PepsiCo, Inc. (NASDAQ:PEP) is known for its namesake cola, but it is also a snack food giant and has other top drink brands. Some of the well-known brands it owns includes: Gatorade, Lay’s (potato chips), Ruffles, Rold Gold Pretzels, Quaker Oats, Cheetos, Sabra Hummus, Doritos, Cracker Jack, Lipton, Ocean Spray, Rockstar Energy Drinks, Tostitos, Tazo, Mountain Dew, Fritos, Aquafina and so many more.

This stock has been in a downtrend lately, and that prompted me to take a look. I am a big believer in buying pullbacks, especially if key support levels are hit.

I am particularly intrigued when I see significant pullback in a stock that also happens to be a “Dividend King”, as is the case with PepsiCo. It’s a big deal to be considered as a dividend king because only 54 companies have earned this exclusive ranking. A stock is a dividend king if it has increased the dividend for at least 50 years. Let’s take a closer look at the buying opportunity I see in PepsiCo:

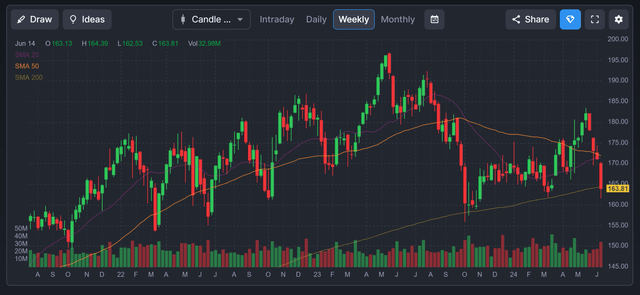

The Chart

As the chart below shows, this stock was trading for around $182 in May, and has since plunged to about $163 per share. What’s notable on the chart is that the stock is now trading right around the 200-week simple moving average, which is represented on the chart by a light-brown trend line. In the past couple of years, PepsiCo shares have rarely hit this trend line, but in the three times that it has, it rebounded. That seems to be quite a strong track record, and so I see this as a strong buy signal for two reasons. I see it as a buy signal because it has found support at this level three times now, and of course also because it rebounded from this level every time.

Finviz.com

Earnings Estimates And The Balance Sheet

Analysts expect PepsiCo to earn $8.17 per share in 2024, with revenues coming in at $94.54 billion. In 2025, earnings estimates are at $8.83 per share, on revenues of $98.95 billion. For 2026, earnings estimates jump to $9.49 per share, and revenues are also expected to rise to $103.23 billion. Based on these estimates, the price to earnings ratio is just around 20 times earnings in 2024, and only around a 17 times multiple for 2026. This looks like an attractive level to buy, especially with Coca-Cola (KO) shares currently trading for more than 22 times earnings.

As for the balance sheet, PepsiCo has about $45.87 billion in debt and around $8.35 billion in cash. PepsiCo also has an investment grade credit rating, which keeps borrowing costs relatively low.

The Dividend

PepsiCo currently pays a quarterly dividend of $1.36 per share, which totals $5.42 and yields about 3.3%. As a dividend king with increases every year for 51 years now, it’s quite likely this trend will continue. The 5-year dividend growth rate is 6.62%. Over the past ten years, the dividend has more than doubled from $0.5675 per share each quarter to the current $1.36 per share each quarter.

The Challenges Facing PepsiCo And Potential Downside Risks

The lower end consumer is showing signs of strain and there is a possibility that this will become a deeper problem for PepsiCo. This could lead to some consumers cutting back on snacks and even trading down to less expensive or generic brands.

Product recalls such as the one that Quaker Oats recently announced can impact revenues, brand value and profit margins.

PepsiCo is a global business and as such it is negatively impacted when the U.S. dollar is too strong. A strong U.S. dollar lowers margins, and it is strong right now because the Federal Reserve is keeping interest rates “higher for longer”. Meanwhile, the European Central Bank recently cut rates for the first time in years. This just serves to weaken the Euro and boost the strength of the U.S. dollar. This is a headwind for now, however the Federal Reserve recently released projections showing that they expect interest rates to likely be much lower in the next couple of years. If this is the case, the U.S. dollar could weaken significantly and go from being a headwind to becoming a tailwind.

There’s a new wave of weight loss drugs that are incredibly popular, and there is credible analysis that suggests the impact could be significant on the food industry. This is a potential downside risk based on the potential for these weight loss drugs to curb appetites, especially since so many people are now using these medications. These drugs are already incredibly popular but could become even more so as analysts at Morgan Stanley (MS) have suggested that up to 7% of the U.S. population, or around 24 million people, could be using weight loss by 2035. The impact of these weight loss drugs on the food industry could be felt more by PepsiCo due to the higher fat and sugar content in some snacks. The Morgan Stanley report states:

Significantly, survey participants cut back the most on foods high in sugar and fat, reducing their consumption of confections, sugary drinks and baked goods by as much as two-thirds. As more people in the U.S. use obesity drugs, overall consumption of carbonated soft drinks, baked goods and salty snacks may fall up to 3% by 2035.”

What Could Go Right

PepsiCo has had solid pricing power in the past, and it might continue to be able to put forth price increases that expand margins. The U.S. dollar is not likely to sustain the levels it holds now because interest rates are probably set to decline, and possibly significantly so, between now and 2026. Also, the U.S. dollar could be weakened by the already enormous and continuously growing national debt. The U.S. national debt is nearly $35 trillion, and it could become a crisis that undermines dollar strength.

PepsiCo still has time to adapt to the potential longer-term impact of the new weight loss drugs. It has been expanding into healthier snack options, which might be less impacted by these trends. It also has options to change portion sizes and raise prices in some instances in order to counter reduced volumes. I believe that with consumption of drinks, baked goods and salty snacks potentially falling 3% by 2035 (as projected above), there is enough time and there are multiple ways to more than offset these losses. Even the U.S. dollar could fall in value by far more than 3% by 2035, and that alone could diminish this risk factor.

In addition to lower interest rates potentially leading to a weaker U.S. dollar, lower rates could also ignite investor interest in dividend stocks and especially in dividend kings like PepsiCo. If interest rates decline by as much as the Federal Reserve expects between now and 2026, this would clearly make PepsiCo’s 3.3% yield more valuable to many investors, and that could lead to capital gains.

PepsiCo has the ability to significantly expand some of its brands. For example, Rockstar Energy drinks are popular in the U.S. but are relatively unknown in Europe and the rest of the world. PepsiCo’s international sales have been strong and have also seen operating profits expand in Europe and Latin America, which I believe shows more positive momentum is likely when it comes to international expansion. I believe PepsiCo has significant opportunities to expand in emerging market countries as more consumers in those countries see incomes improve and join the ranks of the middle class.

In Summary

I am a big fan of buying high-quality stocks after a big pullback. I am also a big fan of adding dividend kings to my portfolio. In this case, I see an opportunity to buy PepsiCo at an attractive valuation, plus the stock is now near a key support level from which it typically rebounds. I believe the strength in the U.S. dollar will reverse in the next few months as the Federal Reserve likely begins a rate cutting cycle. This can improve profit margins and also act to increase investor interest in dividend stocks. A lower U.S. dollar can act as a growth driver for profits going forward, and other growth drivers include international expansion. As with any stock that is trending lower, I think it makes sense to buy in stages and average in overtime, even if the stock is around a key support level, as is the case with PepsiCo.

Read the full article here