If you want to know why the PIMCO Dynamic Income Strategy Fund (NYSE:PDX), $22.82 closing market price, has been the best-performing CEF since I first recommended it to my Investing Group subscribers in January 2022, it’s because no other fund has been better managed to navigate the ups and downs of the markets.

PDX leveraged the recovery in energy and energy MLP stocks after COVID-19. It then transitioned to a more fixed-income credit fund when bond prices bottomed in the fall of last year after a brutal interest rate hiking period from March 2022 through July 2023.

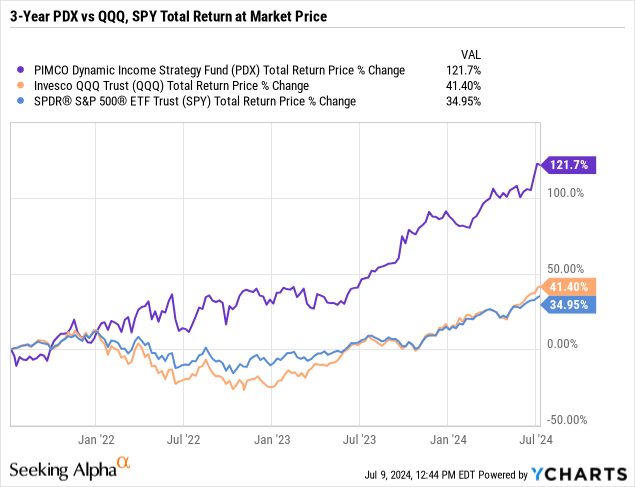

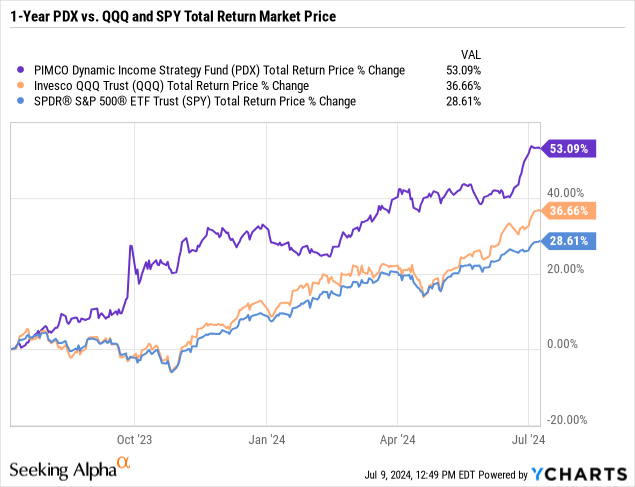

PIMCO pretty much called all of those highs and lows in energy and interest rates, and the results for PDX speak for themselves. Think it’s been tough for any fund to beat the Nasdaq 100 represented by the Invesco QQQ Trust ETF (QQQ), $497.77 closing market price, or the SPDR® S&P 500 ETF Trust (SPY), $555.82 closing market price? Well, here’s how PDX has performed on a market price total return basis compared to QQQ and SPY.

And just to be fair, I won’t use my original recommendation start date of January 10th, 2022 so as not to be accused of cherry-picking. I’ll simply use a 3-year longer-term period and 1-year shorter period comparison of PDX to QQQ and SPY:

YCharts

YCharts

So why do I still consider PDX undervalued even today? First, the more PDX transitions its portfolio from energy and energy MLPs to fixed-income securities, that should just continue to lower the fund’s risk profile.

Everybody knows what happened to energy stocks and energy MLPs during COVID-19. I’m sure that may have been part of the decision to lower the energy exposure in PDX when possible and get back to what PIMCO’s strength is in, i.e., fixed income.

That transition process started in September of last year when PDX was then known as the PIMCO Energy and Tactical Credit Opportunities Fund (NRGX). Here is part of the press release:

NEW YORK, Sept. 22, 2023 (GLOBE NEWSWIRE) — PIMCO Energy and Tactical Credit Opportunities Fund (NYSE: NRGX) (the “Fund”) announced that it will change its name, ticker symbol, investment objectives and guidelines, and portfolio manager lineup, as further described below. Pacific Investment Management Company LLC (“PIMCO”), the investment manager of the Fund, expects that the changes will reduce the Fund’s focus on investments linked to the energy sector in favor of a primarily income-oriented objective and broader, multi-sector credit mandate, which PIMCO believes has the potential to strengthen secondary market demand for the Fund’s common shares.

