Editor’s note: Seeking Alpha is proud to welcome Dividend Dude as a new contributing analyst. You can become one too! Share your best investment idea by submitting your article for review to our editors. Get published, earn money, and unlock exclusive SA Premium access. Click here to find out more »

Investment Thesis:

I am rating Paycom (NYSE:PAYC) a strong buy because they are revolutionizing the way we get paid. Paycom is a cloud-based human capital management software solutions which is a software-as-a-service (SaaS) business model. It basically manages data analytics that various businesses need to manage the complete employment life cycle all the way from recruitment to retirement. This business model already differentiates itself from others in the space because it is cloud-based while other popular companies are not like Automatic Data Processing (ADP) or Paychex (PAYX).

It’s set apart in the landscape because it streamlines multiple services onto one cloud-based platform that employers/employees can use, respectively. Ultimately, it’s distinguished by its focus on automation, employee self-service and capabilities internationally. Some of the features that show this are the GONE time off product and the BETI payroll solution. They have a single database system to simplify HR processes and reduce costs.

Paycom’s product development and innovation continue to remain strong allowing the company to generate a narrow & growing moat in the industry. I believe this moat is only going to widen with time. Paycom also benefits from high switching costs while their competitive advantage ultimately lies in the all-in-one platform they offer. This is something that both Automatic Data Processing and Paychex also benefit immensely from and it’s one of the largest reasons many companies don’t switch to a different human capital management software such as Paycom. The main thesis is that Paycom is providing immense value to enterprises who use them, saving them time, & they do this all in one streamlined & cloud-based platform that will get better & better with time.

Competitive Landscape

Paycom does have some competitors. The most notable are Paylocity (PCTY), Paycor (PYCR), Workday (WDAY), & less directly but still notable the big players. These are Automatic Data Processing & Paychex. Paycom is differentiating themselves from Paylocity, Paycor, & Workday because they are not only targeting a different size of enterprise but they have many tools unique to their platform. The most notable of these is BETI which is very beneficial to many enterprises trying to save time which is Paycom’s whole pitch. Paycom is different from the leaders because it’s cloud-based, streamlined, & simply more advanced than Automatic Data Processing & Paychex. Paycom has a unique competitive position which is it’s advantage to carve out market-share & grow it.

Fundamentals

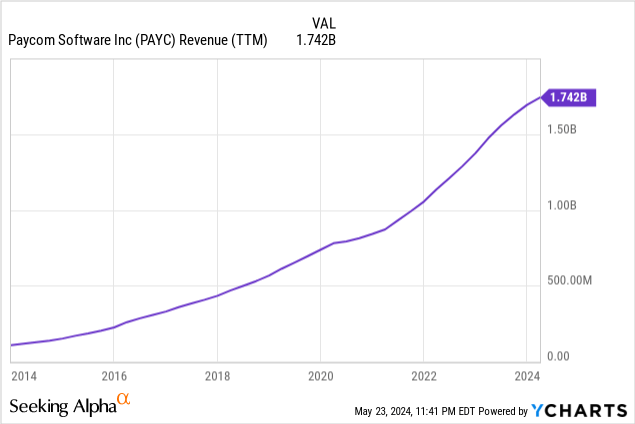

Paycom has some solid fundamentals when it comes to revenue, earnings, free cash flow, ROIC, balance sheet, etc. Starting off with revenue, the company has been able to grow revenue at a fast rate shown by the graph below. This represents a revenue growth CAGR of 31% over the past decade. This growth has decelerated slightly but still remains fast as of late above 17%. The large majority of this revenue is also reoccurring. In my opinion, this indicates that enterprises are satisfied with Paycom’s solutions & sticking around. This also gives Paycom many cross-selling opportunities once it has the enterprises using their platform.

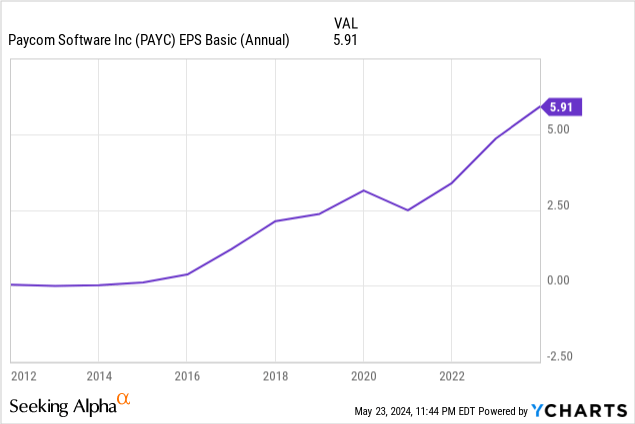

The company has been able to use this revenue to grow earnings per share (EPS) at an even faster rate. The company has an EPS CAGR of 27% over the past 5 years. The company has also begun to buyback shares boosting this metric as of late. With all the cash they have and 0 debt the buyback lever is always available. Especially as the price of Paycom gets cheaper. Net income growing & shares outstanding going down is really how to grow earnings per share at a fast CAGR.

