Investment Thesis

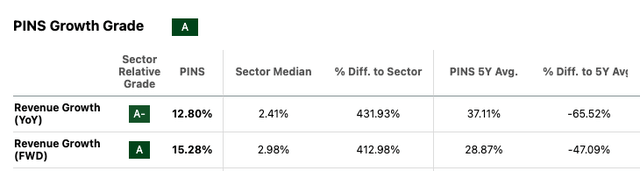

Pinterest (NYSE:PINS)beat earnings estimates by 42.86% for the last quarter, reporting $0.20 Normalized EPS vs $0.14 expected. In fact, revenue has been increasing at a faster rate than the industry over the last 5 years on a YoY basis. Next quarterly earnings are expected Aug 6 with a projected EPS of $0.28 which is an increase of 33.33% YoY.

SeekingAlpha

In my view, Pinterest is experiencing growth, reaching record high in both users which increased 12% YoY and revenue which increased 23% YoY. According to the last earnings call, user engagement is particularly strong, driven by features like curation boards and collages. As CEO William Ready explained during the call, Pinterest is aging down, and Gen Z is now the largest demographic, representing around 40% of the user base. This is fueling the growth as Gen Zers use the platform for inspiration and shopping.

“In fact, Gen Z rates Pinterest higher on promoting and preserving well-being metrics like self-worth, belonging, and purpose compared to other traditional social media platforms. As a result, Pinterest is aging down, a rarity in consumer internet applications, which typically age up as they mature. We’re also continuing to break through with Gen Z by connecting through culturally relevant moments.”

To capitalize on this trend, Pinterest is focusing on tool like direct links and improved ad measurement, leading to greater ad revenue. Additionally, they are investing in AI to personalize recommendations and further enhance the platform, all while maintaining strong profitability.

The online advertising landscape is encouraging. Both Pinterest and Snapchat (SNAP) recently revised their revenue guidance upward, and Facebook (META) also reported higher revenue that beat expectations. However, Facebook last earnings call projected weaker earnings, which could be a short-term concern specific to the platform.

SeekingAlpha

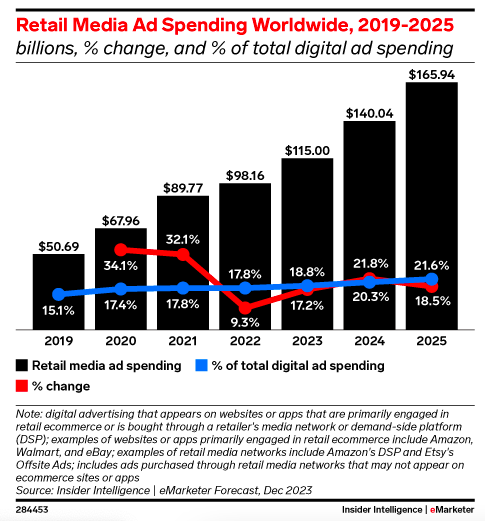

Despite this, the overall trend suggests a significant shift in advertising budget toward online channels. According to the study highlighted below, social media, in particular, is expected to capture around 20% of digital spending. In simpler terms, while individual platforms might experience fluctuations, social media advertising shows a clear upward trajectory and is likely to claim a larger portion of the digital advertising budget.

emarketer

I find Pinterest particularly well-positioned to capitalize on this trend due to several key strengths:

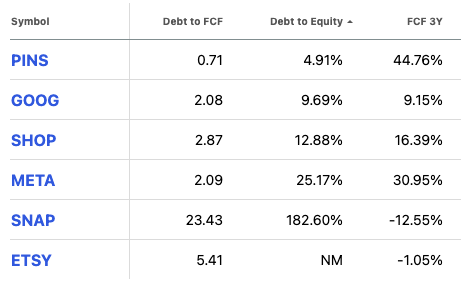

- Financial Discipline: Pinterest strong financial position, with lower debt and rising free cash flow compared to competitors like Snapchat, allows for more strategic investments. This flexibility fuels further revenue growth, user acquisition, and the ability to attract more advertising dollars.

SeekingAlpha

- Engaged user base: as you will read later in this article, Pinterest fosters deeper user engagement compared to other platforms.

- Affluent users: importantly, as you will also read further below, their user base skews towards affluent demographics who are already thinking about spending, making them highly attractive to advertisers.

Given these competitive advantages, I’m inclined to initiate coverage with a Buy on any price weakness as I believe the stock will find some resistance at its 52week high.

