Editor’s note: Seeking Alpha is proud to welcome CJ Value as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis

PDD Holdings (NASDAQ:PDD) has been one of the most misunderstood Chinese companies since its IPO in the U.S due to the company’s secretive culture as well as U.S investors’ lack of first-hand shopping experiences with major domestic Chinese e-commerce players. Most investors view PDD as just another Chinese e-commerce player. But in reality, PDD has a very differentiated and superior business model than JD.com (JD) and Alibaba (BABA). This differentiated business model gives PDD a structural cost advantage against JD and Alibaba. With the recent launch of Temu, PDD’s trying to replicate its success in China across the globe. In my view, the current valuation of PDD is simply too cheap for a company that can still grow at 20-30% over the next 3-5 years.

PDD’s differentiated business model

While PDD, JD and Alibaba are all internet retailers, their business models are completely different.

First of all, JD and Alibaba (especially the T-Mall segment) focus mostly on branded products. PDD’s focus is mostly on the so-called “white label” products, or generic brand products. Branded products such as Nike (NKE) and Estee Lauder (EL) usually invest advertising dollars outside of the e-commerce channel to build brand equity and very little advertising on e-commerce channel. Therefore, brands are less willing to pay high commission on e-commerce platforms. But for those “white label” products sellers, because they rely heavily on the e-commerce channel, they are much willing to pay higher commission on e-commerce platforms. This is why PDD has already had a higher monetization rate than Alibaba and JD.

Monetization rate comparisons:

BABA,PDD, and JD’s most recent annual reports

Secondly, PDD has a different merchant ecosystem. For Taobao and T-Mall, the threshold to open a new store is very high. A Taobao store is very much like an offline store in the sense that it takes time to accumulate customers and reputation. But once the store gets enough good ratings and returning customers, life will be very easy. In a sense, it is a closed system that protects the incumbent stores. PDD’s merchant system is almost the exact opposite. It’s very easy to open a store on the platform. A seller can operate multiple stores. PDD’s algorithm will direct traffic to the store with the lowest cost regardless of how long the store has been running. As long as the store continues to offer high-demand products at the lowest cost, PDD will continue to direct traffic to the store. Unlike a Taobao store, a PDD’s store faces intense competitive pressure every day because of PDD’s intense focus on low cost. This fundamental difference in traffic algorithm makes PDD’s sellers much more competitive than Taobao’s sellers.

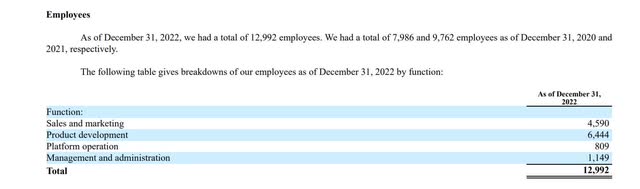

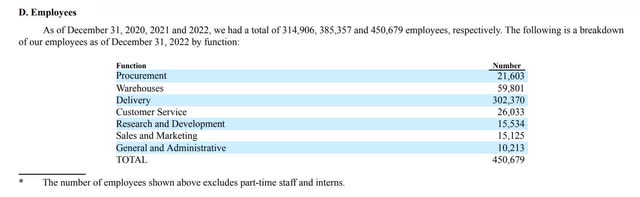

Thirdly, PDD has a much more efficient operating structure than both JD and Alibaba. Alibaba has more than 230,000 employees (as of March 31, 2023), while PDD only has less than 13,000 employees (as of December 31, 2022). The average profit per employee for Alibaba is only 308,000 yuan compared to 2.4 million yuan for PDD. JD’s even worse with more than 450,000 employees (almost 35 times as many employees) but the same level of GMV as PDD. It’s astounding how much more efficient PDD is compared to both Alibaba and JD.

PDD’s number of employees:

PDD’s annual report (p-108)

Alibaba’s number of employees:

Alibaba’s annual report (p-167)

JD’s number of employees:

JD’s annual report (p-148)

There are other differences in terms of business models among PDD, Alibaba and JD but the aforementioned three are the most important ones. Clearly, PDD has a structural cost advantage against its domestic competitors, and it is very likely PDD will continue to take share from both Alibaba and JD in the future.

Temu is replicating PDD’s success across the globe

PDD launched its international e-commerce platform Temu in September of 2022. Temu’s business model is very similar to the domestic platform Pinduoduo with some differences. First of all, Temu has the discretion in terms of product pricing whereas with Pinduoduo, sellers make their own pricing. Secondly, unlike Pinduoduo, on which sellers are responsible for logistics, Temu is responsible for warehousing and shipping.