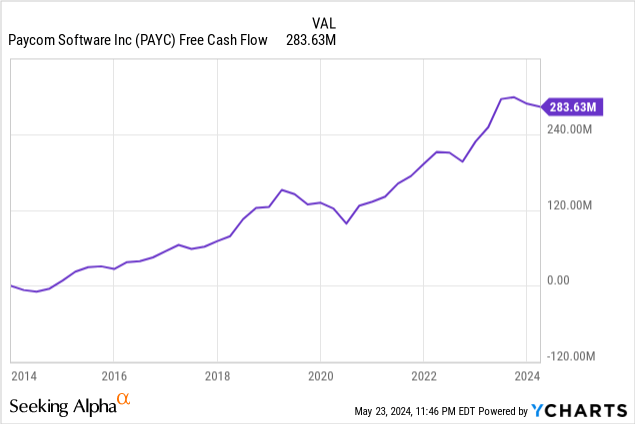

The company has also done very well on a free cash flow (FCF) basis. They have grown free cash flow at a 14% CAGR over the past 5 years despite the heavy spending into SG&A and R&D. I expect this company to continue to grow free cash flow at a double digit rate as the size of their clientele will continue to increase, as well as their overall customer count. Larger companies with more employees boost free cash flow, and currently they are aiming for those companies.

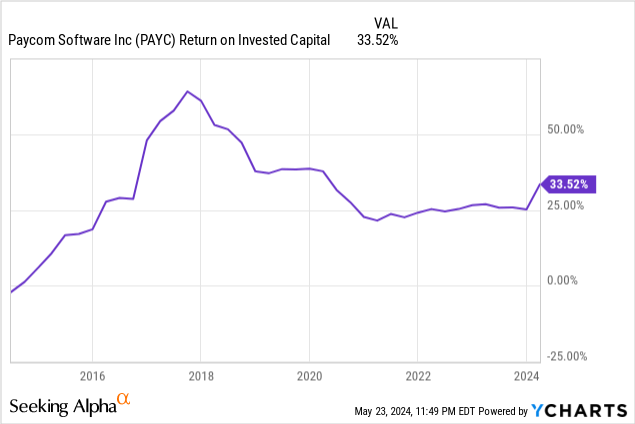

Now, these are intrinsic value drivers of the company but one of the most important in my personal opinion is the return on invest capital (ROIC) the company has. We want to see this metric in the double digits at least and would really love to see it above 12%-15% as this is the average in the S&P 500. We can see that over the past 10 years this ROIC metric has smashed the average and currently sitting at 33.52% so the free cash flow they get is well funded and reinvested back into the business. This helps them come up with new products for enterprises like most recently BETI. The more cash flow they can reinvest the more innovation can occur. In my opinion, they are taking advantage of this immensely!

Valuation

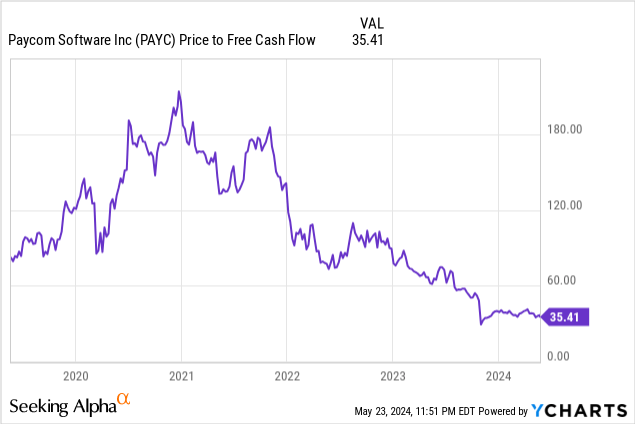

Now, these are intrinsic value drivers of the business and they all seem to be good and heading in the right direction. With this information that SHOULD reflect a stark increase in stock price over the past 5 years? Well if you thought that you would actually be WRONG. We can take a look at the price to free cash flow ((P/FCF)) which is actually trading at some of the lowest levels we have seen in 5 years. This is mostly driven by some growth concerns and price wars in the space. I do not agree with this mispricing by the market as the reason they’re total customer count growth has slowed down is due to them seeking out bigger customers which will in turn generate even more revenue and free cash flow.

From most metrics this company appears to be trading at lows in comparison to where it has usually traded. However, this can be misleading as some may believe the company is losing its strong market position and not taking market weshare at the rate they were. This is something I disagree with. The thesis for Paycom Software still remains intact. The company is still growing revenue, free cash flow, earnings per share, and in terms of key performance indicators (KPIs) still has a high retention rate and is growing customers over time. The retention rate for PAYC is current around 91% and has previously been around 90%-93%. Although there is a certain level of risk around Paycom, I still think they remain in a favorable market position with a widening moat. The company has also begun buying back shares which will only increase shareholder value as they believe their own company is undervalued. We can see they have done their first round of buybacks recently.