Sticky Ad-dollars and a differentiated Platform

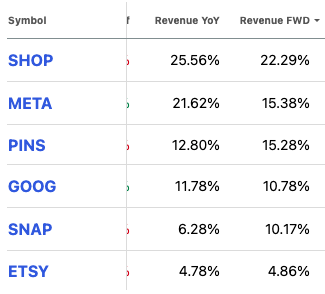

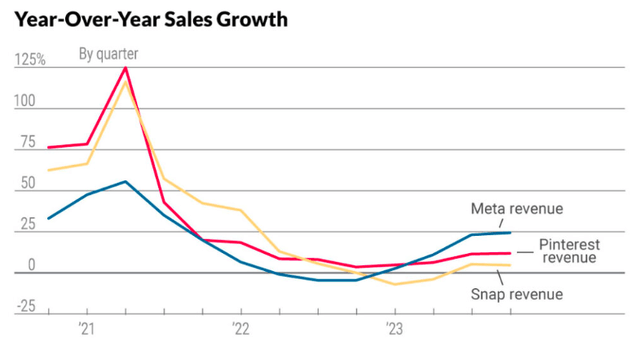

Online advertisement spending has seen a steady rise, particularly after the pandemic. Pinterest and Snapchat saw significant growth in 2021 with 52% and 64% increase in revenue respectively and the trend is expected to continue, although at a more moderate pace. For example, Pinterest revenue has increased at around 8.5% on average YoY since 2021, Snapchat revenue has been more erratic with revenue being flat for 2023.

Factset

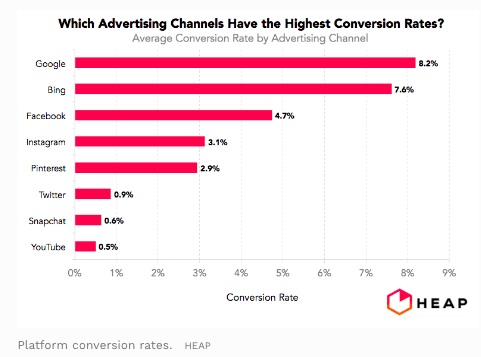

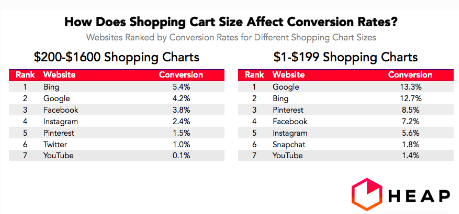

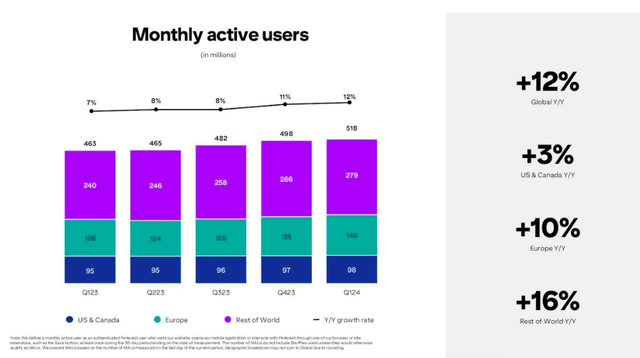

However, for advertisers, size isn’t everything. Conversion rates, which measures how effectively ads turn viewers into buyers, is a key metric. Here, Pinterest stands out. Statista aggregates Monthly Active Users for each platform and Pinterest despite having a smaller user base with around 500 million active users compared to giants like Facebook approaching 4 billion daily users and YouTube approaching 3 billion, the company boasts a conversion rate that surpasses YouTube, Snapchat, and Twitter (or X), combined, rivaling even Instagram’s effectiveness.

Heap.io

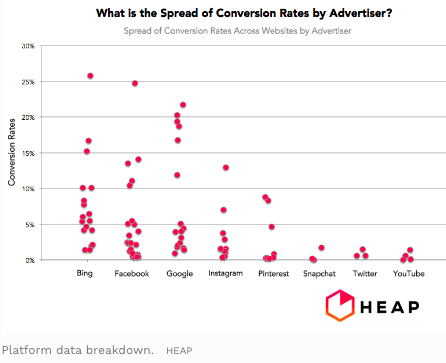

This is further amplified by a wider “conversion rate spread” across different websites, making Pinterest attractive to advertisers from various industries with a range of product prices.

Heap.io

Heap.io

A Pew Research study also reveals that Pinterest’s user base leans toward affluent demographics, aligning perfectly with their “ready-to-spend” mindset. Since taking the helm in 2022, CEO William Ready has prioritized shopping features, further strengthening this connection.

Pew Research

I believe a key pain point for Pinterest has been monetizing their large international user base with 80% of users but only 20% of the revenues as Bill Ready suggested during the earnings call in February. This is being addressed through strategic partnerships with Amazon and Google for ad serving, especially in international markets. These partnerships, rather than creating competition, appear complementary and hold the potential to drive significant long-term growth for Pinterest. The only risk that I find is that Pinterest does not grow their user base fast enough to capitalize on these projects. However, as the table below suggests user acquisition has been on a positive trend.