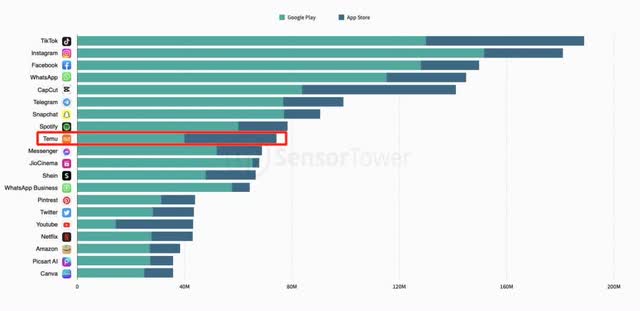

To understand Temu’s business model, all we need to do is to study Shein’s path. What Shein did, in effect, is consolidating China’s excess yet efficient manufacturing capacity and exporting low-cost products overseas. After a few years, Shein has built a world-class supply chain in Southern China. Shein has also cultivated a large group of experienced buyers who are very good at predicting overseas products demand. All Temu needs to do is to stand on Shein’s shoulders and do a better job. So far, Temu has been doing just that. It’s only been less a year since Temu’s launch and Temu has expanded to more than 30 countries. According to Sensor Tower, during Q2 of 2023, Temu made it to the top 10 globally most downloaded apps list. Temu’s growth is truly extraordinary.

Some investors are concerned with Temu’s potential near-term loss due to high customer acquisition cost and huge amount of subsidy. Clearly Temu’s expansion will impact PDD’s near term bottom-line but Temu is almost certainly to become profitable once the expansion phase is over.

PDD Valuation – Extremely cheap

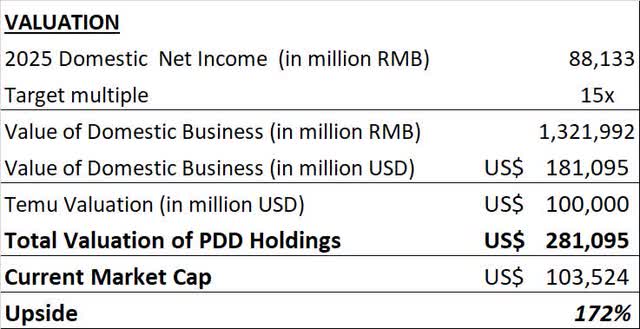

PDD’s domestic business is likely to grow its GMV from 3.2 trillion yuan in 2022 to almost 6 trillion yuan in 2025, or about $820 billion based on the current exchange rate. PDD’s monetization rate has risen to about 4.3%-4.5% based on my own estimate. If we assume a 4.3% monetization rate and 35% net margin (based on the recent net margin trend), PDD’s domestic business can generate revenue of 252 billion yuan, or about $35 billion, and net profit of 88 billion yuan, or $12 billion. Usually a fast growth business deserves a 25-30 times P/E multiple but considering the geopolitical discount (valuation discount to Chinese ADRs due to escalating geopolitical risks), we’ll apply a 15 times P/E multiple. This will put PDD’s domestic business at a valuation of $181 billion in 2025.

With Temu, we can use Shein’s valuation as a baseline, which was $100 billion before Temu’s rise and $66 billion at the latest round. Temu has surpassed Shein recently in terms of DAUs and GMV. In three years, Temu can easily be valued at more than $100 billion. Here we’ll use $100 billion as a conservative estimate.

Author’s calculation

Author’s calculation

Combined, PDD is worth almost $281 billion in three years. At current price (as of August 28, 2023) of barely $104 billion, PDD Holdings looks extremely cheap.

Risks to consider

The biggest long-term risk to PDD’s business is whether the company can stay focused and lean. So far PDD has maintained its super lean and efficient organizational structure. But almost all big tech companies including Alphabet (GOOG) (GOOGL), Meta Platforms (META), Tencent (OTCPK:TCEHY) and Alibaba eventually become too “bloated” and much less efficient as they grow to tech juggernauts. As PDD grows, some day it may face the same problem.

On the competition side, PDD and Temu face increased competition from live-streaming platforms such as ByteDance’s (BDNCE) Douyin and TikTok. ByteDance is a very formidable competitor both within China and outside.

Furthermore, both Alibaba and JD have taken efforts to address the competitive threat from PDD. Alibaba has replaced CEO Daniel Zhang with Alibaba’s co-founder and Jack’s Ma right-hand man Joseph Tsai. With the return of Tsai, Alibaba is likely to take dramatic steps in the future to improve the performance of Alibaba’s domestic e-commerce business. Similarly, JD’s founder Richard Liu has also taken on a more active role. It’s almost certain competition will pick up in China in the next few years.

From a valuation point of view, the Chinese ADRs are extremely volatile due to a worsening U.S-China relationship. PDD’s opaque communication style makes it even more volatile than other Chinese ADRs.

Summary

To sum up, PDD is a unique e-commerce platform with a differentiated and superior business model. Temu is rapidly replicating PDD’s domestic business overseas. PDD will likely to continue to grow at 20-30% annually in the next 3-5 years. While the stock is extremely volatile, I believe it is too cheap at the moment.

Read the full article here