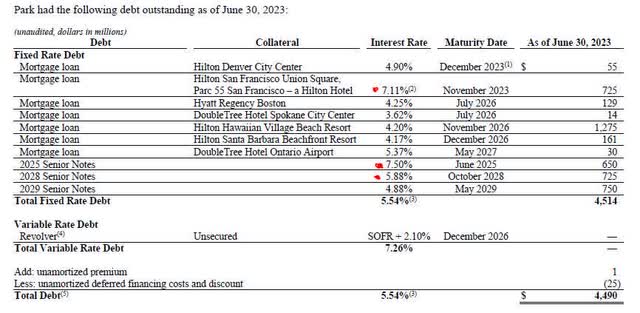

In an earlier article I mentioned the concern of rising debt levels during the current elevated interest-rate environment. If you look at the outstanding debt of Park Hotels below, you can see that some of the debt is costing them well over 5.5%, and even 7.5%. I think these are considerably high costs of debt.

Park Hotels – outstanding debt (company q2 results)

However, somewhat of a mitigating factor is that according to their balance sheet the long-term debt is decreasing on a YoY basis:

Park Hotels – long term debt YoY (Seeking Alpha)

While this is positive news, it is still not where I would like them to be on debt, at least not until rates come down significantly, so another reason I am not a buyer of this stock right now but would be a holder instead.

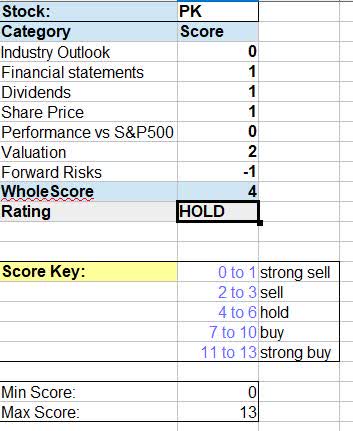

WholeScore Rating

In today’s rating, this stock got a WholeScore of 4, giving it a Hold / Neutral rating.

Park Hotels – WholeScore (author analysis)

My rating today agrees with the consensus from the quant system, which I think has accurately depicted this stock right now.

Park Hotels – rating consensus (Seeking Alpha)

Read the full article here