Pinterest Earnings Presentation

Management Evaluation

Pinterest’s leadership team has undergone a recent transformation. Bill Ready, with extensive experience in commerce and payment, having previously served at Google (GOOG) and PayPal (PYPL), took over as CEO in mid-2022. He holds significant stock options, which I consider a “high alignment ratio” with the company success. He took over Ben Silbermann, who is one of Pinterest cofounders and who still has significant voting power along with Paul Sciarra who is Pinterest other co-founder according to the latest 10 Q. Pinterest third cofounder is Evan Sharp, who transitioned out of an operation role in 2021. However, Sharp, is still supporting the company in an advisory capacity but SEC filings do not mention him as a controlling member.

Salary.com

Joining Ready is CFO Julia Brau Donnelly, who brings expertise in finance and accounting from her previous role at Wayfair (W). While she’s new to the industry, her credentials suggest a smooth transition.

I believe, that this new leadership teams reflects Pinterest’s focus on fresh ideas for continued growth. Partnerships with Amazon and Google are an example of this strategic shift. While user base growth remains a focus, and any new leadership transition requires adjustments, I find that the new management appointment have been meet with positive approval according to Glassdoor. Considering all the factors, I am inclined to give the current management a “Meet Expectations” rating.

Glassdoor

Corporate Strategy

Pinterest’s corporate strategy revolves around transforming the platform into the premier destination for inspiration-driving shopping. I find that they have this three-pronged approach:

- Seamless Shopping: features like direct links and advanced ad measurement tools facilitates effortless purchases directly within the platform by using partnerships with Amazon.

- AI- powered personalization: leveraging AI to personalize content and ad recommendations to user interests, leading to higher conversation rates

- International monetization: with a substantial international user base, Pinterest is forging a partnership with Google to unlock advertising revenue opportunities in those markets.

I have created the table below to compare their strategy to its competitors.

|

|

Snapchat |

|

YouTube |

X (Twitter) |

|

|

Daily Active User (DAU) |

500 million |

800 million |

4 billion |

2.5 billion |

611 million |

|

Conversion Rate |

2.9% |

0.6% |

4.7% |

0.5% |

0.9% |

|

Affluent User Base |

41% |

25% |

68% |

89% |

29% |

|

Corporate Strategy |

Focus on shoppable features, AI-powered personalization, expanding internationally |

Focus on augmented reality (AR) experiences, growing user base, diversifying revenue with Snapchat + |

Focus on building the metaverse, integrating platforms, increasing user time spent |

Focus on creator economy, short-form video content, subscription with YouTube TV |

Monetization through advertising and subscriptions (Twitter Blue) |

DAU is approximate

Source: From companies’ website, presentations, Pew Research

Valuation

Pinterest currently trades at around $41.44 after jumping around 20% after reporting earnings in late April. Employing a conservative 11% discount rate ((r)). This represents a hurdle rate that an investor expects to receive considering time value and inherent risk of that investment. To calculate it, I used a 5% rate for time value in addition to a 6% average market premium.

Then, using a simple 10 year two staged DCF calculator and I reversed the formula to obtain its implied FCF growth rate which is around 20%.

$41.44 = sum^10 FCF (1 + “X”) / 1+r) + TV FCF (1+g) / (1+r)

*I added Book Value in the calculation

That is, the market currently anticipates Pinterest FCF to grow at 20% this year. However, Pinterest expected FCF growth is 41.83%. So, valuation seems to be undervalued.

SeekingAlpha

Technical Analysis

The stock price has positive momentum due to several factors including a bounce in online advertisement spending and new growth projects. Further, I see the company has healthy financials with low debt and increasing FCF. The company also has smoother revenue with a positive trend. However, the stock is at a 52-week high after a 20% jump after the last earnings report so I believe it will find some resistance pressure at $43 pending more information. Therefore, I believe the stock will fluctuate between $40-$45. I will revisit my investment thesis as needed.

Next earnings report is estimated to be July 31.

TradingView

Takeaway

Pinterest smashed earnings with record user growth of 12% and revenue increase of 23% on a YoY basis. Next quarter’s projected EPS growth suggests continued momentum. Their engaged user base, particularly affluent Gen Zers, aligns with their focus on shoppable features. High conversion rates further strengthen their appeal to advertisers. In my opinion they are financially strong with low debt and rising free cash flow and under a new leadership prioritizing a growth strategy, Pinterest leverages AI to personalize experiences and drive conversions. While user base expansion remain a focus and the current stock price has found some pressure at its 52-week high, I will take a price weakness in the stock as a buying opportunity. For this reason, I am starting the coverage of the stock with a cautious Buy.

Read the full article here