I believe these buybacks, as well as what I’ve discussed previously will continue to drive free cash flow per share higher and higher. Free cash flow per share is what I believe to be the BEST intrinsic value driver/teller of a business and I believe Paycom is going to grow this at a fast rate in the next decade.

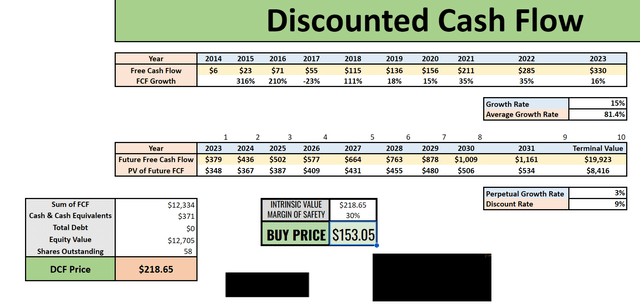

We can do a DCF on Paycom to see the value of their future free cash flows. We can see that we get an estimated fair value of $218.65 representing significant upside to the current share price of Paycom. I think growth can be even faster than 15% but I like to be conservative on my valuation models. The reason I believe this is because management has said that they expect growth to reaccelerate past next year.

Another thing to note is the building of offices for their employees is also making free cash flow look less than it should be. Once this stops happening at the rate that it’s happening right now, the free cash flow will be much higher. This also factors into my estimated free cash flow growth rate for Paycom. This makes me much more bullish on the company in the long run.

Overall, the company in my opinion is basically a GARP (growth at a reasonable price) opportunity here. Whether growth reaccelerates or it doesn’t the stock is not trading at a demanding valuation & should have good returns either way. This is why I am buying so heavily, I believe the risk-reward is very favorable at current price levels.

Author’s Calculation

Large TAM

The industry Paycom is in is expected to grow at a fast rate. Over the next 5 years the industry is expected to grow at a near double digit CAGR. 40% of companies still use offline human capital management services which is PERFECT for Paycom to come in and take advantage. Cloud-based solutions which Paycom offers should continue to take share.

AI will increase people wanting cloud-based solutions and I believe Paycom is in a favorable position to leverage AI into their products. Streamlining multiple services into one integrated solution is going to be very attractive to companies who use offline, point solutions. Paycom has a completely modern, easier, and more convenient service. AI will significantly increase productivity and data in every single segment of Paycom’s business model. This is something most of the competition cannot take advantage of.

This TAM is different than other players because of how much of the market they have yet to tap into. How many major enterprises still on HCM solutions that are not cloud-based & streamlined like Paycom is.

International Growth

Now that we have discussed the basic fundamentals and valuation I believe we can go into more specifics regarding the company. Paycom has recently tapped into the international market and it’s been going quite swimmingly for them. They launched their payroll product in the UK, Canada, and also Mexico. They have recently announced that they also plan to launch it in Ireland next. They have also spoken on earnings calls of getting interest from various big companies with global presences considering Paycom for their needs.

BETI To Drive Strong Sales

One of the biggest growth catalysts for Paycom is BETI (better employee transaction interface). BETI helps employees better manage payroll and the process as a whole. This will overall increase efficiency and reduce costs/hassle. The evidence of it being a strong value proposition is clearly there as 2/3rds of the customer base have already adopted BETI. I also believe BETI has pricing power that they can leverage in the future to increase margins and profits because the value proposition is just that strong. Nobody can tell the exact growth that BETI will bring, but it’s another positive catalyst for a company that already has many. BETI should drive strong growth in the future and management has a lever of pricing to pull with them whenever they feel it’s needed.

Bear Case

To simplify the bear case it’s simplify if a recession where to occur, Paycom would be one of the first to go. They will be impacted immensely in multiple ways as companies would reduce employee count, companies stop hiring, companies go bankrupt, & Paycom would not have such a strong position in selling new products as they really would not be needed. The company is not recession-proof like some others are.

In addition, it is possible that larger enterprises just don’t switch to Paycom and continue using Paychex & Automatic Data Processing. While I think it’s unlikely that is something that can happen. For instance, Automatic Data Processing has a very high retention rate despite their old & outdated solutions. It just goes to show how sticky this type of business can be.

Conclusion

My conclusion on Paycom is a “strong buy” rating and I have actually made Paycom the largest holding in my portfolio. Despite near-term growth concern pressure driving the price down the long-term opportunity is there. The massive TAM and BETI pricing power can drive long-term profit growth, while the thesis of an all-in-one payroll management service I think is attractive to companies. International expansion just beginning, continuing to take market-share, cross-selling products, pricing power among multiple segments, as well as increased return of capital to shareholders is what makes me so bullish. I think the intrinsic value of the company is near $300 based on current fundamentals. This is why I am assigning Paycom with a strong buy rating and I think they are poised to fight off competition and continue to be the attractive, easy, all-in-one, modern human capital management SaaS business.

Read the full article here