The Fund will be renamed “PIMCO Dynamic Income Strategy Fund” and its New York Stock Exchange ticker symbol will be “PDX”. The Fund’s new investment objectives will be to seek current income as a primary objective and capital appreciation as a secondary objective. The Fund will also rescind its policy to invest, under normal circumstances, at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in investments linked to the energy sector. The Fund will, however, continue to invest at least 25% of its total assets in the energy industry.

Two weeks later, on October 9th, 2023, I pounded the table again on PDX with this article, NRGX May Be A Stealth Opportunity To Get More Bond Exposure when inexplicably, PDX’s NAV rose +10.3% overnight from $19.98 to $22.03!

As it turned out, the portfolio managers of NRGX had made a large investment early on in a private holding called Venture Global LNG (Liquefied Natural Gas). Over the course of several months, they had seen the investment jump in value from +12.2% of the portfolio value, or approximately $100 million, to closer to +23% of the portfolio value, or $190 million.

Though I surmised in the article that PIMCO may have sold or was in the process of selling down the position, it was certainly not a coincidence that when PIMCO announced its new policy and name change from NRGX to PDX, the overall energy exposure in the fund declined from a total of 80% of the net portfolio value to 25%. This was almost exactly the appreciated value of the Venture Global LNG holding.

Fast-forward to today and PIMCO has actually taken their time in transitioning over to a multi-sector bond/credit portfolio. In fact, as of 3/31/2024, the 1st Qtr portfolio holdings of PDX still included:

+10.7% in energy-related holdings

PIMCO

+25.9% in energy MLPs

PIMCO

And a +17.5% position still in Venture Global LNG.

That’s +54.1% in energy and energy MLPs, so there’s still a long way to go to get down to the +25% target.

But like everything PIMCO has done with PDX, it was actually a smart move to take it slow, as energy has outperformed bonds so far this year. In addition, we won’t know what changes PIMCO has actually made over the last 3-months until the 2nd Quarter Holdings report is released later this month or in early August. So, there already may have been more of the changeover that we don’t see yet.

But most importantly, why do I think PDX is still cheap? First, compared to the rest of the PIMCO multi-sector bond CEFs that PDX is slowly morphing into, though it will continue to have 25% energy exposure, PDX trades at a far wider discount of -9.0% compared to the rest of the PIMCO fixed-income CEFs. It still has blown them all away in performance.

Second, I’m guessing PIMCO will gradually increase PDX’s use of leverage, which could be ideal timing as the Federal Reserve starts considering interest rate cuts.

And third, with PDX’s NAV up +13.9% YTD, there is a very good chance that PIMCO will increase PDX’s distribution yet again this year. PIMCO has already increased PDX’s distribution twice this year, but with a still very low +5.4% NAV yield, there is room to increase again. And the more PDX moves to a multi-sector credit and bond fund and the more leverage it uses, the higher the yield the fund should be able to support.

When you add it all up, PDX is still in an excellent position to continue to outperform, though probably not quite at the pace it once saw. That’s fine with me because, like the fund, I’m ready for a more conservative approach at 63 years of age too!

What are the risks? Most likely, the biggest risk to PDX is a US or global recession, which would certainly hurt the fund’s volatile energy and energy MLP holdings and particularly PDX’s largest position, Venture Global LNG, as a more illiquid private holding.

But that would be partly contingent on where PIMCO is in the transition over to a more traditional multi-sector bond fund since fixed-income would probably be considered a safe haven in a recession while interest rates would likely move down.

I’ll be back with another article and review after PIMCO releases PDX’s 2nd Quarter Holdings later this month or early August.

Conclusion

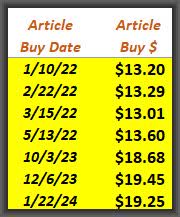

After recommending to my subscribers to buy PDX at $13.20 on January 10th, 2022, I have gone on to recommend PDX 6 more times to my subscribers on the following dates and prices (not including distributions):

Capital Income Management, LLC

In fact, my last recommendation on 1/22/24 at $19.25 in this article, PIMCO Dynamic Income Strategy Fund (PDX): New & Improved, Still Among Best Performing CEFs, would have netted you +21.8% since then if you took my advice.

As you might guess, PDX is my largest CEF holding for clients in my investment advisory program. And more and more, I hear from subscribers that PDX has grown into their largest holding as well.

Not bad for a fund that is probably the least known and the least followed of all the PIMCO CEFs.

Read the full article here